How to Position Your Portfolio in a Market Downturn

Aug 2, 2024

This morning alone, over $2.9T in value has been wiped out from stocks & indices as they experience the most severe downturn since 2020, leaving investors scrambling to protect their portfolios.

This turbulence, reminiscent of previous market crashes, has shaken confidence in the resilience of the bull market that has dominated much of the past decade. International markets also haven't been spared, with the MSCI World Index down over 5%. This widespread sell-off has affected nearly all sectors and asset classes, prompting many to wonder if we're on the brink of a prolonged economic downturn.

Are we entering a contraction period?

The question of whether the U.S. is entering a contraction period can be assessed by examining key areas such as the economy, geopolitics, the US dollar, and US debt. Here’s a brief analysis of each factor:

The economy

The U.S. economy has shown mixed signals.

On one hand, there has been resilience in consumer spending and job growth. However, there are concerns about rising inflation and higher interest rates which could dampen economic growth.

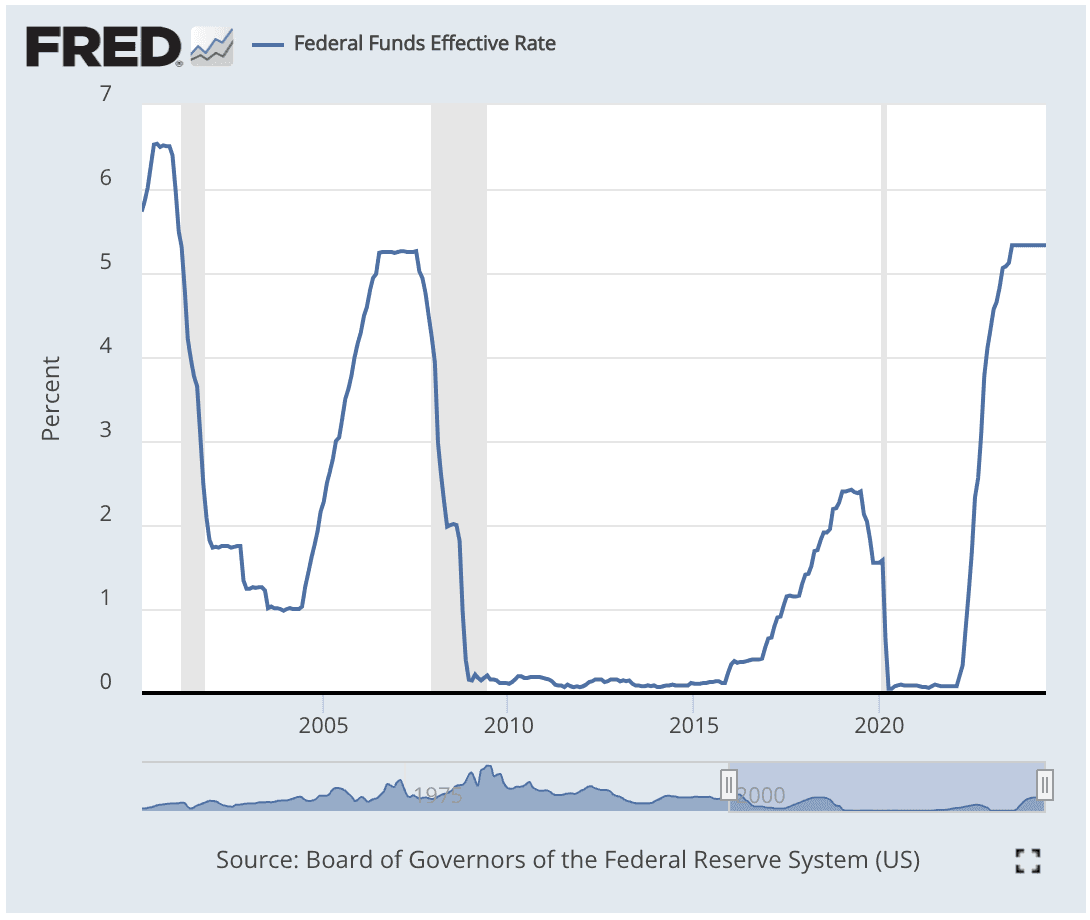

The Federal Reserve has raised interest rates to combat inflation, which historically can slow down economic activity and potentially lead to a recession.

Some indicators, such as a slowing housing market and decreasing manufacturing output, suggest that a contraction could be on the horizon.

For anyone who’s been paying attention, none of this should come as a surprise.

Around the world, but especially within the US, people have increasingly voiced their inability to make ends meet as prices skyrocket and wages stay the same (or in some cases, decrease due to more US workers engaged in multiple part-time gigs than ever with a simultaneous plummet in citizen-filled jobs.)

Inflation concerns have been at the forefront, with the Consumer Price Index (CPI) rising 3.8% year-over-year in 2024.

This persistent inflationary pressure has forced central banks worldwide to tighten monetary policy aggressively, shifting aggressively from the low-interest-rate environment that fueled much of the previous bull market - resulting in investors reevaluating risk assets.

Geopolitics

Geopolitical tensions are high, particularly with the ongoing conflict in Ukraine, strained US-China relations, and instability in the Middle East.

These tensions can disrupt global supply chains, increase energy prices, and create uncertainty in financial markets, all of which can negatively impact economic growth. Additionally, political instability within the US, such as polarization and policy gridlock, can hinder economic policy responses to emerging challenges .

Geopolitical tensions have also played a significant role in market uncertainty. Ongoing conflicts and trade disputes have disrupted global supply chains and heightened economic nationalism, leading to increased volatility in commodity prices and currency markets. These factors have combined with signs of slowing global economic growth to create a perfect storm for equity markets.

US Dollar

The US dollar has been relatively strong due to higher interest rates and global demand for safe-haven assets amid geopolitical uncertainties.

However, a strong dollar can have mixed effects: while it lowers the cost of imports and controls inflation, it can hurt US exports by making them more expensive for foreign buyers. If the dollar remains strong, it could contribute to a trade deficit, which can be a drag on economic growth.

Further, the dollar’s strength in recent decades has come from its correlation with oil, which is rapidly declining as Saudi Aramco recently began accepting non-USD currencies for trade.

US Debt

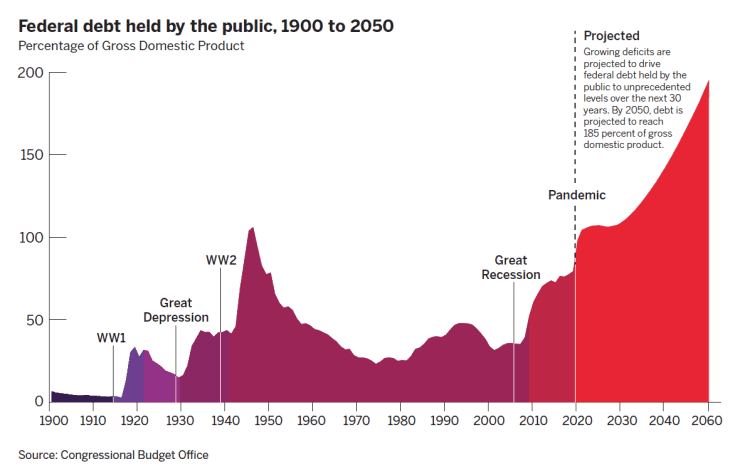

The US national debt is the elephant in the room at historically high levels, exceeding $35 trillion. The interest payments on this debt are becoming a larger part of the federal budget, which will ultimately crowd out other essential spending unless checked.

Last month alone, over 75% of taxes received went towards servicing interest payments on debt.

High debt levels can also limit the government's ability to respond to economic crises with fiscal stimulus. If investors lose (any more) confidence in the US’s ability to manage its debt, it could lead to higher borrowing costs and economic instability.

Unfortunately, with no signs of the government attempting to get spending under control, it seems we’re in for a ride.

Misc Data

GDP growth slowed to an annualized rate of 1.2% in Q1 2024, down from 2.1% in the previous quarter.

The unemployment rate has ticked up to 4.1%, a notable increase from the 3.7% seen just six months ago.

Corporate earnings have also disappointed investors, with many companies reporting lower-than-expected profits and providing cautious guidance for the future. This has led to a reassessment of equity valuations, which had reached historically high levels in many sectors.

These macroeconomic indicators suggest that the economy may be shifting gears, potentially signaling the end of the expansionary phase of the business cycle.

How to position yourself

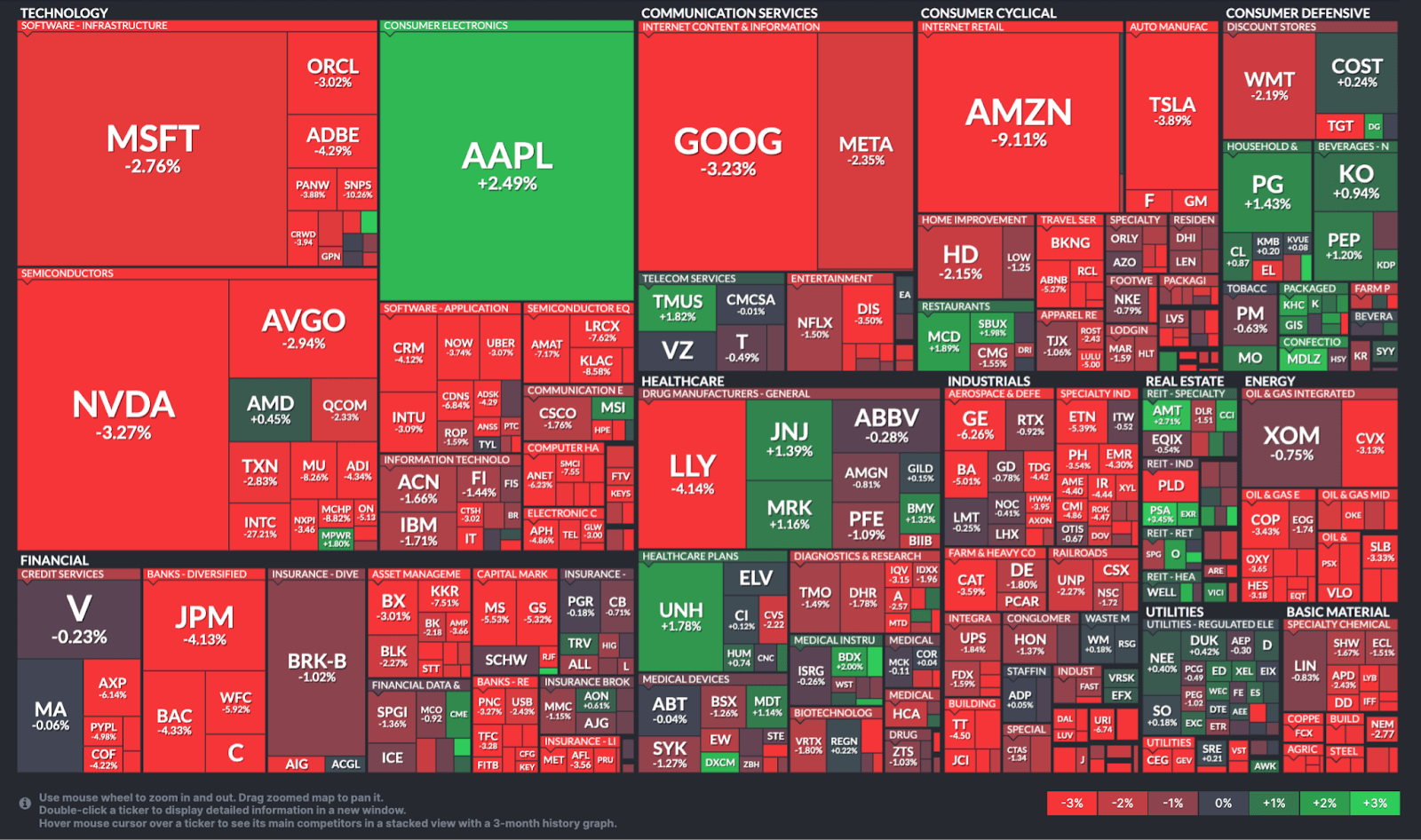

In this challenging environment, different market sectors are showing varying degrees of resilience. Traditionally defensive sectors like Consumer Staples, Utilities, and Healthcare have outperformed the broader market, though they too have experienced declines. Consumer Staples, for example, are down 5% year-to-date, significantly less than the overall market drop. Utilities and Healthcare have fallen 8% and 10% respectively, showcasing their relative stability in turbulent times.

On the other hand, growth-oriented sectors that had led the market's previous ascent have been hit particularly hard. Technology stocks, once the darlings of investors, have seen some of the steepest declines. Many high-flying tech companies have lost 30% or more of their market value, as investors reassess growth prospects in a higher interest rate environment.

For investors, navigating this market downturn requires a careful and measured approach. While it may be tempting to panic and sell everything, history has shown that such reactions often lead to missed opportunities when markets eventually recover. Instead, this may be an opportune time to reassess investment strategies and rebalance portfolios.

The importance of sitting on your hands

In reactionary times like these, sometimes it’s best to take some time on the sidelines and just spectate.

Diversification remains a crucial tool for managing risk. A well-diversified portfolio that includes a mix of stocks, bonds, and alternative assets can help cushion the blow of market volatility. Investors might consider increasing their allocation to defensive sectors and high-quality bonds, which tend to perform better during market downturns.

Value investing strategies may also come back into favor. As growth stocks face headwinds, companies with strong fundamentals, steady cash flows, and attractive valuations could offer a safer harbor. Dividend-paying stocks, particularly those with a history of maintaining or increasing dividends during tough times, can provide a source of steady income and potential stability.

For those with a longer investment horizon, the current market downturn may present buying opportunities. Dollar-cost averaging into quality companies or broad market index funds can be a prudent strategy to take advantage of lower prices without trying to time the market bottom.

It's also worth considering geographic diversification. While global markets have generally moved in tandem during this downturn, different regions may recover at different rates. Emerging markets, for instance, might offer growth potential once global economic conditions stabilize.

Final thoughts

As we navigate these turbulent waters, it's important to maintain perspective. Market downturns, while painful, are a normal part of the economic cycle.

Historically, markets have always recovered and reached new highs given enough time. However, the path to recovery can be long and unpredictable.

The key is to remain vigilant, stay informed, and be prepared to adapt as market conditions evolve.

What do you think: Are we just in a contraction, or could this be the beginning of the decline of an over-leveraged empire?

Share