Is Nvidia fraudrulent? Diving into the allegations

Jul 26, 2024

Introduction

NVIDIA is a company that 5 years ago, most investors had no idea about. Now, they’re celebrated as a titan in the tech world and a primary driving force in the stock market.

Without any doubt, the company has created a tremendous amount of wealth for a lot of people.

However, this may not be sustainable for much longer. Disturbing similarities to Enron and Cisco’s notorious downfalls are emerging, raising serious concerns about NVIDIA's financial integrity and its future stability.

In this article, I’ll explore the allegations that are growing increasingly noisy around NVIDIA and aim to determine whether it could be time to start taking some profits after a magnificent 5 year run of over 3,400% in gains.

The Allegations

Over the past 18 months, allegations have cast a shadow over the company's success, raising questions about the legitimacy of its reported earnings and business practices.

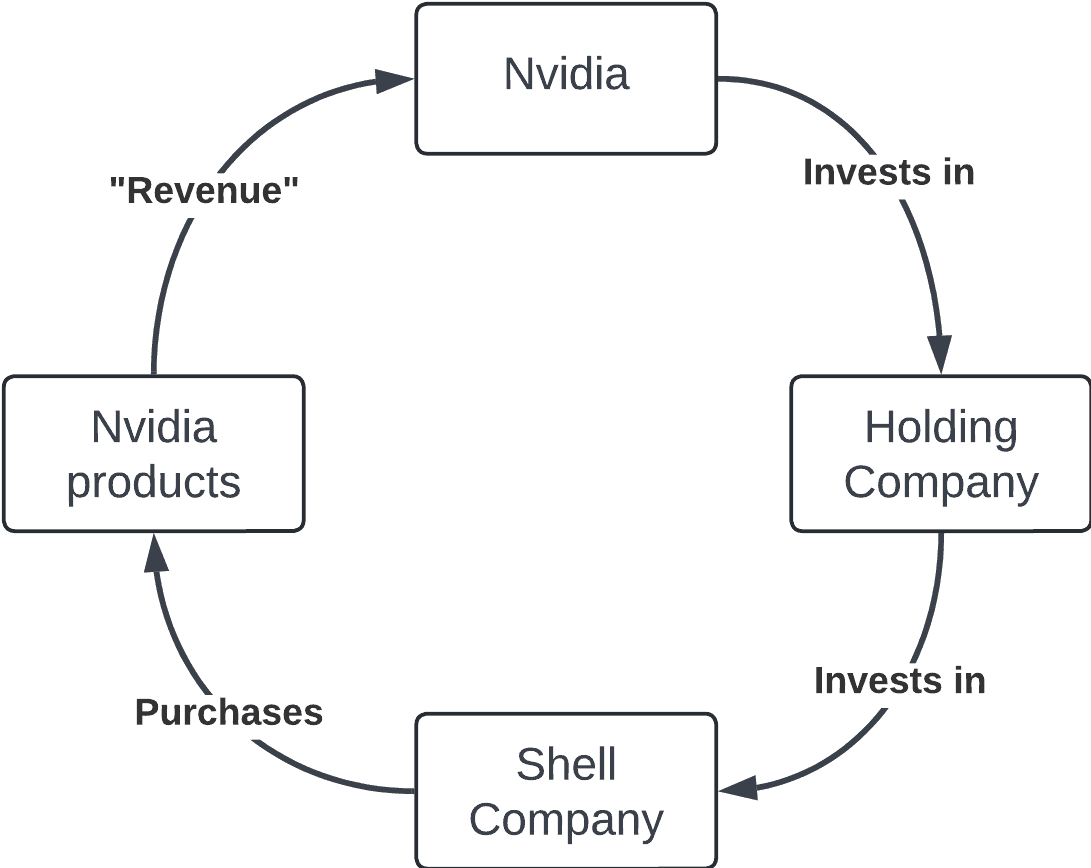

Earnings Are Propped Up By Shell Companies

One of the most serious allegations against NVIDIA is that it's artificially inflating its earnings through transactions with shell companies.

The claim suggests that NVIDIA funds these entities, then they turn around and use that funding to purchase NVIDIA products, creating a circular flow of money that significantly inflates revenue figures.

The cycle of NVIDIA’s cash

Coreweave: Case and Point

The most notorious example of this allegation stems from a company, Coreweave, that has raised over $10B in debt financing, largely from NVIDIA themselves, to acquire NVIDIA products (Coreweave even has a history of selling these products for a loss.)

In fact, NVIDIA’s Q2 earning’s beat came entirely from this one company, who took out a $2.3B loan, using NVIDIA’s H100s as collateral. H100s which it bought with said line of credit.

Even stranger? The loan was partially funded by NVIDIA - to purchase more NVIDIA products.

Yes, you read that correctly.

Even further concerning is that Coreweave’s main backers are Magnetar Capital, who were notorious scammers during the Great Financial Crisis.

Overall, there are an increasingly amount of concerning stories about shell companies surrounding NVIDIA, but it seems the music is continuing to play… for now.

YouTube video by Nobody Special Finance

Suspicious Shell Companies & Carbon Credits: The People Behind Coreweave

If true, this would significantly overstate the true demand for NVIDIA's products, which would constitute fraud and could lead to severe legal and financial consequences.

NVIDIA Is Starting To Compete With Its Largest Clients

Satya vs Jensen

Last year, NVIDIA started its own cloud service, DGX Cloud, a competitor to some of its own largest customers, including Microsoft and Amazon Web Services. DGX Cloud rents NVIDIA-powered servers from within AWS' data centers and then, promising greater computing capability, leases them back to NVIDIA's customers, The Information reported.

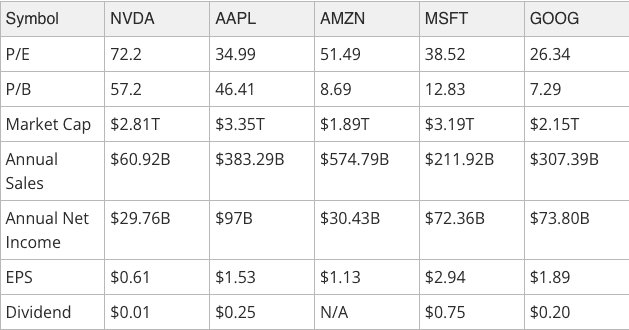

Comparing NVIDIA To Its Trillion Dollar Peers

When we dive into the numbers of the other companies with market caps above $1T, NVIDIA starts to stand out as noticeably overpriced.

When compared to the other companies on this list, NVIDIA has:

More than 3x lower annual sales

More than 2.5x lower annual net income to its closest-valued peer ($MSFT)

A significantly higher price to earnings ratio of 72

An outrageous price to book ratio of 57.2

Making it stick out like a sore thumb.

Wall street Is clearly justifying its current statistics based on the company’s growth trajectory, but that’s where things get messy, as its actual growth is significantly lower once you factor in the amount of questionable accounting practices in

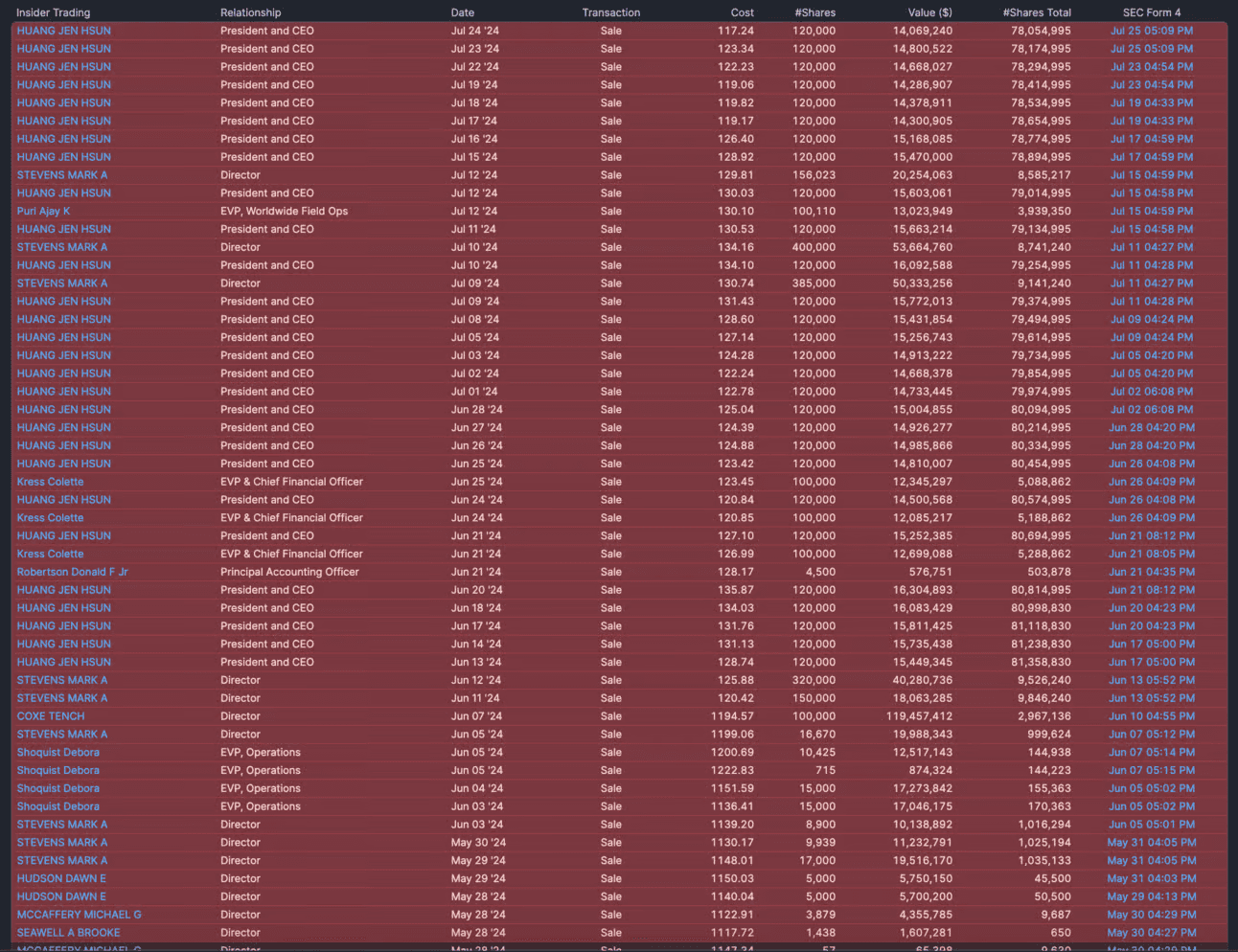

Massive Insider Selling

To add even more fuel to the fire, insiders have been absolutely DUMPING shares almost every single day, with Jensen Huang unloading 3,360,000 (or over $425M) in the last month and a half alone.

This certainly doesn’t reflect confidence in the company’s current situation.

Making Sense Of It All

Some of the issues discussed here are complex, so let’s break this down piece by piece.

Regarding NVIDIA’s revenues, I don’t think there’s any legal wrongdoing. The company is technically not breaking the law by recognizing revenues in the way it is due to the fact that it is providing specialized software, which can be regarded as a service.

Advance revenue claims could lead to future impairment charges, especially given tight supply and flexible client agreements.

High revenue concentration in few clients poses risks. Speculation exists that some sales to China may occur through third parties (Coreweave) to circumvent export restrictions.

NVIDIA's investment in CoreWeave, a major client, presents a potential conflict of interest. Other investors like BlackRock may have incentives to boost NVIDIA's revenues due to their exposure.

The loan backed by H100s is unusual, potentially indicating market irregularities or creative ways to work around Chinese sanctions.

Magnetar's involvement raises questions about potential short positions against NVIDIA.

Insider selling, particularly by CEO Jensen Huang, seems inconsistent with the company's bullish AI narrative.

These factors, combined with NVIDIA's high valuation multiples, suggest caution.

While the AI boom may justify some unconventional practices, historical semiconductor industry cycles and NVIDIA's 2017 SEC fine for inadequate disclosures about crypto-related revenue highlight the need for scrutiny.

Share