Treasure Hunting in the Stock Market: Finding Value Investments

Aug 16, 2024

When Warren Buffett bought his first shares of Berkshire Hathaway in 1962, little did the world know that this would mark the beginning of one of the greatest investment success stories in history. Buffett's approach, rooted in the principles of value investing, would turn a struggling textile company into a $700 billion powerhouse. But what exactly is value investing, and how can everyday investors apply its principles to their own portfolios? In this week’s article, we’ll cover the most profitable strategy in the markets: finding (and holding) value investments.

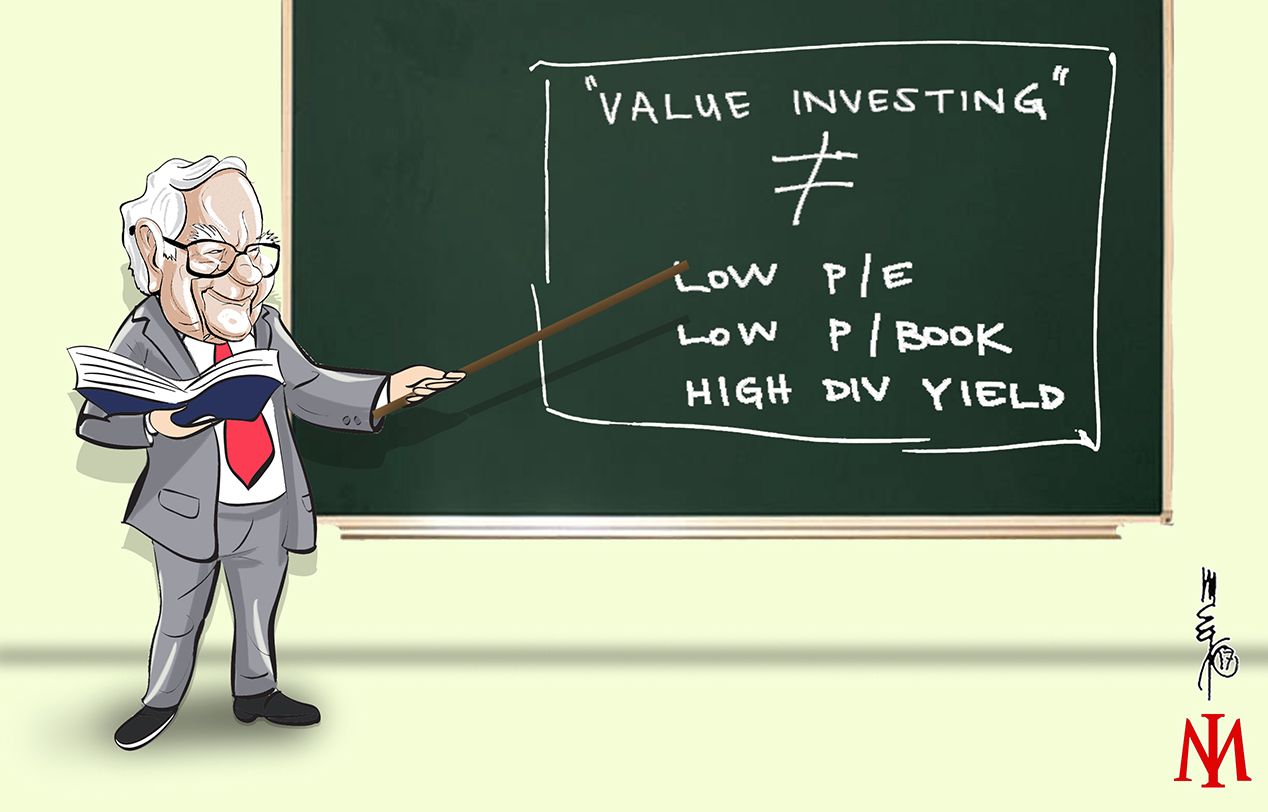

At its heart, value investing is about finding diamonds in the rough - companies that the market has overlooked or unfairly punished. It's the financial equivalent of finding a designer handbag at a thrift store price. The concept is simple, but the execution requires patience, diligence, and often, the courage to go against the crowd.

Buffett isn't alone in his success with this strategy. Take Seth Klarman, for instance. Known as the "Oracle of Boston," Klarman has quietly amassed a fortune by investing in unloved assets and out-of-favor companies. His Baupost Group has achieved annualized returns of around 20% since its inception in 1982, turning a $10 million initial investment into billions.

So how do these investing wizards find their golden tickets? Let's break down a few methods:

The Buffett Approach

Think of this as buying a castle with a moat. Buffett looks for companies with strong competitive advantages - or "economic moats" - that protect them from rivals. Think Coca-Cola's brand power or Apple's ecosystem. He also emphasizes the importance of solid management and consistent earnings. It's not just about buying cheap stocks; it's about buying great companies at a fair price.

So how do you determine if a company is great and selling at a fair price?

Here’s Buffett’s method in a nutshell

Determining if a company is great:

Durable competitive advantage: Buffett looks for companies with strong "economic moats" - sustainable advantages that protect a company's market share and profitability. This could be brand power, patents, network effects, or cost advantages.

Consistent earnings: He favors companies with a long track record of stable and growing earnings. Buffett is wary of businesses with volatile or unpredictable profits.

High return on equity (ROE): Buffett prefers companies that can generate high returns on shareholder equity without excessive debt.

Strong management: He looks for honest, capable managers who allocate capital efficiently and act in shareholders' best interests.

Simple, understandable business model: Buffett famously stays within his "circle of competence," investing in businesses he can easily understand.

Determining if a company is selling at a fair price:

Buffett uses a discounted cash flow (DCF) model to estimate a company's intrinsic value. While he hasn't publicly shared his exact formula, his approach can be approximated as follows:

Estimate the company's future cash flows (owner earnings) for the next 10-15 years.

Apply a discount rate (often using the risk-free rate plus a risk premium) to these future cash flows to get their present value.

Sum up these discounted cash flows and add a terminal value to get the company's intrinsic value.

Compare this intrinsic value to the current market price.

Buffett looks for a significant margin of safety - he wants to buy companies when they're trading well below his estimated intrinsic value. He's famously said, "It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price."

It's worth noting that Buffett's approach is more nuanced than just running numbers through a formula. He combines quantitative analysis with qualitative factors like the strength of the business model and management quality. He's also known to adjust his approach based on market conditions and specific company situations.

The Lynch Method

Peter Lynch, who turned Fidelity's Magellan Fund into a legend, had a different mantra: "Invest in what you know." Lynch believed that everyday investors could spot great opportunities just by paying attention to the world around them. Did you notice a new restaurant chain always packed with customers? That could be your next investment idea. Lynch also popularized the PEG ratio, which compares a stock's price-to-earnings ratio with its growth rate, helping investors spot undervalued growth stocks.

Invest in What You Know: Lynch believed that individual investors could gain an edge by paying attention to products and services they encounter in their daily lives. He encouraged investors to look for investment opportunities in their own areas of expertise or industries they understand well.

Classify Stocks: Lynch categorized stocks into six types:

Slow Growers: Large, mature companies with slow growth rates

Stalwarts: Large companies with moderate growth rates

Fast Growers: Small, aggressive companies with high growth rates

Cyclicals: Companies whose fortunes rise and fall with economic cycles

Turnarounds: Companies recovering from difficulties

Asset Plays: Companies with valuable assets not reflected in the stock price

Focus on Fundamentals: Lynch emphasized understanding a company's business model, competitive advantages, and financial health. He paid close attention to factors like earnings growth, debt levels, and inventory turnover.

Look for Reasonable Valuations: Lynch used the PEG ratio (Price-to-Earnings ratio divided by Growth rate) to assess whether a stock was reasonably priced relative to its growth prospects. A PEG ratio below 1 was generally considered attractive.

Understand the Story: Lynch believed every stock has a story. He stressed the importance of understanding why a company is growing, what its future prospects are, and how it plans to overcome challenges.

Long-term Perspective: While Lynch was known for active portfolio management, he advocated for patience and a long-term view. He believed that the longer you hold a stock, the more likely you are to see positive returns.

Diversification: Lynch's portfolios often contained hundreds of stocks. He believed in spreading risk across many companies and sectors.

Continuous Research: Lynch was known for his tireless research efforts. He read extensively, visited companies, and talked to management, customers, and competitors.

Be Contrarian: Lynch often looked for opportunities in unpopular or overlooked areas of the market. He was willing to go against the crowd if his research supported it.

Stay Flexible: Lynch adjusted his strategy based on market conditions and was willing to admit mistakes and sell when his investment thesis no longer held.

Lynch's approach combines thorough fundamental analysis with an investor's personal insights and observations. It encourages investors to leverage their unique knowledge and experiences while still doing rigorous financial analysis. This strategy aims to find growth at a reasonable price across various types of companies, making it a versatile approach for different market conditions.

The Graham Net-Net Strategy

This one's for the true bargain hunters. Benjamin Graham, Buffett's mentor, developed this ultra-conservative approach. It involves finding companies trading below their net current asset value - essentially, companies priced so low that you're getting their business operations for free. It's like buying a house for less than the value of the land it sits on.

Margin of Safety: Buy securities significantly below their intrinsic value.

Mr. Market Concept: Exploit market irrationality, buying low and selling high. Remove emotion and look at markets as a living, breathing tool at your disposal.

Intrinsic Value: Focus on a company's fundamental value, not market sentiment.

Financial Analysis: Thoroughly examine financial statements, especially balance sheets.

Diversification: Spread risk across multiple investments.

Defensive Investing: For conservative investors, buy stable, dividend-paying blue-chip stocks.

Net-Net Strategy: For aggressive investors, seek stocks trading below net current asset value.

Emotional Discipline: Control emotions in investment decisions.

Quantitative Criteria: Use metrics like P/E ratios, earnings stability, and dividend history to screen stocks.

Graham's approach emphasized protecting capital while seeking undervalued securities, using rigorous analysis and a long-term perspective. His strategy aimed to provide steady returns and minimize risk rather than chasing spectacular gains.

Now, let's apply these concepts to today's market.

Consider Alibaba (BABA)

often called the "Amazon of China." Despite its dominance in Chinese e-commerce, BABA trades at a fraction of Amazon's valuation. With a forward P/E ratio of around 10, it seems absurdly cheap for a company of its caliber. But here's the catch - regulatory crackdowns and geopolitical tensions have scared off many investors. Is this a value opportunity or a value trap?

But remember, in value investing, not all that glitters is gold. Many stocks are cheap for a reason. The key is to distinguish the temporary setbacks from the permanent problems. It requires rolling up your sleeves, diving into financial statements, and really understanding a company's business model and competitive landscape.

In the end, value investing is as much an art as it is a science. It demands patience, often years of it, as you wait for the market to recognize a company's true worth. But for those willing to put in the work and go against the grain, the rewards can be substantial. Just ask Warren Buffett.

Share