Who is Sterling Anderson & why is he Travis Kaleneck-ing his stock?

Dec 14, 2023

Aurora Innovation ($AUR) is a small-cap stock that can best be described as a promising series B-C stage startup that you can purchase on the public market.

The company is on a mission to make trucking autonomous - a bold vision that could genuinely disrupt a massive industry.

Based on their trajectory over the past few years, they’re bleeding cash quickly but making significant progress towards their mission and are acknowledged as a front-runner in the industry; all things considered, it looks risky, but potentially promising.

So why is a co-founder & executive dumping all of his stock?

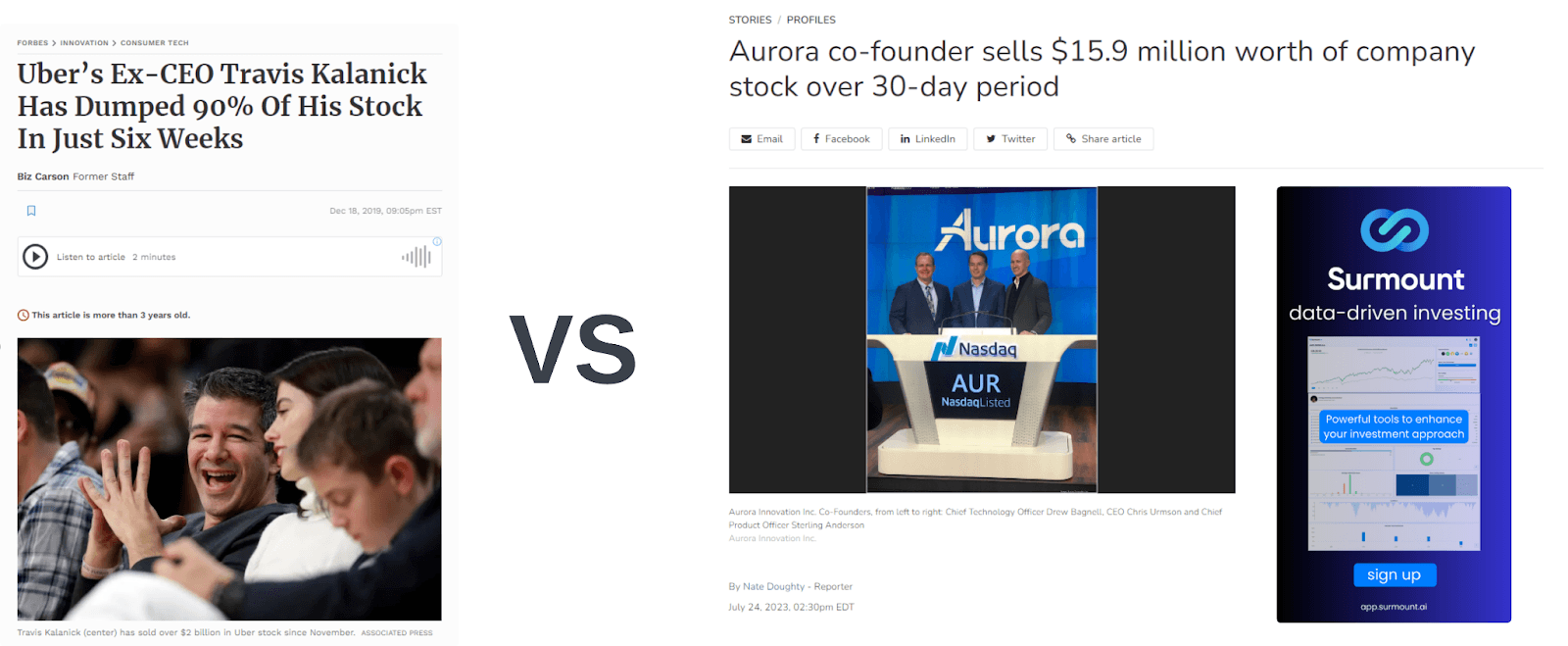

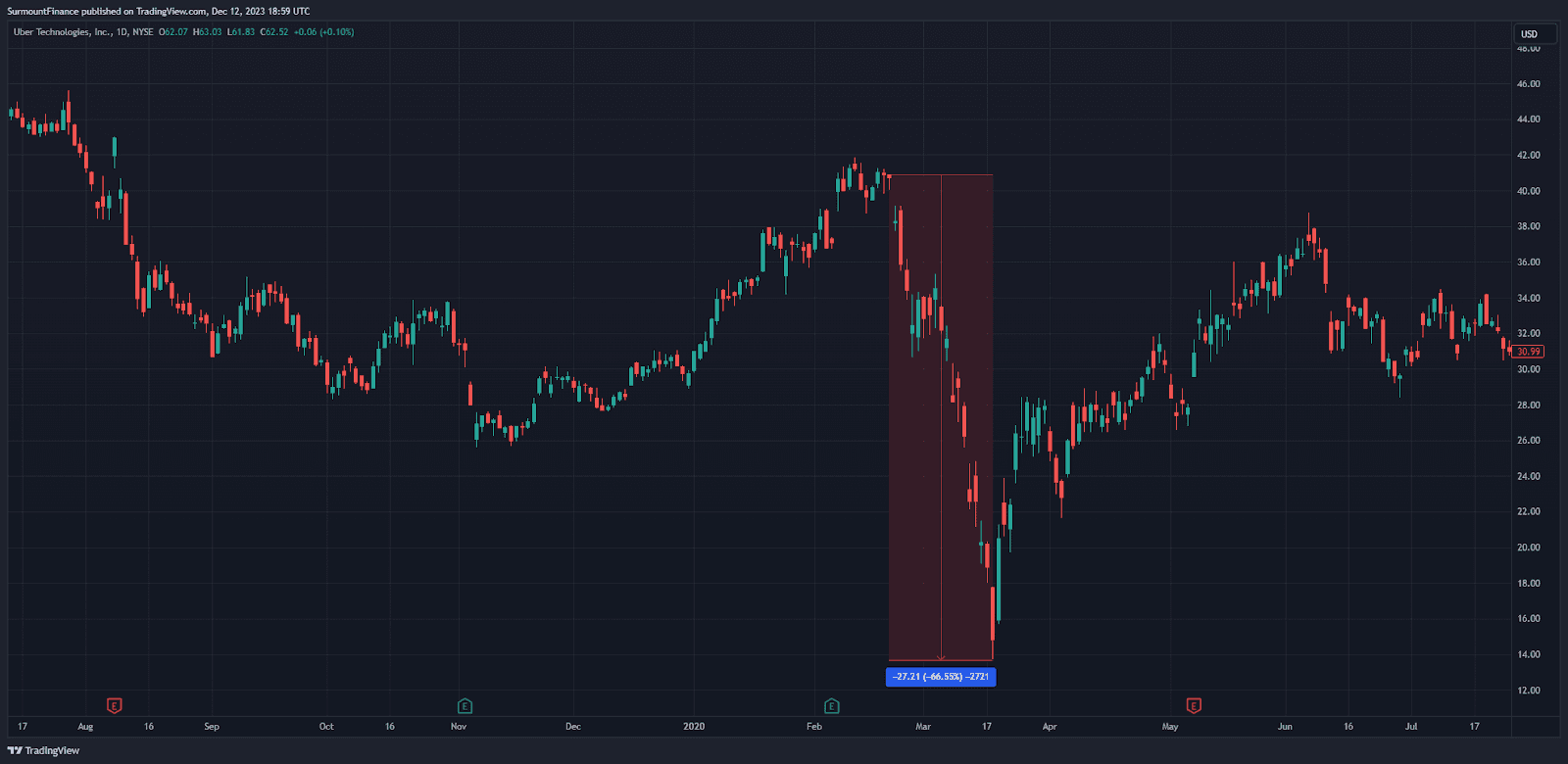

You might recall when, in 2019, Uber’s stock tanked nearly 70% in 6 weeks not long after their IPO due to their ousted CEO, Travis Kalanick, unloading his shares over a brief period.

There’s a similar situation playing out at a much smaller scale over at Aurora ($AUR), where co-founder & CPO Sterling Anderson has sold $23M in stock all throughout 2023.

However, instead of the stock continuing to tank as it did with its (-90%) performance throughout 2022, it’s come back 140% to $2.88 - putting a buffer between Stocktwits comments fearing an eventual OTC transition.

Executives sell stock all the time. So why is this case particularly interesting?

After a deeper dive, a couple of things stuck out to me:

No one else in the company has sold stock in the last 2 years

“Smart money” has built positions after the price drop

Insiders still own a lot of the company (comparatively speaking)

While there has been a considerable amount of insider selling at $AUR since 2022, it’s all come from one person: Sterling Anderson, co-founder & CPO.

Source: tipranks.com

Aside from that, insiders and “smart money” (aka: big institutions with dozens of analysts) have been piling into the stock.

Source: Yahoo Finance

Is Anderson gradually transitioning away from the company?

Is he just cashing out a portion of his position to fund his lifestyle?

Does he know something that we don’t and is selling in preparation?

Let’s dive in and try to find out.

I’ll be entirely honest: $AUR typically would never have popped up on my radar.

The first interaction with Aurora was in January 2023 when their stock was around $1.50 after a challenging 2022 where Aurora’s net income totaled (-$900M) and the stock nosedived 90% from $12 to $1.

$AUR rightfully wasn’t turning many heads going into 2023, but since kicking off the new year, the stock has revived a bit - up 140% to $2.88 from their $1 low.

It wouldn’t spark much of my interest based on technicals alone, but I happened to present at an event where they were a keynote speaker and throughout their presentation, I became extremely intrigued.

I hadn’t heard of them before, but as they were sharing their impressive list of who they were backed by, the traction they were making (industry partnerships, customer contract interest, product development) it became clear that I wanted to learn more about potentially making a private investment. Then they mention… they’re public?

At this point, I couldn’t take it; I’d pulled out my laptop mid-presentation and began some quick sleuth work. As much as I wanted to criticize their IPO as yet an employee/investor liquidation event & cash grab - I couldn’t.

This sparked a multi-month deep dive into as much as I could find about the company.

In this paper, I’ll share what I know so far and, based on the available information, speculate on whether this could be a purchasing opportunity.

Let’s look at the facts.

There are certain industries & ideas that have yet to be fully optimized and hold such massive opportunity for the companies that drive the next wave of innovation that professional investors are happy to “lose” billions on promising teams building big ideas before ever expecting to see a return; robotics & electric vehicles are both front-runners of that category the last time I checked.

So you could imagine that Aurora’s 10 year mission of making national carriers fully autonomous, along with their logo-crammed team slide, has been lighting up investors’ eyes (and opening their wallets) without much hesitation, since 2017.

The company raised over $1B from top investors prior to going public, and another $2.8B from and after going public.

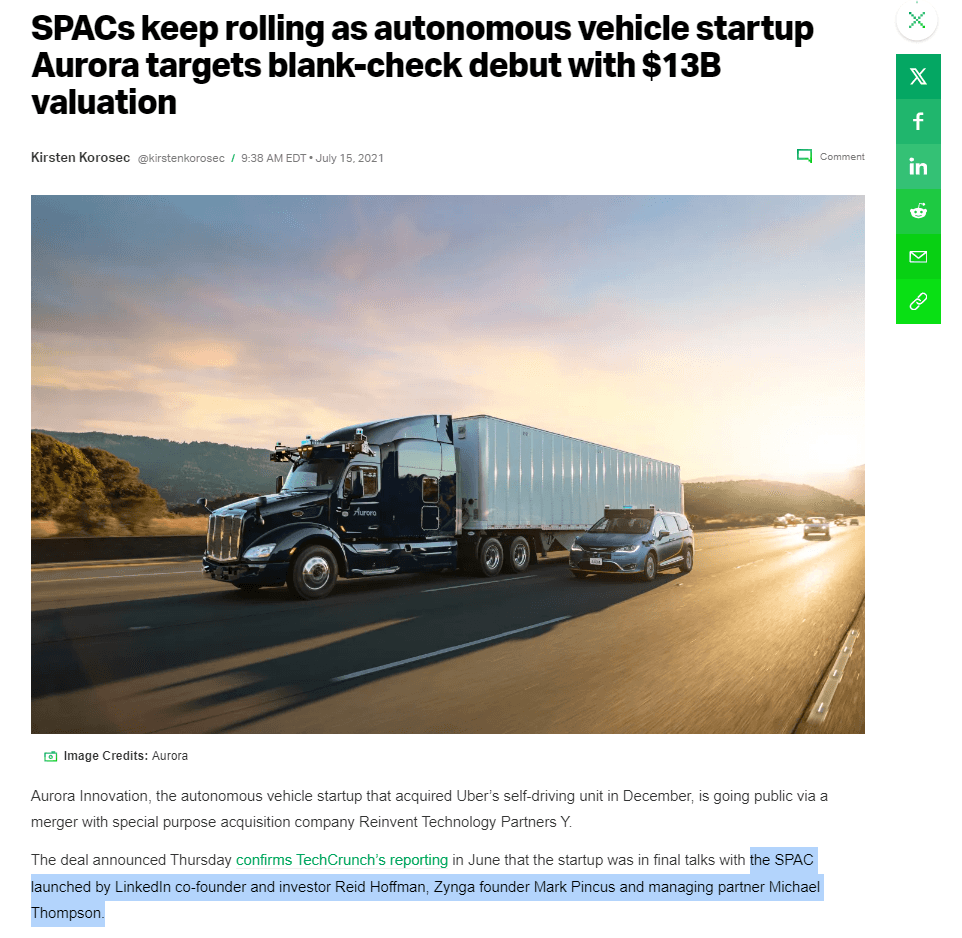

They went public in 2021 via Reinvent Technology Partners Y SPAC launched by Reid Hoffman (Linkedin), Mark Pincus (Zynga) and Michael Thompson (MP), which is a good place to start.

I was surprised to see that, even after PIPE shares free’d up and the cash grab could commence at a rather hefty ~$13B valuation, many of the insiders continue to hold.

Reid Hoffman still owns over 14M shares, which are worth around $40M at the current price, with none of the other insiders reporting any large sales since going public - signaling that they feel even the $13B valuation has room to grow.

Definitely interesting.

So again - who is this Sterling Guy and should we be any less bullish based on his consistent selling? Surely a co-founder & executive dumping stock should be a sign for us all to run to the hills with our profit, right?

Actually, I’m not so sure. The key missing detail here is: how much did Sterling own before & how much does he still own?

I have yet to find a full statement of ownership for Sterling. It very well could be that he’s just not a fan of the “marshmallow game,” and is simply cashing out a bit after building a successful company that is now liquid.

After all, the company is doing well - all things considered.

They’re burning a lot of cash and still pre-significant revenue, but they have a stockpile of cash with virtually no debt in comparison. As Peter Lynch would say: it’s going to be pretty hard for them to go bankrupt.

They can try, but it’ll be tough - especially being a Silicon Valley investor favorite.

In conclusion, until we see the situation unfold further, I’m unable to speculate on why Sterling has been selling so much stock, but one thing is clear: the company is in an opportunistic position.

$AUR a pile of cash, a clear ability to raise more, and the support of all of the top venture capitalists, which reduces their chances of going bankrupt. They’ll need to raise again in 2024

Their product is releasing before EOY 2024 and seems on track, if not ahead of projections, on their commercialization goals. They have significant partnerships in the space that represent the quality of demand for their product, and all things point towards their trials performing well.

I’m personally bullish on the trajectory and potential of the company, and will be holding my position throughout 2024.

What are your thoughts?

Share