Tesla's Bold Transition From Products to Systems

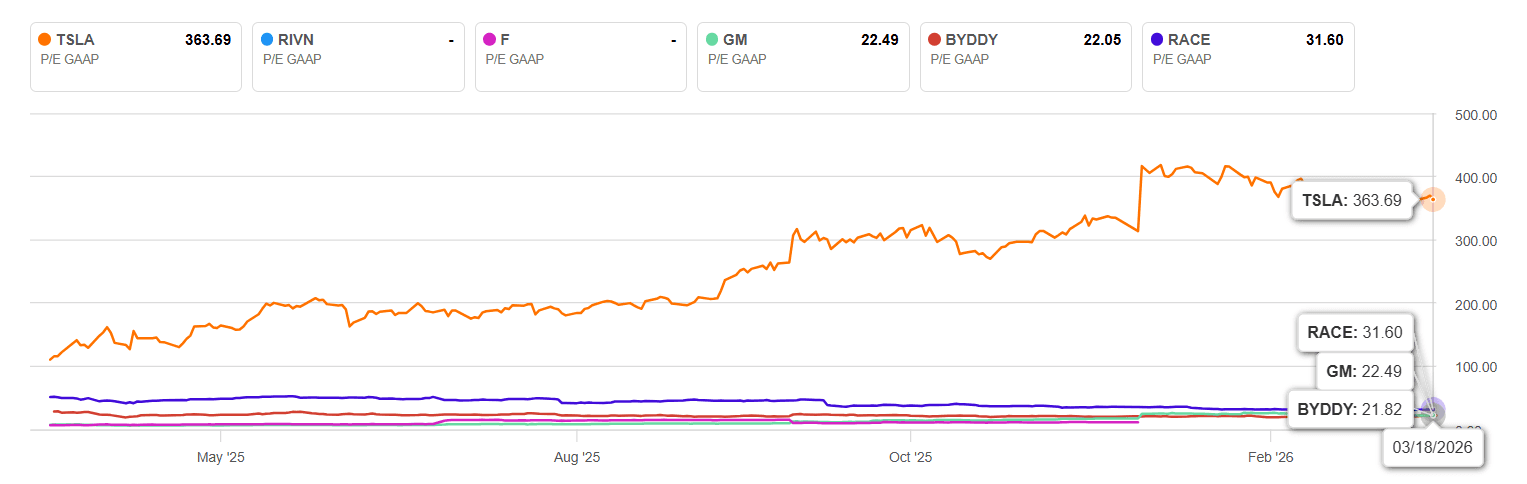

Considering the fact that Tesla Inc. (TSLA) has reported a trailing-twelve month net income total of only $3.8 billion, while trading at a market cap of nearly $1.5 trillion, it’s difficult to disagree with Tesla bears who argue that the stock is outrageously expensive. The fact that the company is trading over 360x its earnings, understandably puts off any investor with a traditional valuation model and a pulse.

To the spreadsheet-bound analyst, Tesla is a car company with a crumbling margin and an eccentric CEO. But to those who understand the shift from linear products to non-linear systems, the current P/E ratio is a red herring.

The mistake the bears make is evaluating Tesla through the lens of a 20th-century OEM—a business that sells a hunk of metal and hopes the customer comes back in seven years. In reality, Tesla is in the final stages of a "Great Decoupling." It is decoupling its valuation from the physical constraints of manufacturing and attaching it to the infinite scalability of global systems.

We are no longer looking at a company that builds "things." We are looking at the architect of three foundational pillars of the next century:

The Mobility System: Where the vehicle is merely a Trojan Horse for a high-margin autonomous network.

The Energy System: Where the battery is the hardware layer for a global, software-defined utility.

The Labor System: Where the humanoid robot is the precursor to a world with zero marginal cost of production.

If you are pricing Tesla based on how many Model Ys they delivered last quarter, you are playing a game that ended three years ago. The real trade isn't in the product; it's in the Operating System of the Physical World.

Energy Storage as the New Global Baseload

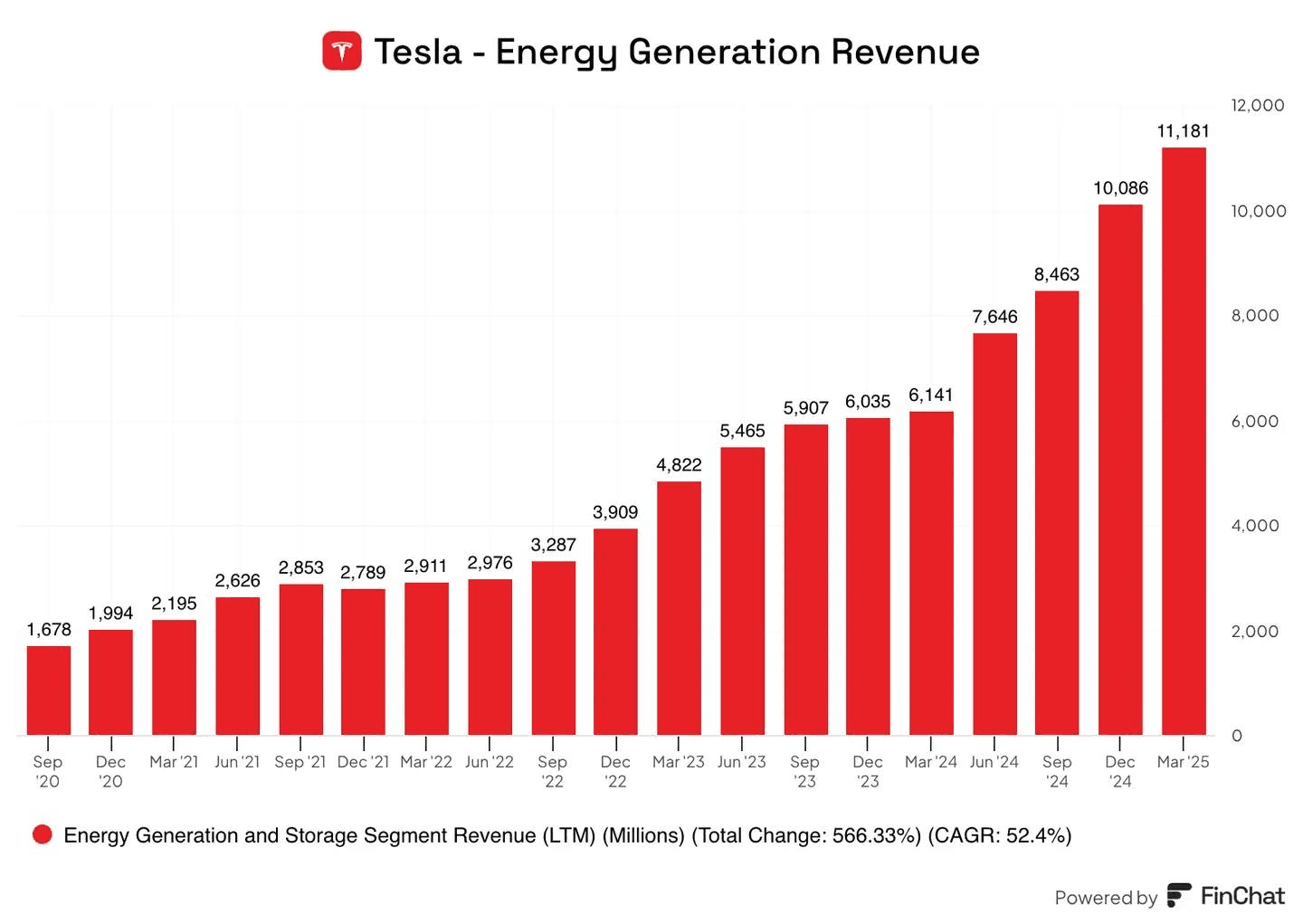

Tesla's energy division has transitioned, in recent years, from a side project into a major growth engine, outperforming the core automotive segment in several key metrics as of early 2026. While vehicle sales have softened, the energy business—which includes Megapack grid-scale storage, Powerwall residential batteries, and solar—has reached record-breaking profitability and scale.

The entire energy generation and storage division reported $12.8 billion in revenue for 2025, while pushing up its 5-year CAGR to ~53%:

Similarly, by the end of 2025, the division began contributing over 30% of the company's total profit despite accounting for only ~12% of revenue.

With the launch of Megapack 3 and the 20 MWh Megablock, Tesla has shifted from selling individual batteries to deploying "Instant Power Plants." These systems can be installed 23% faster and at 40% lower construction costs than previous generations. By the end of 2026, with the Lathrop and Shanghai Megafactories hitting a combined run rate of 100 GWh annually, Tesla will effectively be the world's largest "invisible" utility.

Autobidder: The High-Frequency Trader of Electrons

The real "system" play is Autobidder. Investors frequently miss that Tesla isn't just providing storage; they are providing the arbitrage layer for the global energy transition.

The System Play: As the grid becomes increasingly volatile due to intermittent solar and wind, the "spread" between low and high energy prices widens.

The Moat: Autobidder uses machine learning to autonomously trade energy in real-time. It’s essentially a high-frequency trading desk that never sleeps, ensuring that every Megapack on the grid is always performing the most profitable action—whether that’s frequency regulation, load shifting, or back-feeding the grid during a spike.

Ultimately, the old-guard investment thesis is that renewables are too "unreliable" to replace coal or gas. The contrarian insight is that reliability is now a software problem.

By aggregating thousands of Powerwalls and Megapacks into Virtual Power Plants (VPPs), Tesla can outmaneuver traditional peaker plants. In regions like Texas (ERCOT) and Australia, Tesla is already proving that a distributed network of batteries is more resilient and faster to respond than any centralized turbine.

Investor Note: We are witnessing the birth of a Distributed Global Utility. Unlike Duke Energy or PG&E, Tesla has no geographic boundaries, no aging legacy infrastructure to maintain, and a capital-light model where the "infrastructure" is often paid for by the end-user (Powerwall owners) or project developers (Megapack buyers).

Optimus and the Von Neumann Manufacturing Loop

We are witnessing the birth of the first real-world Von Neumann Machine—a system capable of using its own output to scale its own production. In 2026, the transition from prototype to the "V3" production model marks a singularity in industrial engineering. Tesla is currently repurposing its Fremont lines to produce up to one million units annually, effectively building the biggest labor force in history without hiring a single human.

This is where the product to systems transition is most visible.

We are essentially moving from "Automated Factories" to "Self-Replicating Labor Ecosystems." In the old world, doubling production required doubling your headcount or your CapEx in rigid, single-use machinery. In the new system, labor becomes a software-defined utility.

Similarly, with the 2026 rollout of Cortex 2 (Tesla’s 500 MW AI training cluster), Optimus is no longer limited by hard-coded scripts. It learns by observing video data of human workers. Once one robot learns to install a door seal or kit a battery module, every robot in the "system" learns it instantly.

The "Labor System" targets a manufacturing cost of $20,000 to $30,000 per unit. At an operating cost of roughly $5.71 per hour, Optimus doesn't just compete with human labor; it obliterates the concept of "labor scarcity" as a bottleneck for global GDP.

The market seems to be pricing Tesla based on how many cars they can sell to humans. The contrarian investor should be pricing Tesla based on how much human-equivalent labor they can manufacture and deploy into the global economy. When the "machine that builds the machine" is itself a robot, growth becomes exponential, not linear.

Winning Tesla Systematically, Not Sentimentally

The macro-thesis is clear: Tesla is transitioning from a car company to the backbone of global labor and energy. But for the retail crowd, the path from here to there is a "Volatility Trap." While the market oscillates between euphoria and panic, the smart money isn't "HODLing"—they are automating.

If you believe in the Tesla System, you cannot afford to be shaken out by a 20% drawdown driven by a bad quarterly delivery report. You need a mechanical edge that captures the massive "system-level" trend while cutting the cord the moment the momentum stalls.

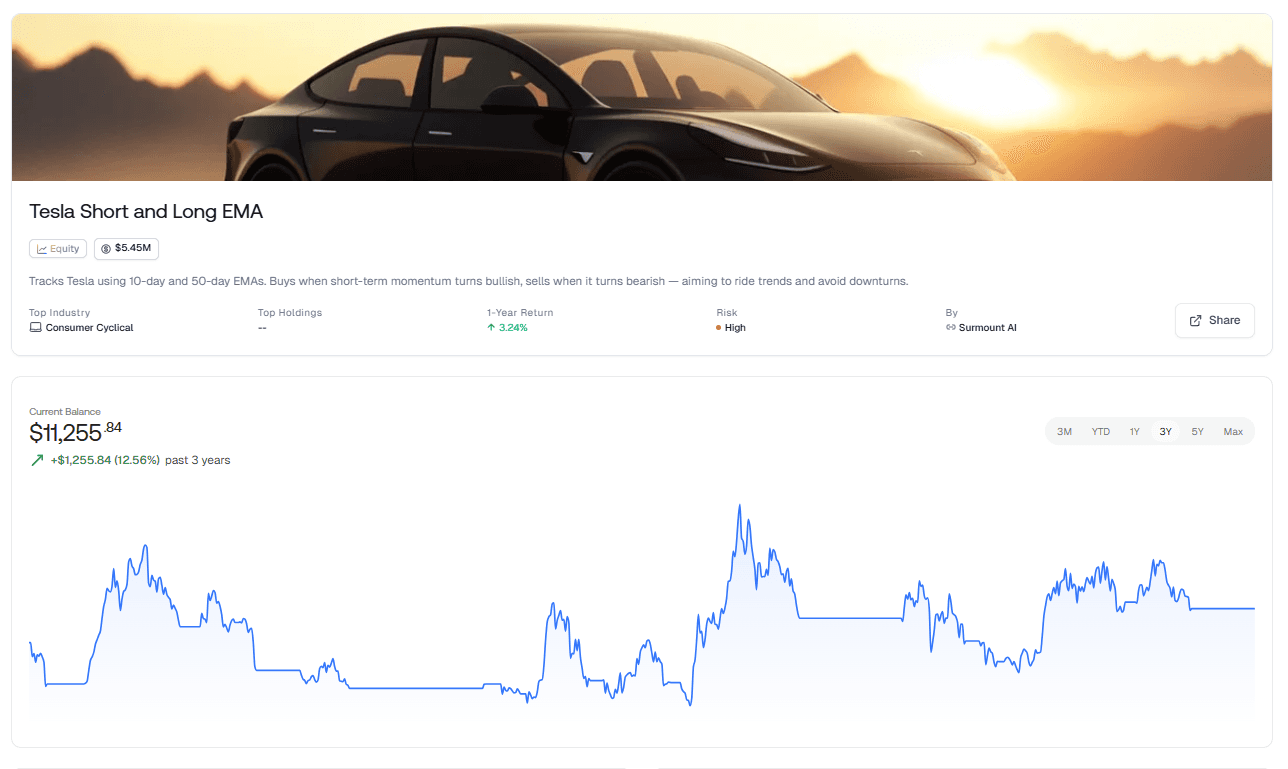

Enter the Tesla Short and Long EMA Strategy

Surmount’s Tesla Short and Long EMA strategy is a battle-tested, automated execution framework specifically tuned for TSLA’s unique volatility profile.

This isn't "guessing"—it’s a systematic Dual-EMA Trend Following strategy that acts as your portfolio’s automated circuit breaker.

The Bull Signal: When the 10-day EMA crosses the 50-day, the strategy recognizes the "System Re-rating" and puts your capital to work.

The Bear Shield: The moment the short-term trend breaks, the system triggers an automated sell. It ignores the "Elon tweets" and the headlines, focusing purely on the price action that matters.

Zero-Emotion Execution: No more staring at charts at 3:00 AM. This strategy deploys directly to your brokerage, buying the breakouts and sidestepping the "SaaSpocalypse" style drawdowns.

The greatest risk in a "Systems Play" is being right about the future but wrong about the timing. Don't let a temporary dip wipe out your long-term conviction.

[Deploy the Tesla Short and Long EMA Strategy]

NEVER MISS A THING!

Subscribe and get freshly baked articles. Join the community!

Join the newsletter to receive the latest updates in your inbox.