Amazon Stock: Market Correction Creates Rare Quality Entry Points

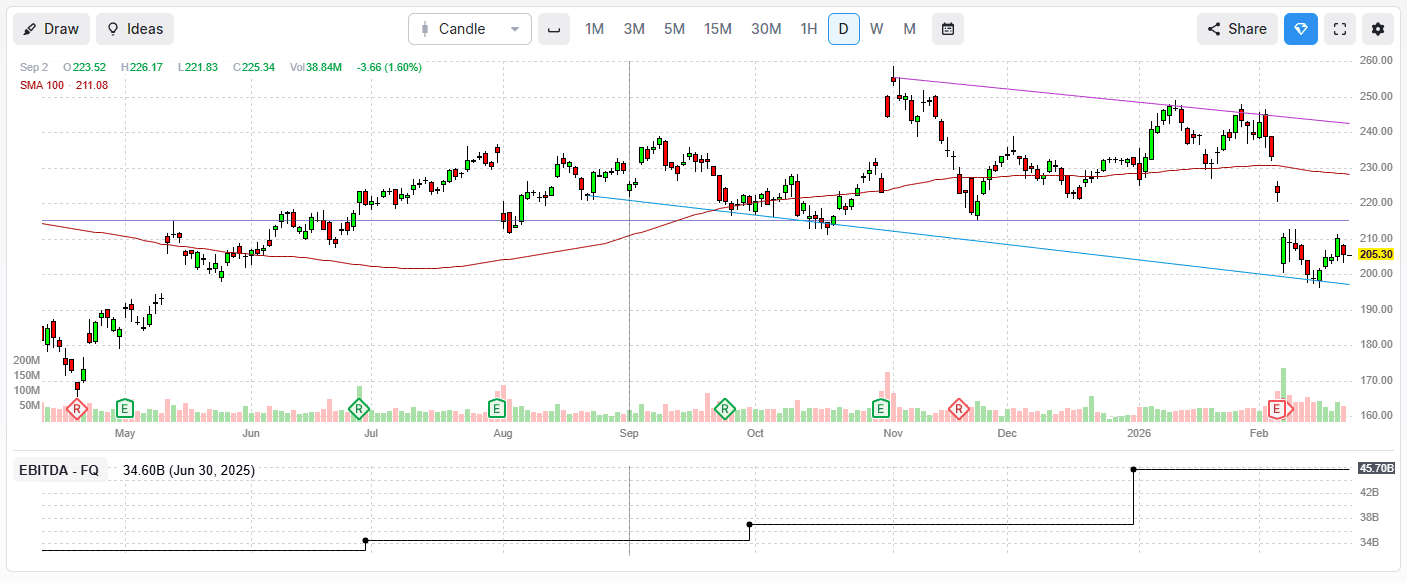

February of 2026 has been one of the most vicious months Amazon Stock price has witnessed, falling from a high of $246 to below the $200 mark. While the stock price has stabilized close to $205, at the time of writing this block, it has shed ~17%, or $451 billion, in just a matter of a few weeks.

Amazon’s drop has been among the more high-profile crashes amid the so-called SaaSpocalypse, where macro volatility, AI hype cycles, and fleeting fears around cloud growth have roiled tech markets. To add, uncertainties surrounding tariffs don’t seem to have calmed, even following the Supreme Court’s 6-3 verdict shooting down the administration’s broad, "emergency" reciprocal tariffs.

Interestingly enough, the Amazon chart technically shows that the stock’s price oscillates between a downward trending support and resistance channel. Currently, the stock has bounced off the bottom, and may be taking on an upward climb from this point onwards.

AWS Gives Amazon Stock Decades of Additional Growth

Amazon Web Services is seriously underrated. Most investors still treat it like a “mature utility” that has already peaked, ignoring the seismic shifts under the hood. The reality is that AWS is entering a phase of unprecedented reacceleration, fueled by AI demand, massive infrastructure expansion, and proprietary hardware that competitors simply cannot replicate by heavy investing alone.

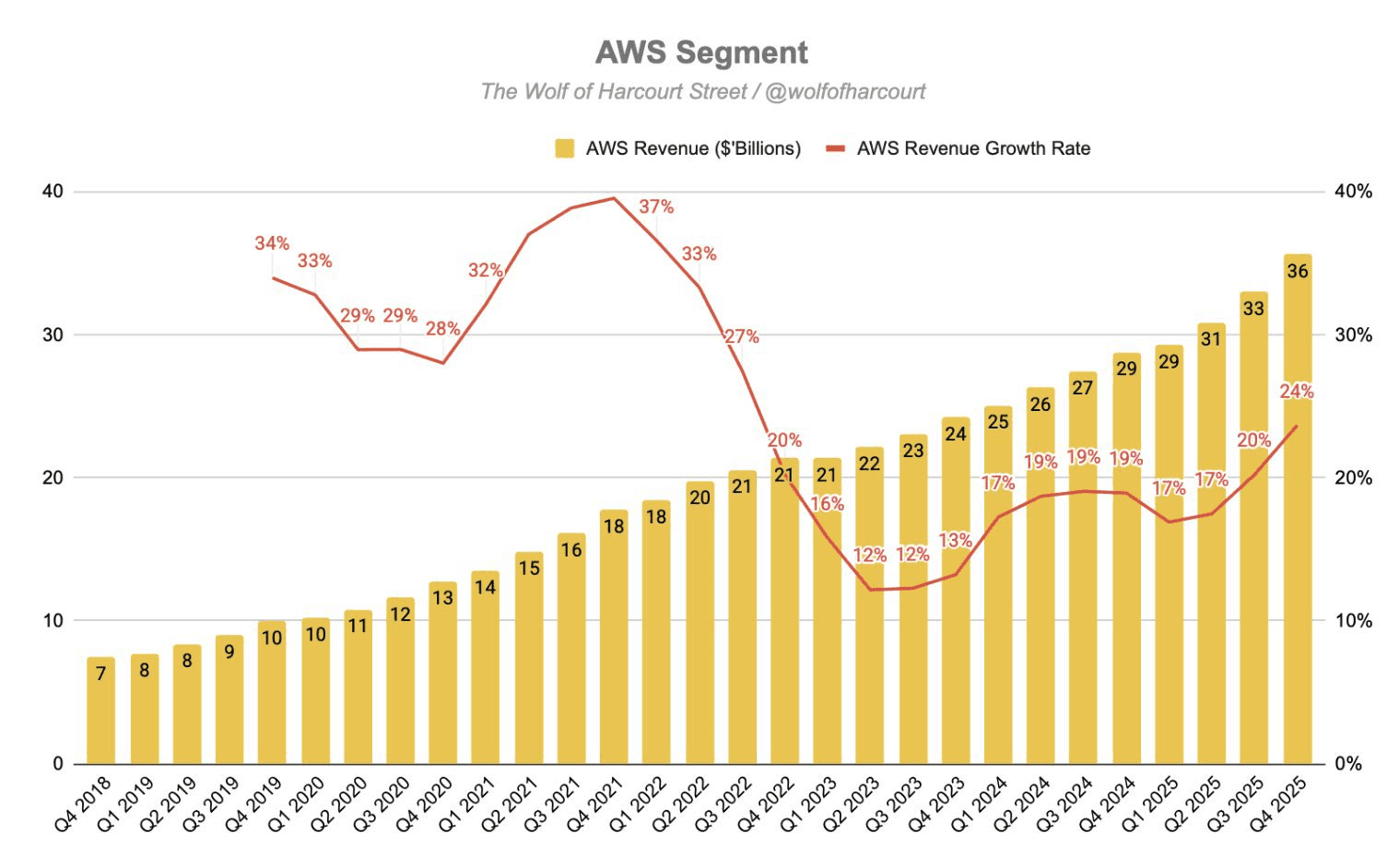

By the end of 2025, AWS reached an annualized revenue run-rate of approximately $142 billion. What makes this figure staggering isn't just the size, but the momentum behind it:

Year-over-year Growth:

AWS delivered 20% growth for the full year of 2025.

The Upward Trajectory:

Growth didn't just stay steady; it accelerated throughout the year, climbing from 17% in Q1 to a robust 24% in Q4.

The "Gigascale" Factor:

Delivering 24% growth on a $142 billion base is fundamentally different from a smaller competitor growing at 30%. In absolute terms, AWS is adding more incremental revenue to its top line each quarter than most of its rivals generate in an entire year.

Perhaps the most critical takeaway relating to this performance is that this expansion actually occurred despite significant capacity constraints. Throughout late 2025, Amazon leadership noted that growth was limited by the physical speed at which they could deploy data centers and procure specialized hardware.

Crucial Insight: When a business accelerates while reporting "supply constraints," it signals a fundamental market imbalance where Demand > Available Infrastructure.

This shift changes the investment thesis from a "demand-capture" story to an "execution-delivery" story. It implies three points in particular:

Zero Demand Risk:

Amazon doesn't need to find new customers to grow; it simply needs to build more "digital shelf space."

Instant Monetization:

In a supply-constrained environment, incremental capacity (new data centers, more chips) converts into revenue almost the moment it comes online.

The $200B Mandate:

This imbalance is exactly why Amazon is willing to shock the market with a $200 billion CapEx projection for 2026. This isn't speculative spending—it is a race to build the pipes for a flood of demand that is already at the door.

Amazon Retail: Tariffs Are an Overblown Fear, Not Reality

While the "SaaSpocalypse" headlines focus on cloud volatility, a quieter—and perhaps more significant—mispricing is happening in Amazon’s core retail business. The market is currently obsessing over the "Tariff Creep," treating President Trump’s plan B tariffs as an existential threat to margins. However, a closer look at the data suggests that for a behemoth like Amazon, tariffs are less of a brick wall and more of a speed bump that they have already learned to outrun.

The prevailing narrative, since early 2025, has consistently been that new trade duties will decimate e-commerce margins. In reality, Amazon’s retail engine is actually far more insulated than the market realizes.

Unlike specialized importers, Amazon’s revenue is hedged across millions of SKUs. The explosion of its Everyday Essentials brand (which grew twice as fast as other categories in 2025) demonstrates a shift toward high-velocity, price-resilient household goods that are often sourced regionally rather than exclusively through high-tariff corridors.

Similarly, while Amazon did "pre-buy" inventory in early 2025 to hedge against initial spikes, the real story isn't the inventory—it's the delivery. By regionalizing its network, Amazon has effectively decoupled "landed cost" from "delivery cost."

Similarly, the "bear case" ignores the massive structural tailwind generated by Amazon’s internal logistics revolution. While the world frets over a 15% tariff, Amazon has been quietly hacking away at its own overhead by two overlooked pillars:

Warehouse Automation:

Through the deployment of over 750,000 robots (and counting), Amazon has managed to cut per-unit shipping costs for eight consecutive quarters as of early 2026.

AI-Driven Placement:

New AI models like "Wellspring" and "Rufus" are optimizing inventory placement to ensure that items travel shorter distances. In 2025 alone, Amazon delivered over 8 billion items same-day or next-day in the U.S.—a 40% increase in speed that actually lowered the cost-to-serve.

The market treats retail as the "boring" side of the house—a slow, low-margin legacy business. Amazon is proving the opposite. Retail is supposed to be slow and low-margin. Amazon proves scale and AI investments make even the ‘boring’ side of the business a growth machine."

By the time a tariff-related price increase hits a competitor’s shelf, Amazon has already offset that cost through robotic sorting and AI-optimized last-mile delivery.

A Classic Case of Mispricing

The confluence of these factors suggests that the market is currently blinded by short-term noise. Investors are overreacting to the "sticker shock" of a $200 billion CapEx budget and the optical volatility of trade policy, while ignoring the underlying acceleration of a $142 billion cloud titan and a retail engine that is systematically engineering its own cost-savings.

Amazon is not spending defensively; it is scaling to meet a verified surge in demand that its current infrastructure literally cannot contain. When you pair a historically low valuation with a business that has effectively decoupled its margins from macro headwinds through robotics and AI, the current dip below $205 doesn't look like a breakdown—it looks like a classic case of mispricing.

Take Action with a Forward-Looking Momentum Strategy

Opportunities like this don’t come around often.

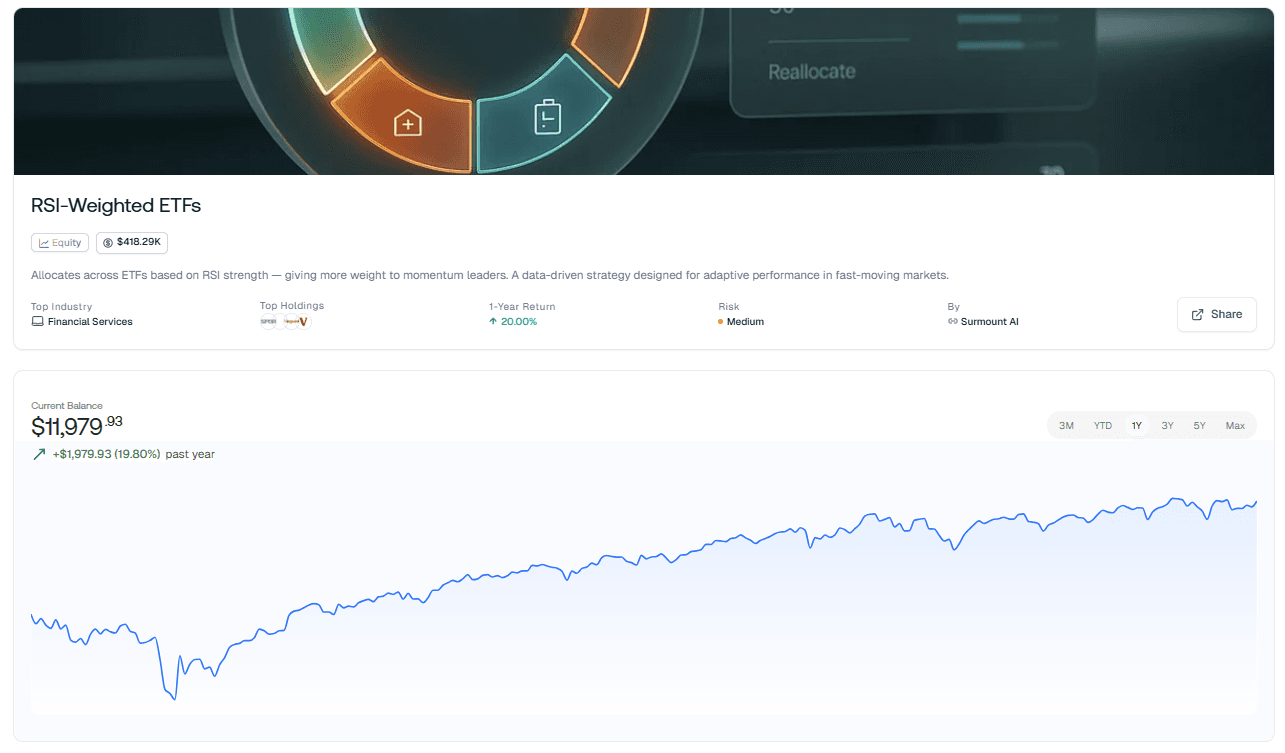

One way to tap into such opportunities as they arise is to follow an automated strategy such as Surmount AI’s RSI-Weighted ETFs:

By using a data-driven strategy that allocates across ETFs and equities based on Relative Strength Index (RSI), you can systematically capture momentum in fundamentally strong assets like Amazon, while avoiding headline-driven panic. This approach empowers you to make informed allocation decisions in fast-moving markets, turning temporary dips into potential gains.

Try this strategy today and position your portfolio to capitalize on quality opportunities in dynamic markets.

NEVER MISS A THING!

Subscribe and get freshly baked articles. Join the community!

Join the newsletter to receive the latest updates in your inbox.