Dividend Investing Isn't Dead — It Was Just Hibernating

For the better part of a decade, dividend investing was the strategy that serious investors loved to mock. While growth stocks were compounding at eye-watering rates and the S&P 500 was delivering double-digit annual returns with mechanical reliability, parking capital in dividend payers felt like the financial equivalent of bringing a horse to a car race. The obituary was written early and often. Income investing was for retirees. Yield was irrelevant when you could get price appreciation instead. Dividends were a consolation prize for companies that had run out of ideas.

The critics weren't entirely wrong — for that environment. When the Federal Reserve holds rates near zero for years on end, the income advantage of dividend stocks evaporates. When cheap money is infinite, growth-at-any-price becomes a rational strategy. When passive indexing into mega-cap tech names delivers 25% annual returns, the careful selection of cash-generative, dividend-paying businesses looks painfully pedestrian. The macro environment from 2012 through roughly 2021 was specifically engineered to make dividend investing look obsolete. The problem is that environment no longer exists — and the hangover from it is only just beginning.

What Hibernation Actually Looks Like — And What Wakes It Up

Hibernation is not death. It is a strategic withdrawal in response to hostile conditions, followed by an eventual, powerful return. To understand why dividend investing is waking up, you need to understand precisely why it went to sleep.

Three forces suppressed dividend stocks for the better part of a decade:

Near-zero interest rates collapsed the relative attractiveness of yield.

When cash pays nothing and bonds barely register, investors rationally chase appreciation instead of income. Dividend stocks — which tend to be mature, slower-growing businesses — simply couldn't compete with the narrative momentum behind high-growth names.

The dominance of mega-cap technology created a gravitational pull that distorted the entire market.

Capital flowed into passive index funds, which mechanically concentrated into the largest names, which inflated their valuations further, which attracted more capital. It was a self-reinforcing cycle that had almost nothing to do with fundamentals.

Free cash flow compression didn't matter when credit was cheap.

Companies could borrow their way through thin margins and still satisfy markets hungry for growth stories.

Each of those three conditions has now inverted.

Interest rates are no longer near zero — they are sitting at levels not seen in over fifteen years, and more critically, expectations for meaningful Fed rate cuts have been repeatedly walked back as inflation proves stickier than consensus expected. The relative income advantage of dividend stocks is no longer theoretical. It is real and it is growing.

Meanwhile, the mega-cap technology trade is showing its first serious cracks, not because these are bad businesses, but because they are now carrying an enormous AI capital expenditure burden that is quietly eroding the very free cash flow that justified their premium valuations.

When Amazon, Alphabet, Microsoft, and Meta are spending hundreds of billions on AI infrastructure with uncertain return timelines, the implicit promise of the index has changed. Buying the S&P 500 today is not the diversified, low-risk bet it once appeared to be. It is a highly concentrated wager on AI capital expenditure generating attractive returns at elevated valuations. That is a very different risk proposition.

History offers useful context here.

The early 2000s saw a near-identical setup — a decade of growth stock dominance, extreme valuation concentration, and a subsequent rotation that was both sharp and sustained.

Dividend-paying, value-oriented stocks dramatically outperformed the index for the better part of six years after the dot-com peak.

The 1970s stagflation era offers another parallel: when inflation runs persistently above expectations and real rates pressure speculative valuations, capital seeks businesses with tangible pricing power and real cash generation.

Dividend growth stocks, almost by definition, are that kind of business. They have survived long enough to generate consistent cash flows, maintained enough competitive positioning to sustain and grow payouts, and carry balance sheets disciplined enough to weather economic turbulence. These are not accidents. They are signals.

This Isn't Your Grandfather's Dividend Strategy

Here is where the contrarian argument gets interesting — and where many investors, even those warming to the dividend thesis, get it subtly wrong. The rotation underway is not a flight to safety in the traditional sense. It is not about retreating into sleepy utility stocks and praying for stability. That version of dividend investing — low beta, bond-proxy, clip-the-coupon — may have its place, but it misses the real opportunity.

The businesses leading this rotation share a different profile. They have pricing power in inflationary environments. They have hard asset exposure or infrastructure characteristics that generate durable cash flows regardless of what the Fed does next. Many are direct beneficiaries of the very trends — AI buildout, energy infrastructure expansion, geopolitical reshoring — that are supposedly the exclusive domain of growth investing. The difference is that these companies are capturing those tailwinds without carrying the speculative valuation premium. They are being paid to wait while the market figures out that not everything worth owning trades at 35 times earnings.

This also matters for how investors should think about volatility. One of the quiet casualties of the growth-stock decade was the normalization of enormous drawdowns as the price of admission for competitive returns. Investors learned to tolerate 30%, 40%, even 50% peak-to-trough declines in individual positions because the eventual recovery always seemed to justify it.

That tolerance is about to be tested in a more serious way as rate pressures, geopolitical risks, and AI capex uncertainty converge. In that environment, lower-volatility, income-generating strategies don't just look more comfortable — they look strategically superior on a risk-adjusted basis.

Dividend investing was never a bad idea. It was an idea that fell out of fashion during an era specifically hostile to its virtues. Patience, cash flow discipline, valuation rigor, and income compounding are not obsolete concepts — they are cyclical ones. And if the current macro environment is telling us anything clearly, it is that the cycle has turned.

The hibernation is over.

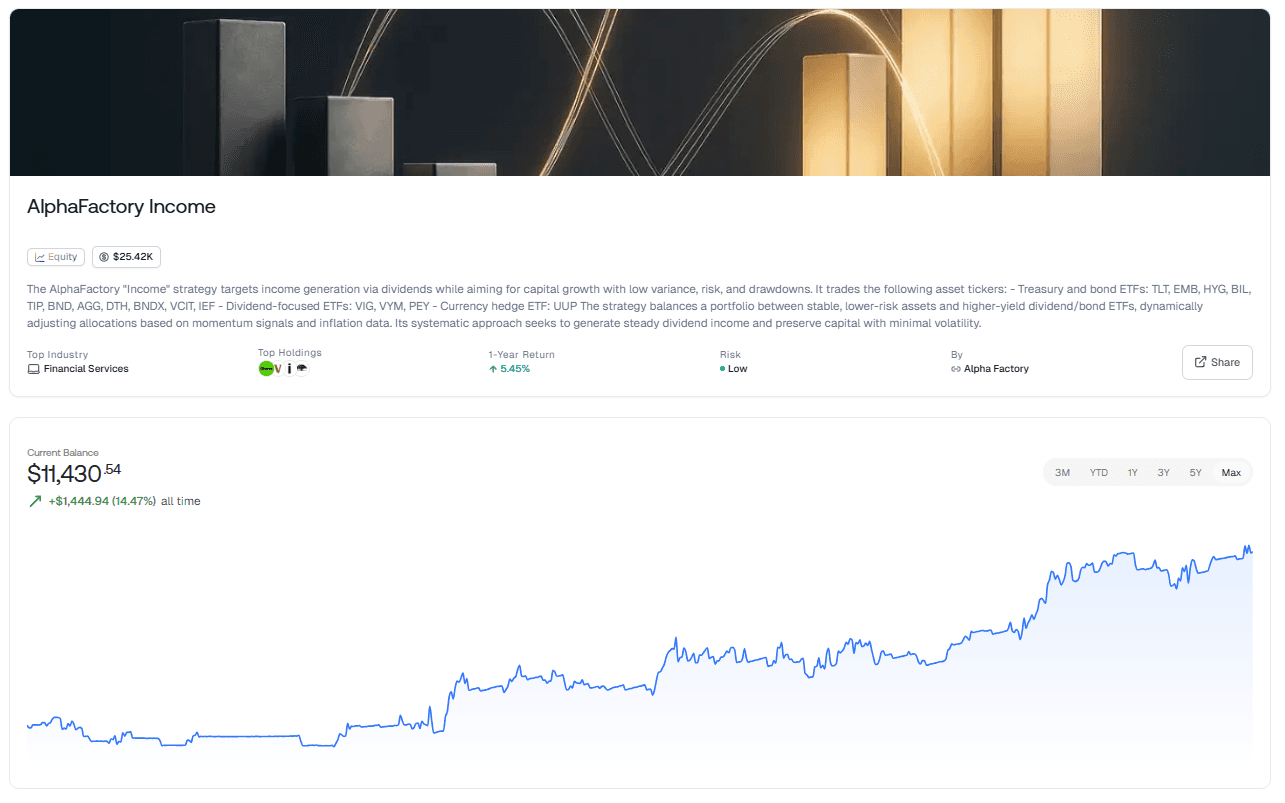

Ready to Put This Thesis to Work? Meet AlphaFactory Income

If this rotation thesis resonates with you, the logical next question is execution. Identifying the right macro environment is only half the battle — capturing it systematically, without the emotional interference that causes most investors to buy late and sell early, is where real returns are made.

That is exactly what AlphaFactory Income is built to do.

AlphaFactory Income is an automated trading strategy on Surmount, purpose-built for the environment described in this article.

It targets steady income generation through dividends and bonds while actively pursuing capital growth — all with a disciplined focus on low variance, minimal drawdowns, and controlled risk.

The strategy trades a carefully selected universe of dividend-focused ETFs including VIG, VYM, and PEY alongside a diversified mix of treasury and bond ETFs spanning TLT, HYG, TIP, BND, AGG, and others. A currency hedge via UUP adds another layer of macro-aware protection.

What makes it genuinely different is its dynamic allocation engine. Rather than holding a static portfolio, AlphaFactory Income continuously adjusts its positioning based on momentum signals and live inflation data — meaning it is systematically doing what this article argues investors should be doing manually: rotating toward income and stability when the macro environment demands it, and leaning into growth when conditions support it.

This is not passive dividend indexing. It is an active, rules-based strategy that operationalizes the contrarian thesis — steady income, capital preservation, and intelligent repositioning — without requiring you to watch every Fed statement or rebalance your portfolio by hand.

For investors who believe, as this article argues, that the next phase of the market rewards discipline over speculation and income over momentum, AlphaFactory Income is worth a serious look.

Explore AlphaFactory Income on Surmount and let the strategy do the rotating for you.

NEVER MISS A THING!

Subscribe and get freshly baked articles. Join the community!

Join the newsletter to receive the latest updates in your inbox.