Geopolitical "Hopium" vs. Ground Realities

The most dangerous moment in the market is when the absence of bad news is mistaken for the presence of good news.

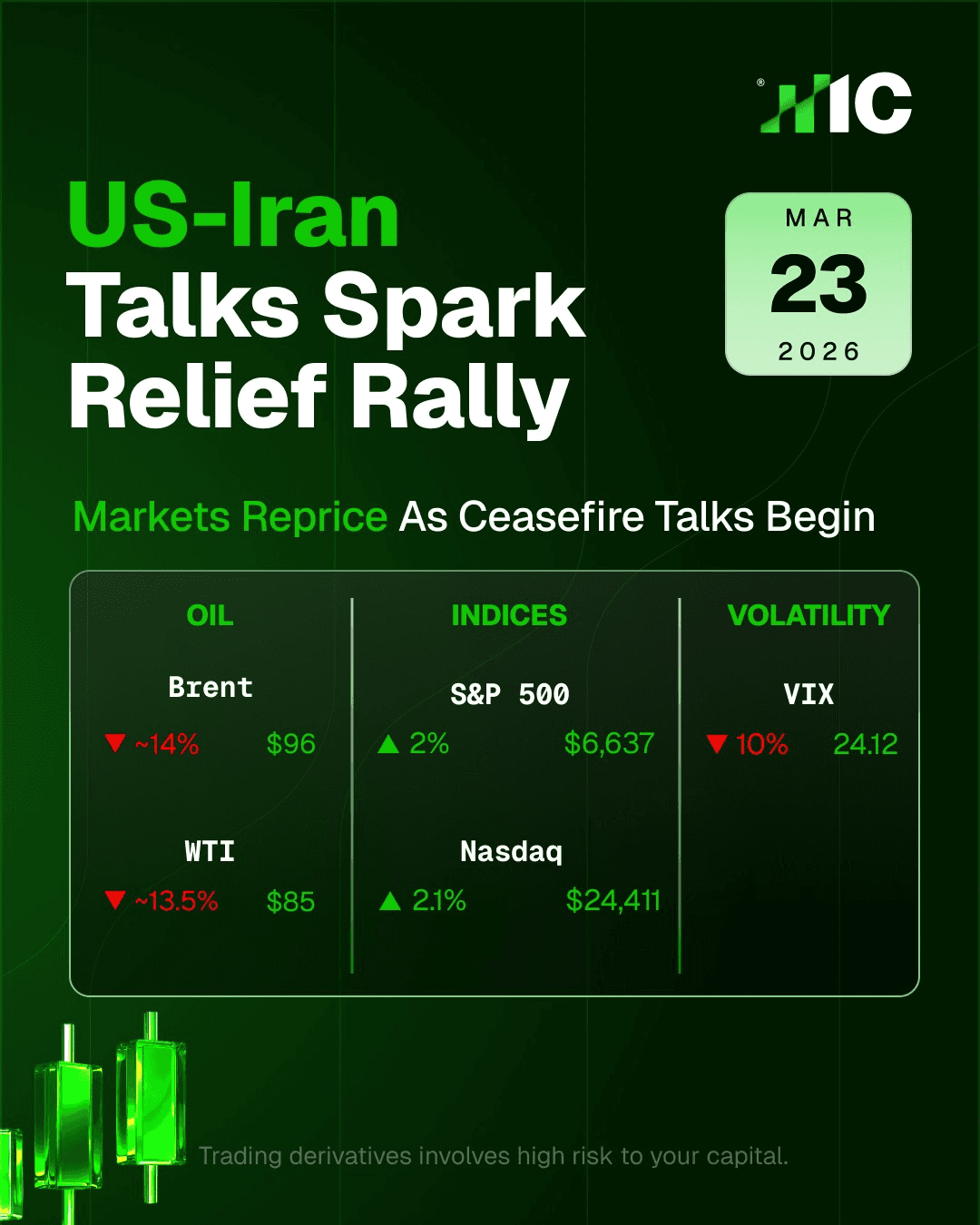

Last weekend, in Islamabad, the world watched as twenty-one hours of high-stakes diplomacy dissolved into a stalemate. The "Islamabad Talks" were framed by the media as a historic breakthrough, the first direct engagement of this magnitude in nearly half a century. But for the contrarian investor, the headline was actually just noise, that a large segment of the market was falling for. While the market spent the preceding week rallying on "hopium," betting on a ceasefire and a return to normalcy, the physical reality was far grimmer.

Despite clearing eight out of ten hurdles, the talks collapsed on the two most critical friction points, which were of course nuclear concessions and the sovereignty of the Strait of Hormuz. This was followed by a Truth Social post by President Trump declaring plans to leverage the US navy to enforce a blockade across the Sea of Hormuz.

Investors have spent the last several days conditioning themselves to believe that geopolitical tensions are merely "noise" to be bought. They looked at a 2% gain in the S&P 500 and assumed the crisis was behind us, ignoring the fact that diplomatic "progress" is binary, it either results in a signed deal or it results in escalation. By choosing to price in the former, the market left itself completely unhedged for the latter.

For those who followed the herd into the "relief rally," the realization is coming too late: you cannot feed a supply chain on optimism, and you cannot power a global economy on failed communiqués.

In this blog post, I will explain why the market’s current obsession with "geopolitical de-escalation" is fundamentally at odds with the physical constraints of the energy sector. We will dive into the dangerous divergence between paper assets and physical barrels, explore the "stealth tax" of sustained triple-digit oil, and identify the specific credit indicators that suggest the equity rally is built on a foundation of sand.

Why Supply Chains Don't Trade on Sentiment

It’s important to remind ourselves that inflation is not in fact just a psychological phenomenon that can be cured by a "good vibe" in the Middle East. Inflation, and specifically energy-driven inflation, is governed by the laws of physics and the cold reality of the global supply chain.

The Molecule Doesn't Care About the Memo

Wall Street may be circulating memos suggesting that the conflict is "priced in," but the physical world hasn't received the message. When oil sustains a price near $100 per barrel, it acts as a non-negotiable tax on movement. Every ship crossing the Atlantic, every truck delivering semiconductors, and every plane in the sky faces a literal increase in the cost of existence. Unlike a stock price, which arguably can be seen as a collective hallucination of future value (just look at Tesla), the price of a barrel of oil is a present-day cost of production.

The Stealth Interest Rate Hike

The market is currently celebrating a "pause" in Fed activity, but $100 oil is essentially a "Shadow Rate Hike." As Goldman Sachs recently pointed out, the current dynamic can drain discretionary income from the consumer and destroy corporate margins.

If oil persists at these levels, the "easing financial conditions" we saw last week will be revealed as a mathematical error. You cannot have "easing conditions" while the primary input for the global economy is becoming 15% more expensive.

The Margin Squeeze No One is Looking At

In 2022, we saw that equity markets often "look through" oil spikes for 4–6 weeks before the reality of compressed margins hits earnings reports.

The "Hopium" view: High prices are transitory; companies will just pass costs to consumers.

The more grounded view: Demand destruction is real. At $100, the "pass-through" stops working, and the consumer begins limiting usage wherever necessary.

We are currently in that "Golden Hour" where the market thinks it can have its cake (high stock prices) and eat it too (high energy costs). But in the physical world, the energy always has to come from somewhere, and right now, the bills are being paid directly out of the bottom line of the S&P 500.

Preparing for the Return of Volatility

The prospects of inflation drifting back to 2% while energy costs remain at levels that historically trigger recessions remain almost non-existent, in my view. For the contrarian, therefore, the opportunity lies in the inevitable re-rating—the moment the market stops pricing in hope and starts pricing in reality.

The Credit Spread Trigger

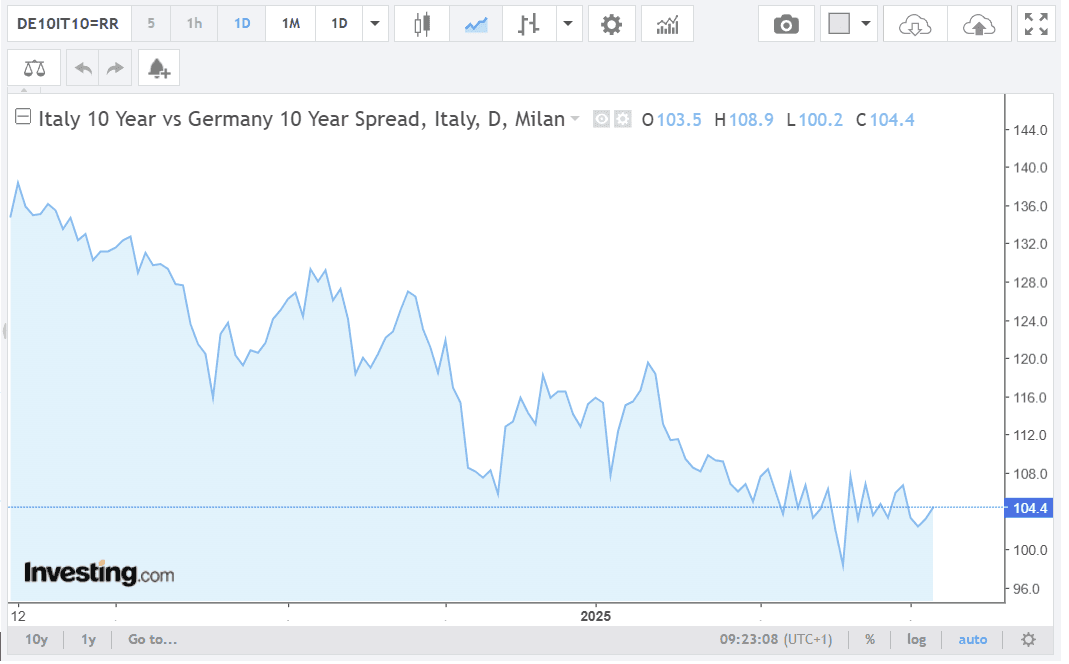

While equity traders are high-fiving over a 3.5% weekly gain, the credit markets (the "adults in the room") are actually beginning to sweat. We are watching a dangerous divergence. Historically, when oil surges, credit spreads (the premium investors demand for taking on risk) should widen almost immediately. The current delay could very well be a sign of a liquidity trap.

Watch the Italian/German 10-year yield spreads; when these begin to blow out, it serves as the definitive signal that the "Hopium" has run out and a flight to safety is imminent.

The Second-Round Effect: Central Banks Cornered

The consensus is currently betting on a "Fed Pause." However, physical reality dictates that if oil stays at $100, the Fed is boxed into a corner. Higher energy costs feed into transportation, manufacturing, and food, creating a "second round" of sticky inflation.

If the market expects rates to stay flat but oil forces them higher, the resulting "Real Rate" spike will be the hammer that cracks the equity market’s valuation multiples.

Prepare for a scenario where "bad news" for the economy is no longer "good news" for the market. In a high-oil environment, a slowing economy doesn't always bring lower rates—it brings stagflation.

Conclusion: Respect the Barrels

The ultimate contrarian move right now is to ignore the green candles on the screen and respect the barrels in the supply chain. The "Physicality" of the global economy is reasserting its dominance over the "Digitality" of the stock market. When the re-rating occurs, it won't be a slow slide; it will be a violent adjustment as the market realizes that a "transitory" energy shock was actually a structural shift.

Don't confuse a temporary easing of financial conditions with a permanent change in the economic weather. The volatility isn't gone; it's just being compressed. And the tighter the spring is wound, the harder it eventually snaps.

Beyond the Blast Radius: The "Argentina Alpha" Strategy

If you’ve followed the logic of today’s piece, you’ll get that the core of the global market is currently a hostage to geography. As long as your portfolio is tethered to the volatility of the Middle East and the fragile "Hopium" of Western credit spreads, you are playing a game where the rules change with every headline.

But what if you could exit the theater of war entirely?

While the S&P 500 white-knuckles its way through $100 oil, there is a structural opportunity emerging in a market that remains fundamentally decoupled from the Middle Eastern conflict: Argentina.

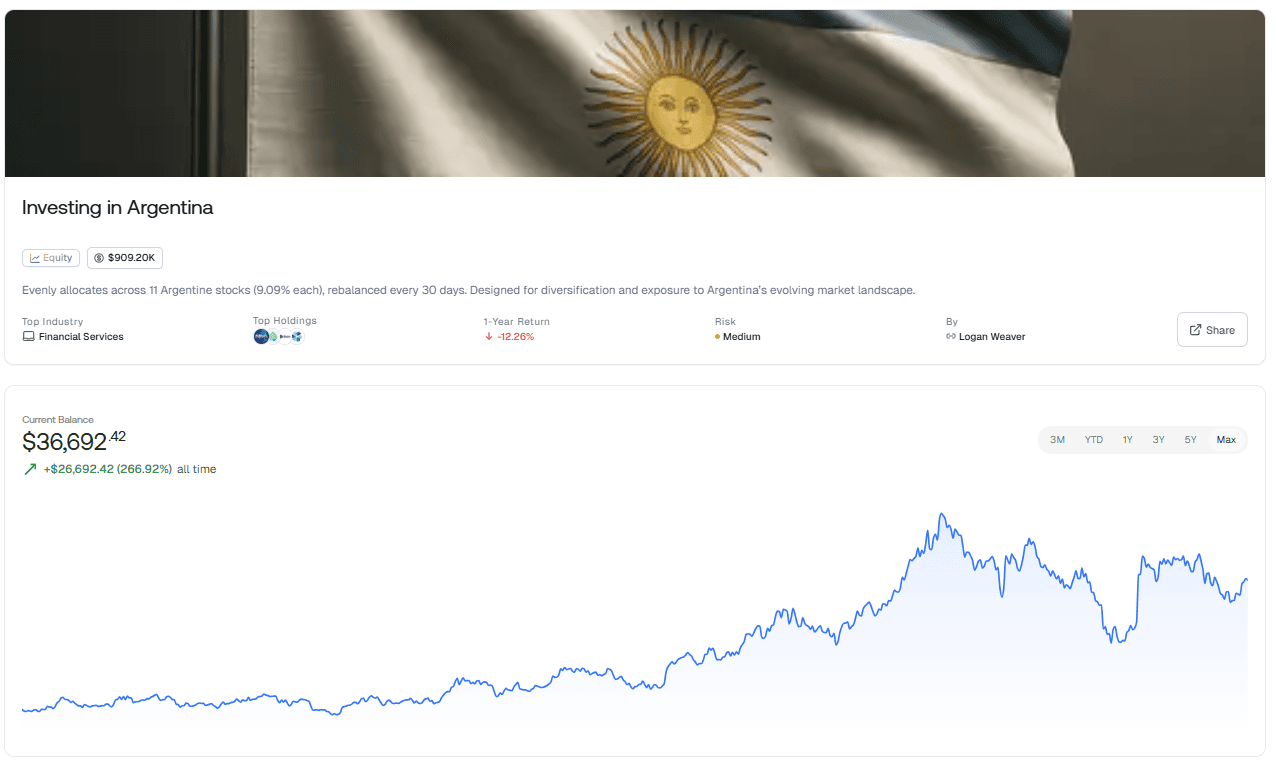

Surmount’s "Investing in Argentina" Automated Strategy

We’ve identified a way to capture the "evolving market landscape" of South America’s most interesting recovery story through a rigorous, systematic approach. This isn't about picking one winner; it’s about capturing a nation’s momentum.

Geographic Insulation: Argentina is geographically and politically isolated from the energy-driven volatility currently paralyzing the northern hemisphere.

Precision Diversification: The strategy eliminates "single-stock risk" by evenly allocating funds across 11 high-potential Argentine stocks. Each position is capped at a strict 9.09%, ensuring no single company dictates your returns.

Systematic Rebalancing: The market moves fast—so do we. The strategy automatically revisits and rebalances your allocation every 30 days, ensuring your capital stays deployed in the most efficient sectors of the Argentine economy.

The Contrarian Edge: While the crowd is fighting over the crumbs of a stagnant Eurozone and a nervous Wall Street, this strategy allows you to diversify into a variety of sectors—from energy to tech—within a market that is undergoing a historic structural shift.

Stop reacting to the war. Start investing in the recovery.

Don't let your portfolio be collateral damage in a conflict you can't control. Maximize your returns by pivoting to a market that doesn't care where the price of oil settles tomorrow.

[Explore the Argentina Growth Strategy on Surmount]

NEVER MISS A THING!

Subscribe and get freshly baked articles. Join the community!

Join the newsletter to receive the latest updates in your inbox.