Defensive Positioning for the "Quiet" Recession: Identifying Sectors That Thrive

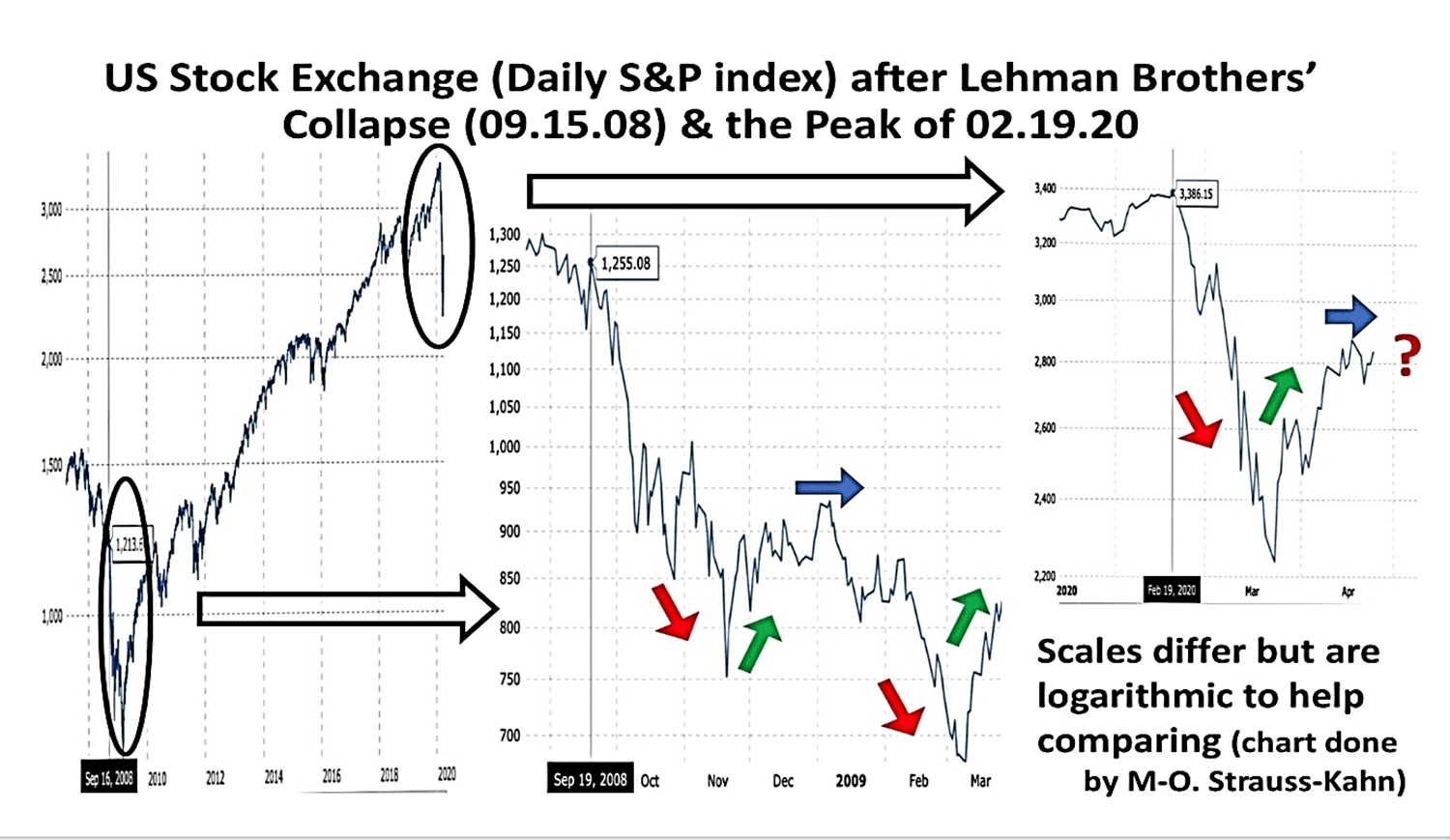

Those of us who are old enough to remember may recall how, in 2008, the world held its breath as the global financial architecture buckled under the weight of a housing collapse. It was a loud, violent explosion—a "sudden stop" that shattered portfolios and grabbed every headline from New York to Tokyo. Relatively more recently, in 2020, we saw another explosion, this time triggered by a biological exogenous shock that forced the world to turn the lights off overnight.

In each of these cases, the markets reacted to a singular, seismic event. There was a "before" and an "after" that could be circled on a calendar. Of course, it is exactly these cinematic collapses that investors are trained to look for. We wait for the "big one," the Lehman moment, or the black swan that sends the VIX screaming into the stratosphere.

Right now, with the crisis alongside the Strait of Hormuz, which shows no clear signs of de-escalation, and oil prices acting as a persistent tax on an already weary consumer, many are scanning the horizon for that same kind of singular, explosive "event." They are looking for a spectacular bank failure or a vertical drop in the S&P 500 to validate what their gut is telling them.

But they are looking for the wrong kind of ghost.

The data actually seems to suggest, as we will explore in this blog, that we aren't facing a sudden cardiac arrest of the markets, but rather a slow, systemic atrophy—a "Quiet" Recession.

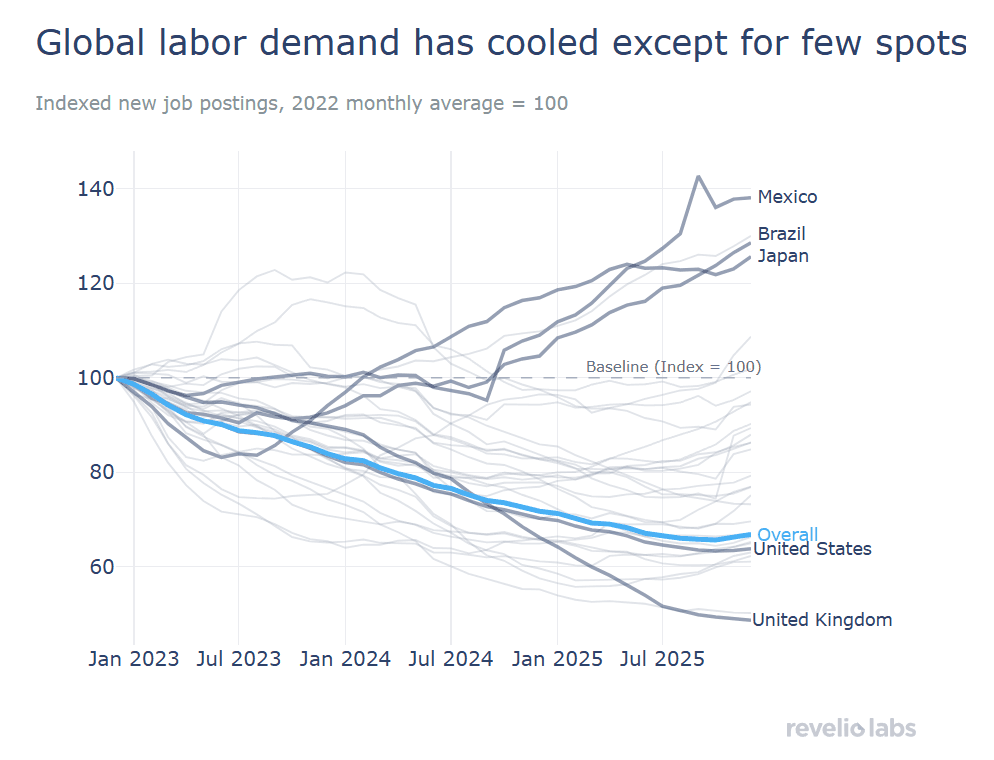

Unlike 2008 or 2020, this downturn isn't characterized by a "sudden stop," but by a "gradual freezing." It is an economic ossification where the gears of upward mobility and corporate expansion simply cease to turn. We see it in the job gains figures that have quietly slid to 2011 levels while the mainstream media was busy celebrating a "soft landing." We see it in the quit rates, which have plummeted to levels not seen since 2015 (outside of the pandemic).

When workers stop quitting, it’s usually because they are paralyzed by the "economic imprisonment" of a cooling labor market. This lack of churn is the hallmark of the Quiet Recession. It is an environment where hiring freezes replace mass layoffs, where "staying put" replaces "leveling up," and where consumer confidence is under pressure due to the situation in the Middle East. All of this reflects a period of severe uncertainty within the economy.

As contrarians, our opportunity lies in recognizing that stagnation is its own kind of crisis. While the "loud" investors wait for a signal that may never come in the form they expect, the "quiet" data points (such as the collapse of top-quartile wage growth and the multi-decade lows in labor participation) are already screaming. The recession hasn't just been "predicted" for 2026; for the American worker and the discerning investor, the cracking of the foundation may have already begun.

The "Safety in Stagnation" Sectors

In a "Quiet Recession," the traditional playbook of "buying the dip" in high-beta growth stocks is a trap. When the labor market is in a defensive crouch—marked by the 2011-level hiring lows and the 2015-level quit rates pointed to above, the velocity of money is what slows down first. Capital ends up migrating toward stability and structural efficiency.

For the contrarian investor, "Safety in Stagnation" isn't just hiding in cash; it’s also about identifying the sectors that thrive when the broader economy stops moving.

1. The "Lock-In" Economy: High Switching Cost Moats

When consumer confidence is at the abysmal levels we’ve seen in 2025 and 2026, both households and corporations stop "shopping around." The friction of changing a service provider becomes a psychological and financial barrier.

Mission-Critical SaaS and Infrastructure: We are looking for companies that are "embedded" into the workflow of their clients. If a company is already struggling with low hiring and high costs, the last thing they will do is undergo a risky, expensive migration to a new software suite or utility provider.

The Investment Play: Focus on firms with high Net Retention Rates (NRR). In a stagnation phase, a company that can grow revenue by 5–10% simply by upselling its existing, "captured" base is worth more than a hyper-growth firm that relies on a constant stream of new (and now non-existent) customers.

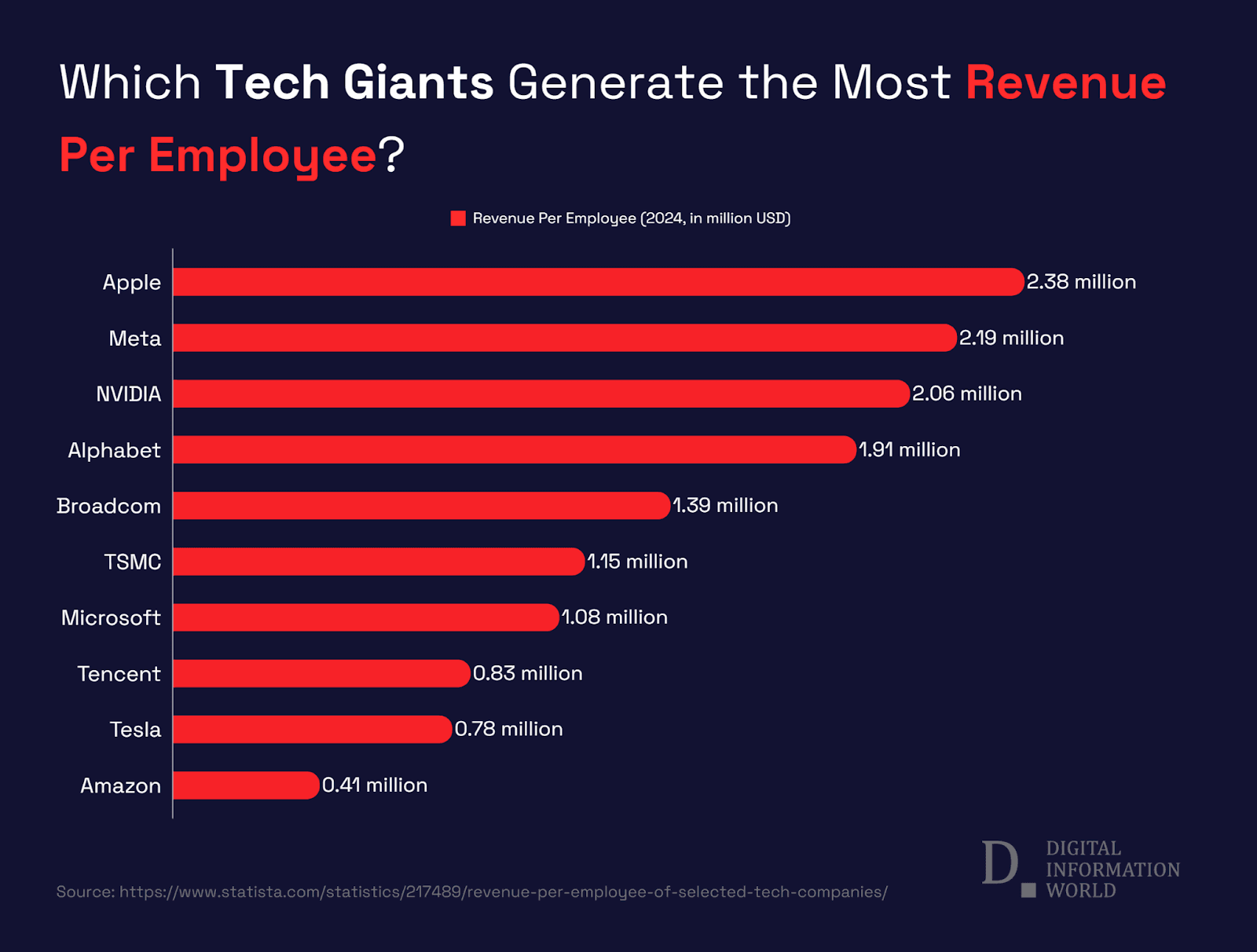

2. High Operating Leverage: Growth Without Headcount

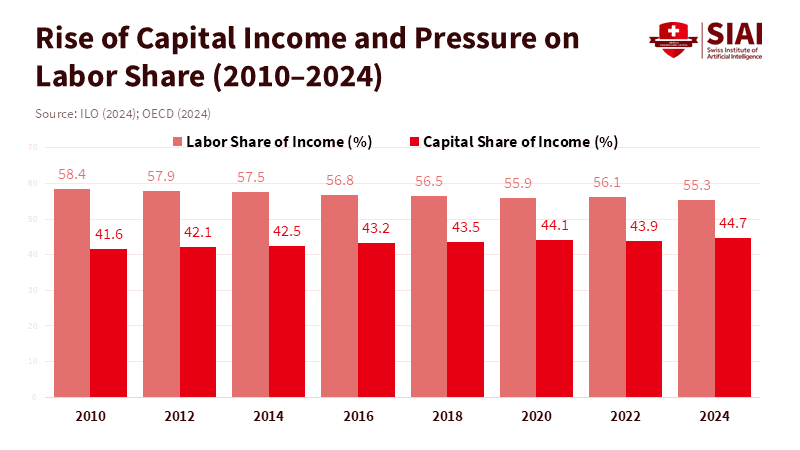

The falling labor share of income trend is a grim reality for workers, but a signal for investors. The "Quiet Recession" favors companies that have already decoupled their revenue growth from their headcount growth.

The Headcount Neutrality Factor: In a typical bull market, companies hire to grow. In a stagnation, the winners are those that can scale via automation and software-driven efficiencies. If a company can maintain its output while the "Temp Help" sector collapses around it, its margins will actually expand as labor's bargaining power wanes.

The Investment Play: Look for sectors with the highest Revenue per Employee. When the labor market "cracks quietly," companies with low labor intensity are shielded from the wage-growth resistance you noted in the top quartiles.

3. Counter-Cyclical Staples: The "Repair" vs. "Replace" Economy

When the "Non-Farm Quits" data is depressed, it signals a workforce that is staying put out of fear. This fear manifests in the "Repair over Replace" mentality.

Deferred Maintenance and DIY: Instead of buying a new home (difficult with high rates) or a new car, the "trapped" consumer invests in maintaining what they already own. This benefits specialized retail in the automotive aftermarket and home improvement sectors that cater to maintenance rather than renovation.

The Investment Play: Identify "needs-based" consumables. While luxury and discretionary quartiles see wage resistance, the demand for healthcare, basic utilities, and discount household staples remains inelastic. In fact, these sectors often see margin expansion during stagnation as their input costs (commodity prices/labor) soften while their pricing power remains intact due to the "essential" nature of their goods.

Most investors view a "frozen" labor market as a precursor to a crash and flee to the sidelines. The sophisticated play is recognizing that stagnation creates a premium on certainty. The sectors above don't need a "soft landing" or a Fed pivot to survive; they are designed to harvest value from an economy that is standing still.

The "Labor Share" Arbitrage: Playing the Structural Shift

A falling labor share of income is a strong signal to adjust one’s capital allocation. As we witness the third quarter of 2025 marking the lowest labor share on record, we are seeing a fundamental decoupling of corporate productivity from human payrolls. If the "quiet" recession is defined by a labor market that is freezing over, the investment play is to own the infrastructure that makes those wages unnecessary.

From "Human Capital" to "Hard Automation"

The data is clear: software and automation are no longer just "efficiencies"—they are the primary drivers of the economy. In an environment where the labor force participation rate has plummeted to 1977 levels, companies that rely on massive headcounts are facing a terminal margin squeeze.

Pivot toward firms with high revenue per employee. When hiring data worsens (as seen in the 3.3% hire rate), companies that have already transitioned to "lights-out" operations or AI-integrated workflows are insulated from the labor friction that will bankrupted their legacy competitors.

The "Bargaining Power" Vacuum

There has also been a noticeable decline in union participation, over the years. Obviously, this does not bode well for the labor floor. While this creates long-term consumer instability, in the short term, it creates an arbitrage opportunity in specific sub-sectors.

The strategy is to identify "Essential Monopolies." These are large-cap companies in sectors like logistics or specialized manufacturing that control their markets so effectively that they dictate terms to a disorganized workforce. While "trickle-down" may be a fiction for the worker, the retention of productivity gains at the corporate level is a very real fact for the shareholder.

The Defensive Exit: Liquidity as the Ultimate Hedge

The final component of this arbitrage is recognizing that a "Quiet" recession eventually leads to a "Loud" policy shift. When consumer confidence hits the abysmal levels we are seeing in 2026, the political pressure for a massive shift in tax policy or a Federal Reserve pivot becomes a "when," not an "if."

Maintain a "Dry Powder" ratio that is uncomfortably high for most. The goal of defensive positioning in the labor-share shift is to stay liquid enough to snap up distressed high-quality assets when the "cracks" in the labor market finally lead to a headline-grabbing break. We are betting on the machines today, so we have the capital to buy the blood in the streets tomorrow.

The Bottom Line: Don't invest in the economy you want (one with robust wage growth and high participation); invest in the one the data shows we have—a structural shift where capital is aggressively cannibalizing labor's piece of the pie.

The "Quiet" Recession Exit: Let’s Look South

While the U.S. labor market enters a period of defensive "ossification," the savvy contrarian knows that capital doesn't just disappear—it migrates to where the structural "cracks" are being mended, not widening.

If the domestic play is about Safety in Stagnation, the offensive play is about Capturing the Inflection.

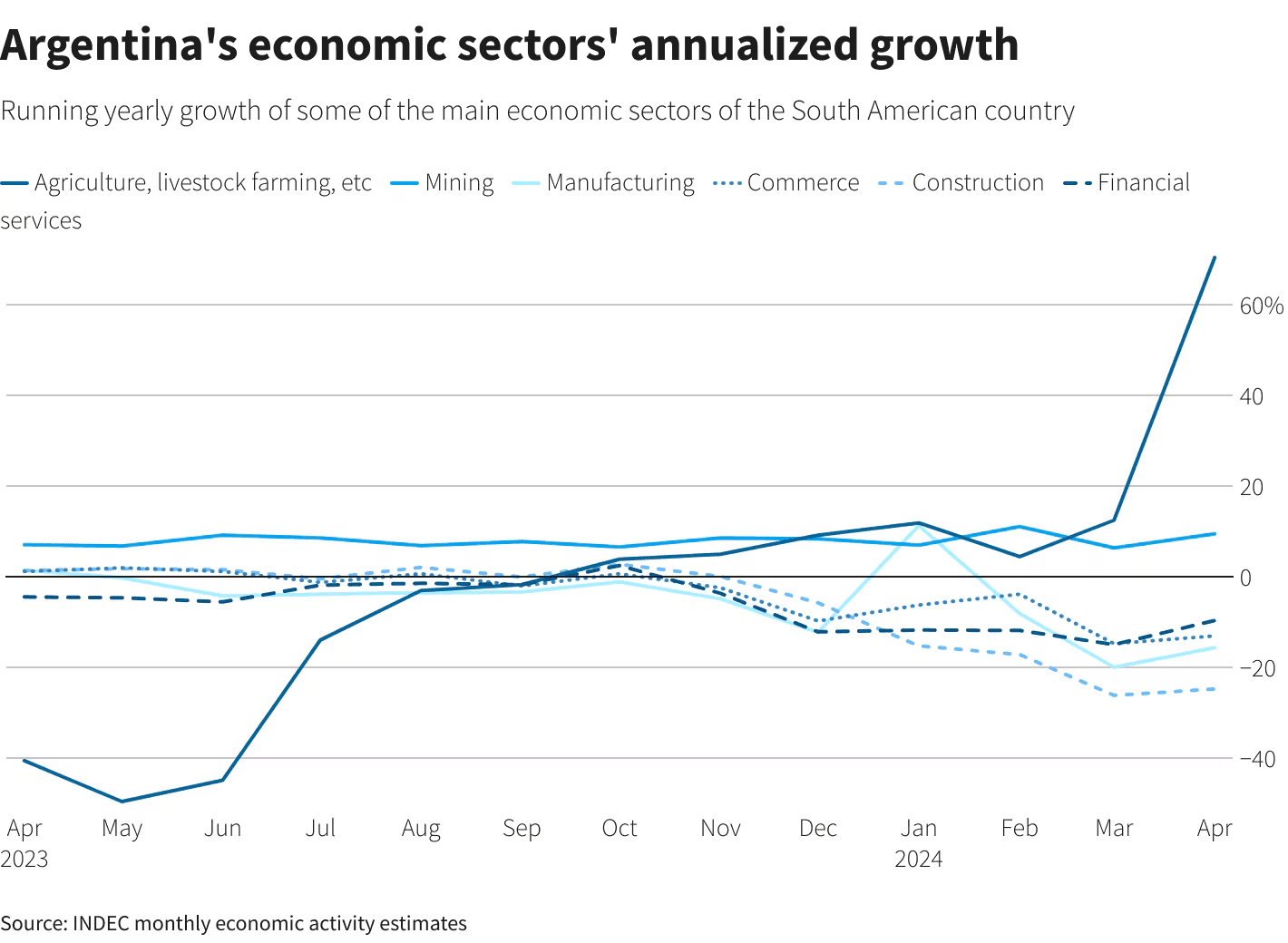

As we watch the U.S. labor share of income hit record lows and hiring hit a decade-long freeze, a massive divergence is appearing in the Southern Hemisphere. In Argentina, the narrative is the exact opposite: we are witnessing the birth of a "Capital-First" recovery.

Similarly, while U.S. workers are "struggling in silence," Argentina has just enacted the Labor Modernization Law, specifically designed to slash employer costs and ignite high-growth sectors like energy and lithium mining.

The Opportunity: Automated Exposure to the Argentine Inflection

To capitalize on this divergence without the emotional baggage of manual trading, one of the optimal ways to win is Surmount’s automated Investing in Argentina trade strategy.

This isn't a speculative bet on a single "moonshot" stock. It is a calculated, systematic capture of a nation’s structural pivot.

Precision Diversification: The algorithm maintains a razor-sharp, equal-weighted allocation (9.09% each) across 11 of the most influential Argentine equities.

Systematic Rebalancing: Every 30 days, the strategy automatically re-aligns. This ensures you are constantly harvesting gains from high-fliers in the booming agriculture and energy sectors (like the 50.8% expansion we’ve seen in fisheries) and rotating back into undervalued laggards.

The Contrarian Edge: While the "Quiet Recession" at home creates a ceiling for growth, Argentina's "jobless recovery" is actually a boon for shareholders—GDP is projected to hit 4.3% in 2026 driven by capital-intensive sectors that prioritize margins over massive payrolls.

Don't let your portfolio get trapped in the U.S. hiring freeze.

If you want to maximize returns while the domestic economy "quietly" resets, you need exposure to markets where the structural reforms are actually moving in favor of capital.

[Explore the Investing in Argentina Strategy on Surmount]

NEVER MISS A THING!

Subscribe and get freshly baked articles. Join the community!

Join the newsletter to receive the latest updates in your inbox.