Geopolitical Premium: How Much of Today's Commodity Price Is Real?

Commodity prices look strong. Oil holds above levels that make energy executives comfortable. Metals are bid up. Coal, iron ore, agricultural inputs — the tape looks healthy, and the narrative around it sounds compelling. War and ‘stone age’ rhetoric in the Middle East. Sanctions on major producers. Shipping lanes under pressure. Of course prices are high.

But here is something almost no one is asking. How much of that price is real?

Not real in the sense of whether you can observe it on a terminal, because of course you can. Real in the sense of whether it reflects genuine, durable demand for the physical commodity, or whether it reflects something far more ephemeral: the market's collective anxiety about what might happen next.

These are two entirely different things, and confusing them is one of the most reliable ways to buy high and wonder why.

Two Prices, Not One

Every commodity price you see today is actually two prices layered on top of each other. The first is the structural price, which is the level justified by underlying supply and demand, production costs, inventory cycles, and long-run consumption trends. This is the price that would exist in a world where geopolitical variables were flat.

The second is the fear premium the additional margin the market charges because a pipeline might get hit, a sanction might tighten, or a conflict might escalate. This premium is real in the short run. It moves markets. It drives earnings surprises. It makes commodity-heavy portfolios look like genius.

But these conditions are never permanent.

A good way to think about the fear premium is that it is rented, and not owned. Most investors buying into commodity strength today are paying rent without realising it.

The goal of this post is not to predict when the next ceasefire happens or call the top in oil. Macro timing is generally a fool's errand. The goal is more useful than that, which is to give you a framework for decomposing what you are actually buying when you buy a commodity-exposed asset at today's prices, and to make the contrarian case that the real opportunity right now may sit precisely where the fear premium is not. This would be the businesses that have been quietly penalised by the same geopolitical environment everyone else is crowding into.

Anatomy of a Fear Premium — How Geopolitics Inflates Commodity Prices

Geopolitical shocks do not inflate commodity prices randomly. They follow a fairly consistent playbook, and understanding that playbook is the first step to not being its victim.

The most direct mechanism is supply disruption fear. When conflict breaks out near a major producing region, the market does not wait to see whether supply is actually interrupted. It prices in the possibility immediately. Oil famously spikes on news of Middle Eastern tension regardless of whether a single barrel of production is affected. The market is not irrational to do this — the risk is real. The mistake is treating the spike as a new fundamental floor rather than a risk premium that will compress as the situation clarifies.

The second mechanism is sanctions and trade route instability. When major producing nations face export restrictions, or when key shipping corridors become contested, the cost of getting commodities from where they are produced to where they are consumed rises sharply. This is real friction with real price effects. But sanctions regimes evolve, trade flows reroute, and what looked like a permanent supply constraint often turns out to be a temporary disruption that the market overpriced.

The third, and most insidious, mechanism is speculative positioning. Hedge funds, commodity traders, and momentum strategies pile into commodity assets when geopolitical headlines are hot. This is not fundamental buying — it is narrative buying. It amplifies the price move well beyond what the underlying supply-demand shift would justify, and it creates a positioning overhang that unwinds sharply when the narrative cools.

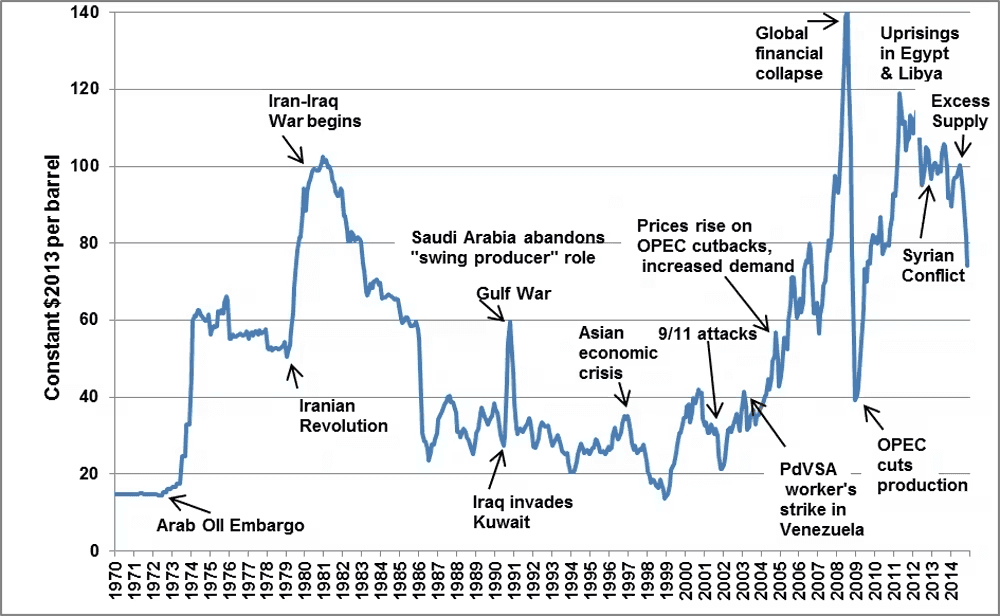

History Rhymes With Uncomfortable Regularity

The historical record on geopolitical commodity premiums is remarkably consistent: they spike fast, feel permanent, and mean-revert faster than almost anyone expects.

The 1970s oil shocks are the canonical example, but they are also the exception — those events reflected genuine structural shifts in the global energy order. More instructive are the episodes that felt like structural shifts but were not.

The Gulf War in 1990 sent oil prices surging. Within months of the conflict's resolution, prices had given back the majority of the spike. The post-9/11 commodity premium unwound as it became clear that global supply chains were more resilient than the panic implied. The 2022 energy shock following the invasion of Ukraine drove European gas prices to levels that seemed to price in permanent scarcity. European industry adapted, LNG supply expanded, and prices collapsed from their peaks with a speed that caught most positioned investors badly offside.

The pattern is not that geopolitical events do not matter. They do. The pattern is that the premium the market assigns to those events almost always exceeds what the eventual fundamental impact justifies.

A Framework for Estimating the Fear Premium

You do not need a PhD in commodity economics to apply a rough decomposition. Ask three questions.

First, what is the long-run cost of production for this commodity? This is your anchor. In competitive commodity markets, prices revert to marginal cost of production over a cycle. If current prices are dramatically above that level, something other than fundamentals is doing the work.

Second, what has changed in the actual supply-demand balance? Strip away the headlines and look at inventory data, production figures, and demand growth. If the physical market is not as tight as the price implies, the gap is largely sentiment and positioning.

Third, what is the positioning picture? If speculative long positioning in futures markets is at elevated levels, you are looking at a market where a lot of the fear is already priced and a lot of the upside has already been taken. The asymmetry at that point is uncomfortable.

None of this tells you when the premium fades. But it tells you clearly whether you are buying fundamentals or buying fear. That distinction matters enormously for expected returns over a 2-3 year horizon.

What Happens When the Premium Fades — And How to Position Now

When geopolitical fear premiums fade, they do not gracefully trickle lower. They tend to unwind in lurches — a ceasefire announcement, a diplomatic breakthrough, a string of weeks where the feared escalation simply does not materialise, and suddenly the positioning that supported elevated prices has no fundamental underpinning. The exits get crowded.

The investors who suffer most in these episodes are not those who misjudged the geopolitics. Everyone misjudges geopolitics — it is inherently unpredictable. The investors who suffer most are those who bought commodity-heavy assets at peak fear and implicitly underwrote the premium as a permanent feature of the price. They confused the level of the price with the quality of the price.

Commodity-heavy portfolios that looked like outperformance during the fear phase frequently give back a disproportionate amount during the normalisation phase. The underlying businesses have not gotten worse. The narrative has just changed.

The Quiet Re-Rating That Nobody Talks About

Here is the part of this story that gets almost no attention: when geopolitical premiums compress, the relative winners are often the diversified, non-resource businesses that were penalised by the same macro environment.

Think about what happens when commodity prices are running hot on fear. Capital flows toward the assets with the most direct commodity exposure. Resources companies, energy majors, and commodity traders attract the multiple expansion and the inflows. Businesses with more diversified, operationally-driven earnings profiles get treated as boring — fine for what they are, but not the place to be when the commodity trade is working.

When the premium fades, the re-rating runs in the opposite direction. The businesses that never needed geopolitical tailwinds to grow — the ones compounding quietly through organic growth, new investments, and operational improvements — suddenly look attractive again on a relative basis. Their earnings did not collapse with the commodity price because their earnings were never built on it. And they were cheap going in, because the market was distracted.

This is a repeatable dynamic. It is not a prediction about any specific event. It is a structural feature of how capital rotates around geopolitical cycles.

(Alternatively, there is also sometimes a ‘hopium’ at play, in these dynamics, which we’ve written an insightful piece about, here)

Where the Contrarian Opportunity Lives

The practical implication is this: the time to position for the premium unwind is not after it happens. By then, the commodity stocks have already sold off and the re-rating in diversified businesses has already begun. The time to position is when the fear is loudest and the consensus is most crowded into commodity exposure — which is roughly where we are today.

The contrarian investor is not making a call on geopolitics. That would be foolish. The contrarian investor is asking a different question: if current commodity prices already embed a significant fear premium, what is the expected return of being long that premium versus being long businesses that will grow regardless of whether the fear materialises?

Framed that way, the answer is usually not close.

Most investors look at a commodity price chart today and feel comfort. It is going up. The narrative explains why. The trade is crowded and therefore feels validated — there is safety in company.

But conviction and correctness are not the same thing. Crowded trades with a strong narrative and geopolitical justification have a long historical track record of eventually delivering very poor returns to the investors who arrived late and paid for the fear.

The better question to be asking right now is not how to get more exposure to what has already run. It is where, in this environment, quality is being mispriced because everyone is looking somewhere else.

That is where contrarian investors earn their returns. Not from being right about what will happen — but from not paying rent on what everyone else fears.

Putting the Insight to Work

Reading about geopolitical premiums and mispriced quality is one thing. Positioning your portfolio to actually benefit from it is another.

The core argument of this piece is that in noisy, fear-driven markets, the investors who win are the ones making disciplined, data-driven decisions — not the ones reacting to headlines. That is easy to say and genuinely hard to execute. Emotions, narrative momentum, and the discomfort of going against the crowd make it extraordinarily difficult to act on contrarian logic in real time.

That is exactly why we want to introduce you to a strategy built for this environment.

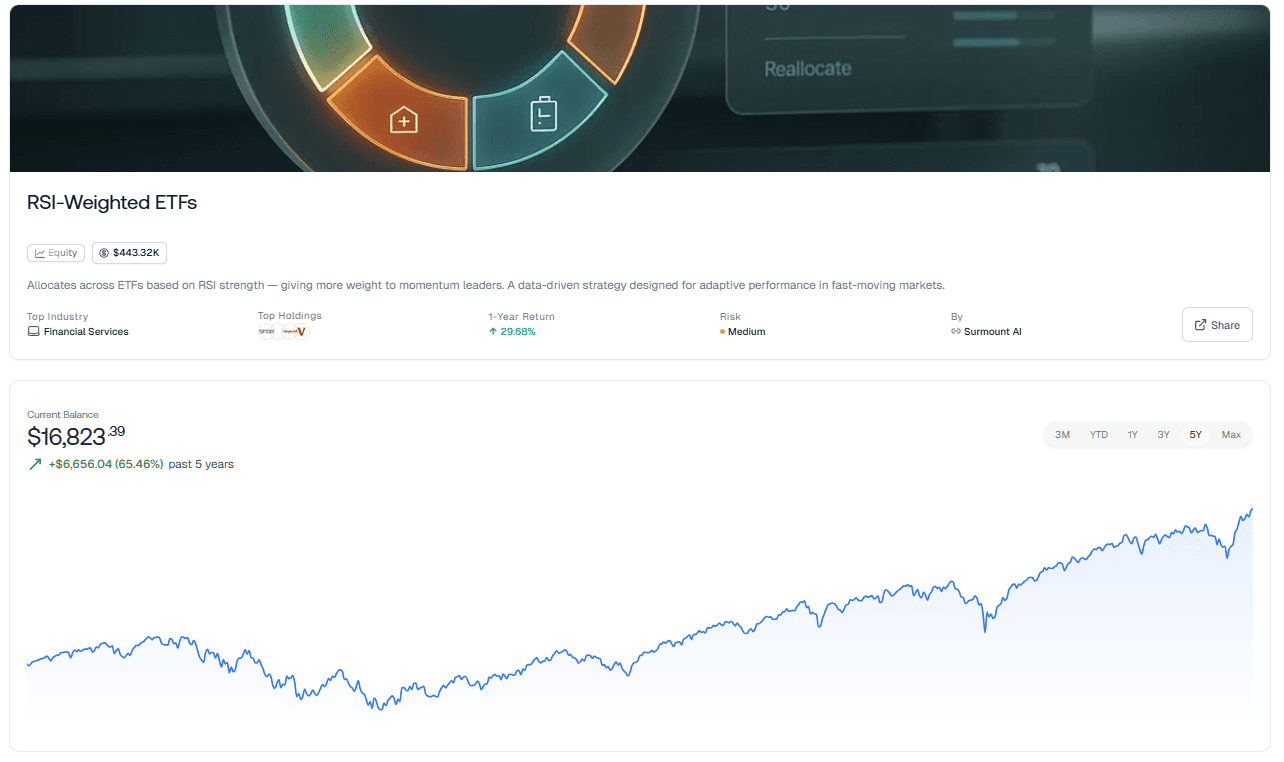

Introducing the RSI-Weighted ETFs Strategy on Surmount

While most investors are glued to geopolitical headlines trying to guess which way commodity prices move next, this automated strategy is doing something far more rigorous: it is reading the actual strength of the market itself.

The RSI-Weighted ETFs strategy uses the Relative Strength Index — one of the most battle-tested momentum indicators in quantitative investing — to determine where capital should be allocated at any given moment. Rather than making binary bets on individual sectors or macro calls, it allocates proportionally across ETFs based on their RSI values. The stronger the momentum signal, the greater the weight. The weaker the signal, the less exposure you carry.

What does this mean in practice? When the crowded commodity trade starts to lose momentum — when the fear premium begins its inevitable compression — the strategy detects the shift and reweights accordingly. You are not waiting for a pundit to tell you the cycle has turned. The data tells you first.

Why This Strategy Fits the Moment

The entire thesis of this blog comes down to one idea: price is not always value, and narrative is not always signal. The RSI-Weighted ETFs strategy is built on exactly that premise. It does not care about the story. It does not care whether oil should be high because of Middle East tension. It cares about what the market is actually doing — and it positions accordingly.

In fast-moving, macro-driven markets like the one we are navigating right now, that kind of adaptive, rules-based discipline is not just useful. It is a genuine edge.

This is the contrarian approach made systematic. No emotion. No narrative capture. Just clean, data-driven allocation that adjusts as conditions evolve.

Ready to Let the Data Lead?

If this piece has convinced you that the market is mispricing risk — and that the real opportunity lies in cutting through the noise with discipline — the RSI-Weighted ETFs strategy on Surmount is designed precisely for investors who think this way.

Explore the RSI-Weighted ETFs strategy on Surmount and see how a momentum-driven, adaptive approach can help you stay ahead of the rotation — not behind it.

Don't pay rent on someone else's fear. Let the data do the work.

NEVER MISS A THING!

Subscribe and get freshly baked articles. Join the community!

Join the newsletter to receive the latest updates in your inbox.