For the past several years, the global geopolitical map has looked like a series of cascading "black swans." From the grinding war of attrition in Eastern Europe to the volatile flashpoints across the Middle East and the simmering tensions in the South China Sea, conflict is no longer a tail risk—it is the baseline.

While the world did enjoy a brief, post-Cold War era of "peace dividends" and globalized harmony, that era has arguably been buried, considering the increasing frequency of armed conflict.

The eruption of conflict we see unfolding in the Middle East between the US-Israel alliance and Iran is seemingly shaping up to be one of the most extreme stress tests for global markets since the 1970s.

Oil prices have already surged on fears of supply disruption, while maritime insurers have essentially cancelled the war risk cover for the Gulf zone.

For investors, the muscle memory is nearly automatic: buy the "bullets and barrels." The reflexive trade in this environment is to go long on defense primes and energy majors, betting that a world on fire will inevitably burn through more munitions and crude oil.

But there is a flaw in this consensus. As the confrontation between the US-Israel alliance and Iran threatens to metastasize, the "obvious" trades are becoming dangerously crowded and expensive. We are entering a phase where the most profitable move may be to position yourself to survive the economic fallout.

The Crowded War Trade: When the "Obvious" Becomes a Trap

When we get to a point where even your local florist is claiming they’re “long Lockheed” and your uncle is texting you about Brent Crude futures, the alpha has already left the building. In the world of contrarian investing, consensus is the enemy of profit.

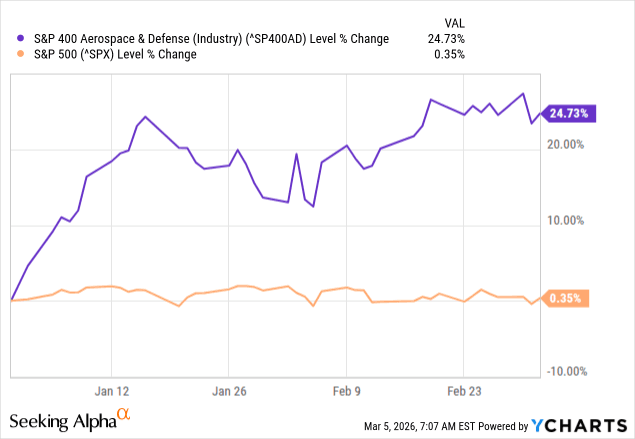

Since the beginning of the current year, the S&P Aerospace and Defense has massively outperformed the broader market:

This typically happens because when a geopolitical flashpoint ignites, the "War Playbook" is executed with such algorithmic speed that the risk-premium is often fully captured within the first 48 hours. By the time the retail crowd arrives, they aren’t buying a hedge; they are buying the top of a parabolic move fueled by fear.

The traditional war trade, which is buying defense contractors and energy producers, relies on a linear projection:

Conflict = More Spending + Higher Prices.

But markets are rarely linear. Here is why the crowded trade often stalls:

Priced to Perfection: Large-cap defense stocks like LMT or GD trade on multi-year government contracts. A new conflict doesn't instantly double their production capacity; it merely confirms the demand that is likely already baked into their P/E ratios.

The "Peace Scare": When a trade is this crowded, even a rumor of a ceasefire or a diplomatic breakthrough can trigger a massive liquidation. The downside risk of "peace breaking out" is often greater than the upside potential of the war escalating further.

Margin Compression: While people focus on the top-line revenue for defense firms, they forget the bottom line. War causes raw material shortages and labor spikes. If a company's input costs rise faster than its fixed-price government contracts allow for, the "war trade" can actually result in lower earnings.

The Liquidity Trap

When you follow the crowd into high-beta volatility, you surrender your most valuable asset: Optionality. If the conflict leads to a broader market contagion or a credit crunch, the investor "long on Lockheed" is trapped in a falling asset with no liquidity to buy the resulting blood in the streets.

By pivoting to cash, and specifically short-term T-Bills, you aren't just avoiding a crowded room; you are positioned at the exit with a full wallet while everyone else is fighting for the door.

The Math of the "Risk-Free" Pivot

In a low-rate environment, cash is "trash" because the opportunity cost of holding it is astronomical. But in a high-rate geopolitical cycle, the math flips. To a contrarian, the Risk-Free Rate is the most important number in the world because it represents the "Hurdle."

So when you buy a defense prime like Lockheed Martin or an oil major during a conflict, you are buying high-beta volatility. You might see a 15% swing in a week based on a single drone strike or a diplomatic rumor. In contrast, short-term Treasuries currently offer a "fat" yield with a duration so short that price sensitivity to interest rate changes is negligible.

If a T-Bill yields 5% and a defense stock yields 2% with a 20% annual volatility, the stock must outperform its historical average by a massive margin just to justify the "stress-adjusted" return.

The "Dry Powder" Multiplier

For many investors, optionality means everything:

Total Return = Yield + The Value of Future Opportunity

If you are 100% positioned in "War Trades" and the conflict ends abruptly, your capital is locked in a drawdown exactly when the rest of the market (Tech, Consumer Discretionary) goes on a "Peace Rally" sale. By holding cash, you earn 5% to wait for the moment of maximum pessimism in the broader market. This allows one to buy the actual bottom of productive assets once the initial panic has liquidated everyone else.

Consider the two primary outcomes of a dragging conflict:

Scenario A (Stagflation): Supply chains break, and inflation stays "sticky." The Fed keeps rates higher for longer. Your T-Bills roll over into even higher yields, while the "War Stocks" struggle with rising input costs.

Scenario B (Deflationary Bust): The war triggers a global recession. Equities—including energy—crater as demand vanishes. Investors flee to the safety of government debt, pushing yields down and the value of your bonds up.

As such, short-term cash is the only asset that provides a "positive carry" (you get paid to hold it) while maintaining a 100% correlation to your own ability to change your mind.

Conclusion: The Peace of Mind Premium

The "War Trade" isn't about picking the right missile manufacturer; it’s about surviving the volatility long enough to buy the eventual recovery. If the conflict drags on, the winner won't be the investor who caught a 10% swing in Brent Crude, only to lose it in a 20% drawdown when the headlines changed.

The winner will be the investor who prioritized low-variance income and capital preservation.

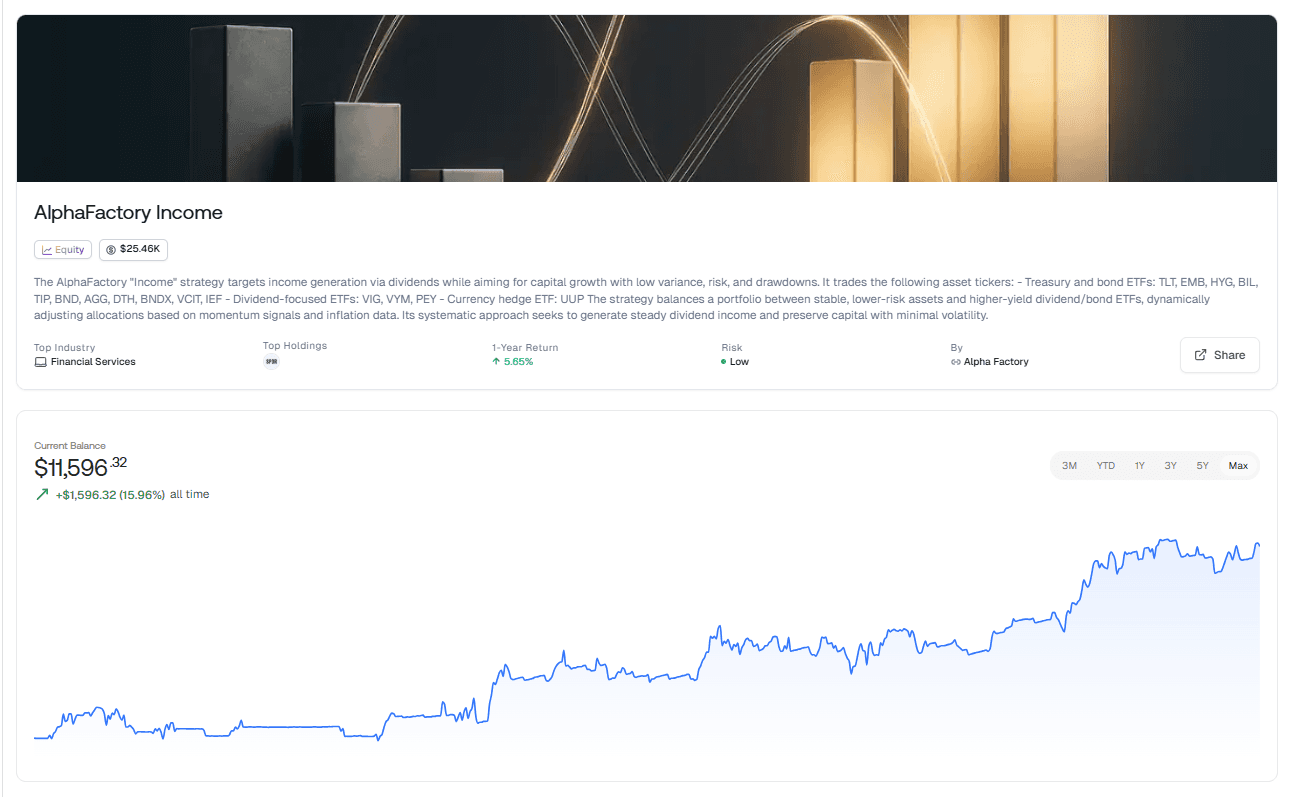

One of the best ways of achieving this is in Surmount’s AlphaFactory Income strategy.

By rotating through a curated universe of Treasury, Bond, and Dividend ETFs, you aren't just hiding—you are participating in a "Positive Carry" environment. This strategy effectively replaces the high-stress gamble of geopolitical speculation with a systematic, momentum-driven engine designed to thrive while others panic.

Why This Systematic Approach Wins Now:

Dynamic Defense: Using tickers like BIL and IEF allows you to capture that "Risk-Free" hurdle we discussed, while UUP (the Dollar Bull ETF) acts as a natural hedge against global instability.

Income Without the Beta: By focusing on VIG and VYM, you extract yield from high-quality companies that have the balance sheets to weather a macro storm, unlike speculative "war plays."

The Inflation Pivot: With TIP and BNDX in the mix, the strategy accounts for the "Stagflationary" risk of prolonged conflict, protecting your purchasing power in real-time.

Take Control of the Chaos

If you’re tired of checking the headlines every ten minutes to see if your portfolio is still intact, it’s time to move from speculation to systematics. Our upcoming Income & Growth Trading Class is built specifically for this macro environment. We teach you exactly how to navigate this basket of 15 elite tickers—TLT, VIG, UUP, and more—using momentum signals and inflation data to stay on the right side of the trade.

Stop betting on the war. Start profiting from the math.

NEVER MISS A THING!

Subscribe and get freshly baked articles. Join the community!

Join the newsletter to receive the latest updates in your inbox.

Related post

April 14, 2026

March 17, 2026