Why China's Robot Boom Could Already Be Outpacing Western Tech

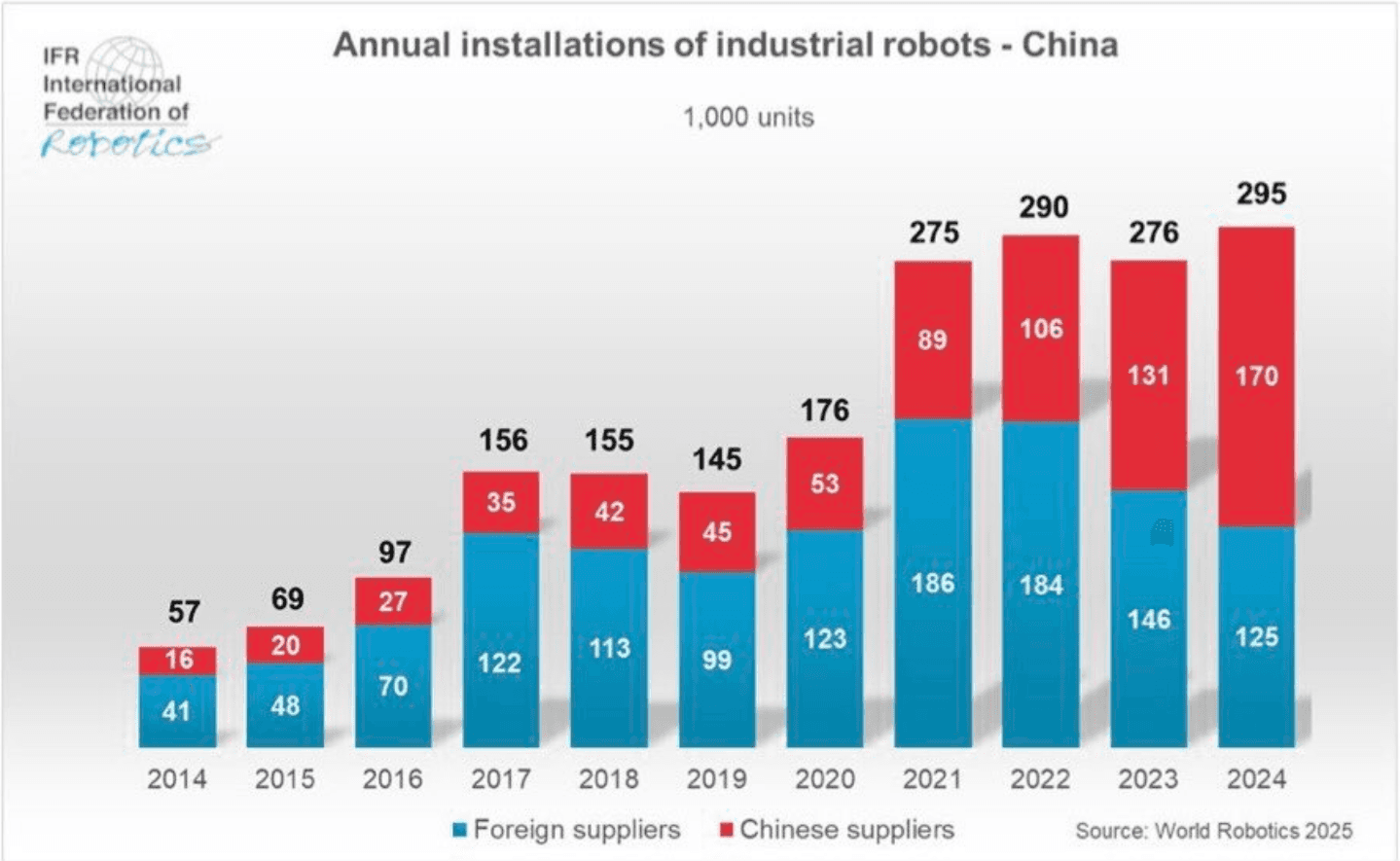

According to data published in the World Robotics 2025 report, China accounted for 54% of all new robot installations globally last year while the rest of the world is collectively lagging behind, unable to keep up with Beijing’s relentless automation mandate.

With over 295,000 units installed in 2024 alone—more than double the combined total of the United States, Japan, Germany, and South Korea—the sheer gap in progress highlights how the China robot boom is no longer a speculative threat for Western competitors, but a structural reality.

While Western big tech seems focused on perfecting "frontier AI" and singular, high-cost humanoid prototypes, China has already turned this technology into a high-speed commodity, and is widening the “robotic gap” across various critical fronts. This adds a mounting pressure to those already concerned about China’s advantageous AI positioning.

China Robot Density Takes The Lead

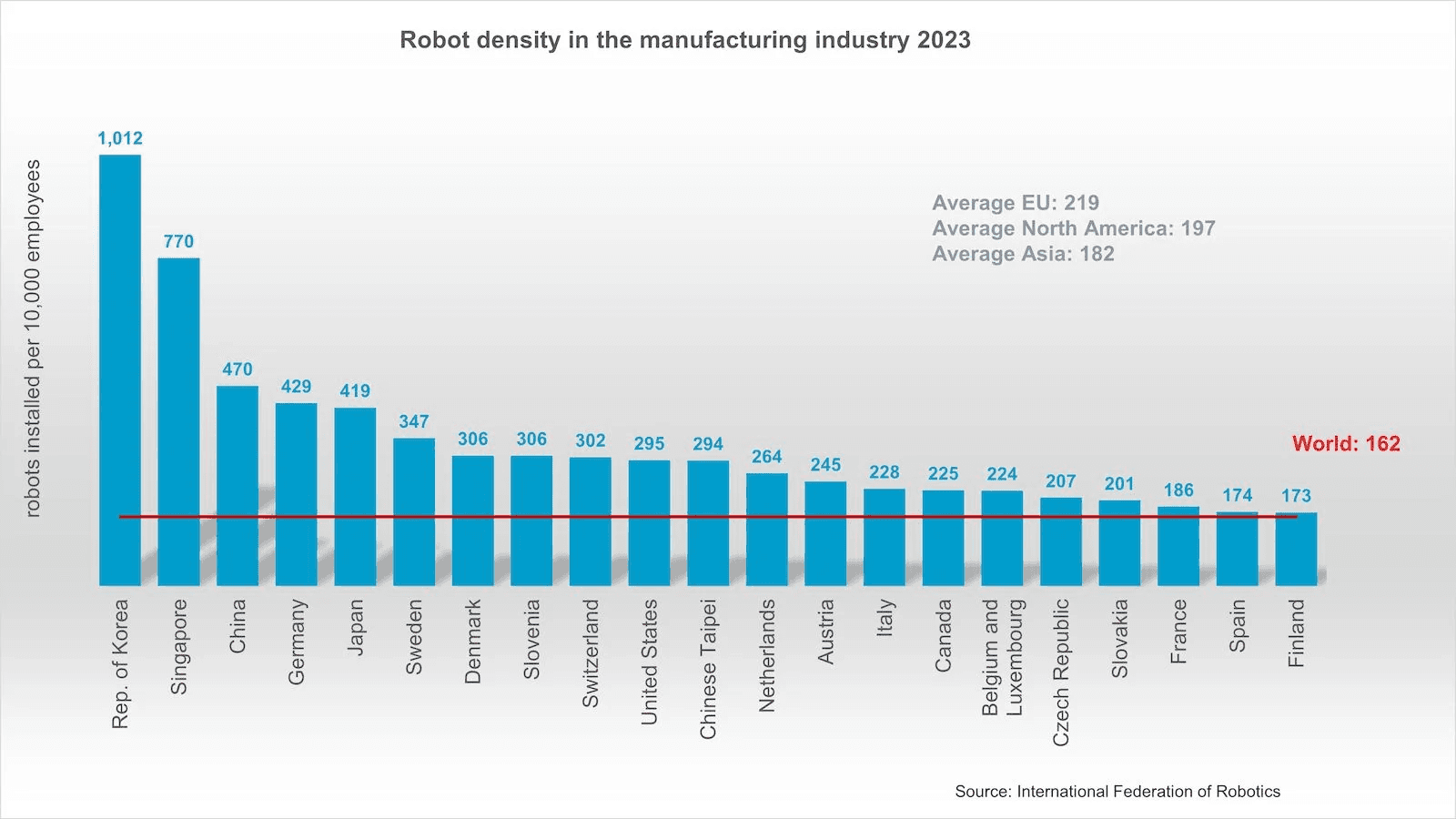

For several years, Germany, Japan and South Korea had a clear lead in robot density, which is the number of operational robots per 10,000 employees. However, the 2025 data confirms China undertaking an explosive leapfrogging maneuver, officially becoming a top contender in this space in just a decade.

Achieving one of the top spots in Robot density, despite a 1.4 billion population, is not an easy feat. While nations like South Korea or Singapore reached high density by automating small, specialized workforces, China’s robot boom has managed to move the needle for the largest labor pool on Earth.

The "Body" vs. The "Brain" Approach

One of the core reasons as to why there is such a stark divergence between China’s robot strides, and Western big tech progress on this front, is their fundamental philosophy of development.

The Western "Frontier" Model:

In the tech hubs of Silicon Valley and Boston, the primary goal has been to solve the "Brain" problem—creating a Generalized Artificial Intelligence that can navigate the infinite chaos of the real world.

This is plainly evident in the way Western leaders like Tesla, Figure AI, and 1X focus on high-fidelity, proprietary software stacks. They are essentially trying to build a "all-knowing" digital mind first, betting that once the brain is smart enough, the hardware will follow. That’s why there is so much emphasis on feeding massive quantities of video and text data into neural networks, hoping that "scaling laws" will eventually grant these machines the spatial reasoning needed to navigate a warehouse or a kitchen.

The Chinese "Commodity" Model:

In contrast, China’s strategy has been to prioritize the "Body", which entails mastering the hardware, the costs, and the physical deployment first. With this approach, Chinese robots are essentially becoming the "mobile phones" of the industrial world: standardized, high-volume, and incredibly cheap. As such, the country’s tech landscape is so easily able to commoditize hardware that what was once a specialized lab instrument is now a modular industrial tool. While the West waits for a "GPT-4 moment" for physical movement, China is flooding the zone with "Good Enough" robots that are learning on the job.

This "Body-First" philosophy creates a massive Data Flywheel that the West may struggle to replicate. By deploying hundreds of thousands of mid-tier robots today, Chinese firms are collecting billions of hours of real-world edge cases—the kind of messy, tactile data that cannot be perfectly simulated in a digital twin.

The Supply Chain "Super-Hub" Advantage to Chinese Robots

One highly overlooked advantage that fuels China’s robot lead isn't just the technology developed, but the ecosystem that births them. In cities like Shenzhen and Dongguan, the "Time-to-Prototype" is measured in days, not months. This is achievable because of some structural logistical strengths that define the Chinese robotics landscape:

Component Dominance:

China now produces the vast majority of the world’s harmonic drive reducers, sensors, and high-torque actuators—the "muscles" and "nerves" of any robot.

Vertical Integration:

Because the factories that build the parts are often in the same zip code as the labs that design the robots, the feedback loop is instantaneous.

The Cost Floor:

While a Western humanoid prototype might cost $150,000 to $250,000 to produce, Chinese competitors like Unitree and Agibot are already targeting the sub-$20,000 price point for mass-market hardware.

In the West, robotics is often treated as a software problem solved with hardware. In China, it is treated as a hardware problem accelerated by software.

A State-Backed Mandate

While Western robotics development is largely driven by venture capital and quarterly earnings, China’s boom is fueled by a centralized, multi-decade roadmap.

In early 2026, as the 15th Five-Year Plan (2026-2030) officially takes effect, Beijing has elevated robotics from a manufacturing tool to a "New Quality Productive Force"—a strategic category designed to redefine the nation’s economic DNA.

The 2027 Humanoid Deadline

The Ministry of Industry and Information Technology (MIIT) hasn't just set vague goals; it has mandated a "world-class humanoid industry system" be in place by 2027. This includes specific targets for mass-producing "brains" (AI control systems) and "limbs" (high-torque actuators) to ensure that 90% of the components in Chinese robots are locally sourced.

Solving the Demographic Paradox

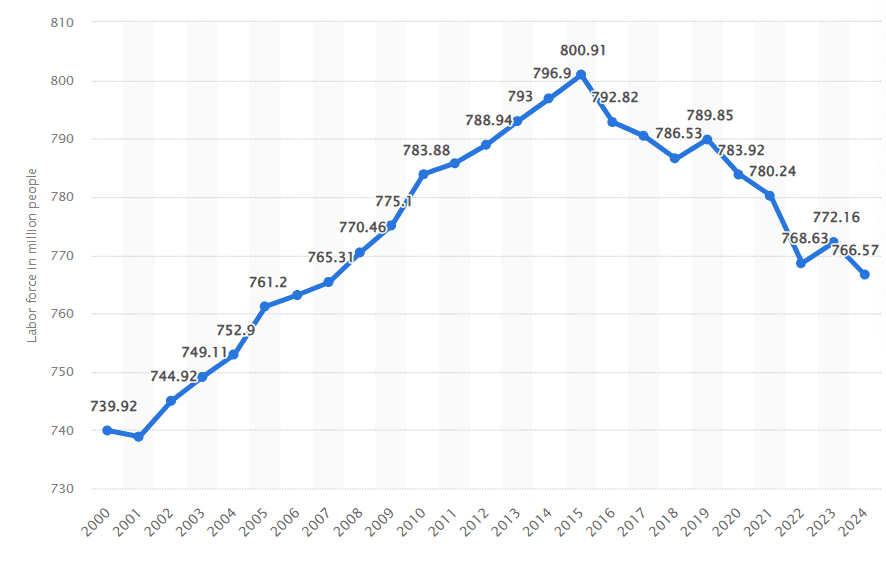

China is facing a shrinking working-age population faster than any nation in history. According to data from Statista, after peaking in 2015, the country’s labor market size is now down to 2007 levels, in a trend that is unlikely to slow down in the near-term.

As such, the state-backed mandate isn't a "race against the West" as much as it is a race against time. By integrating "AI+ Manufacturing," the government is attempting to "get rich even as the country gets old," replacing lost human labor with an automated workforce that operates 24/7.

The Geopolitical Shift

By treating robots as essential infrastructure—similar to 5G or high-speed rail—China is essentially "hardcoding" its lead into the global supply chain. In 2026, for the first time, Chinese manufacturers are selling more robots domestically than foreign competitors (57% market share), signaling that the West has lost its last foothold in the world's largest automation market.

Capturing China’s Robot Revolution

China is doing more than just building robots. It’s redefining the way industries operate. While Western tech focuses on frontier AI and high-cost prototypes, China has made robotics a mass-market, high-speed, commodity reality, deploying hundreds of thousands of robots across factories, warehouses, and logistics networks.

This “Body-First” approach is already generating measurable efficiency gains, collecting real-world operational data, and creating a competitive moat that will influence the productivity and profitability of Chinese businesses for years to come.

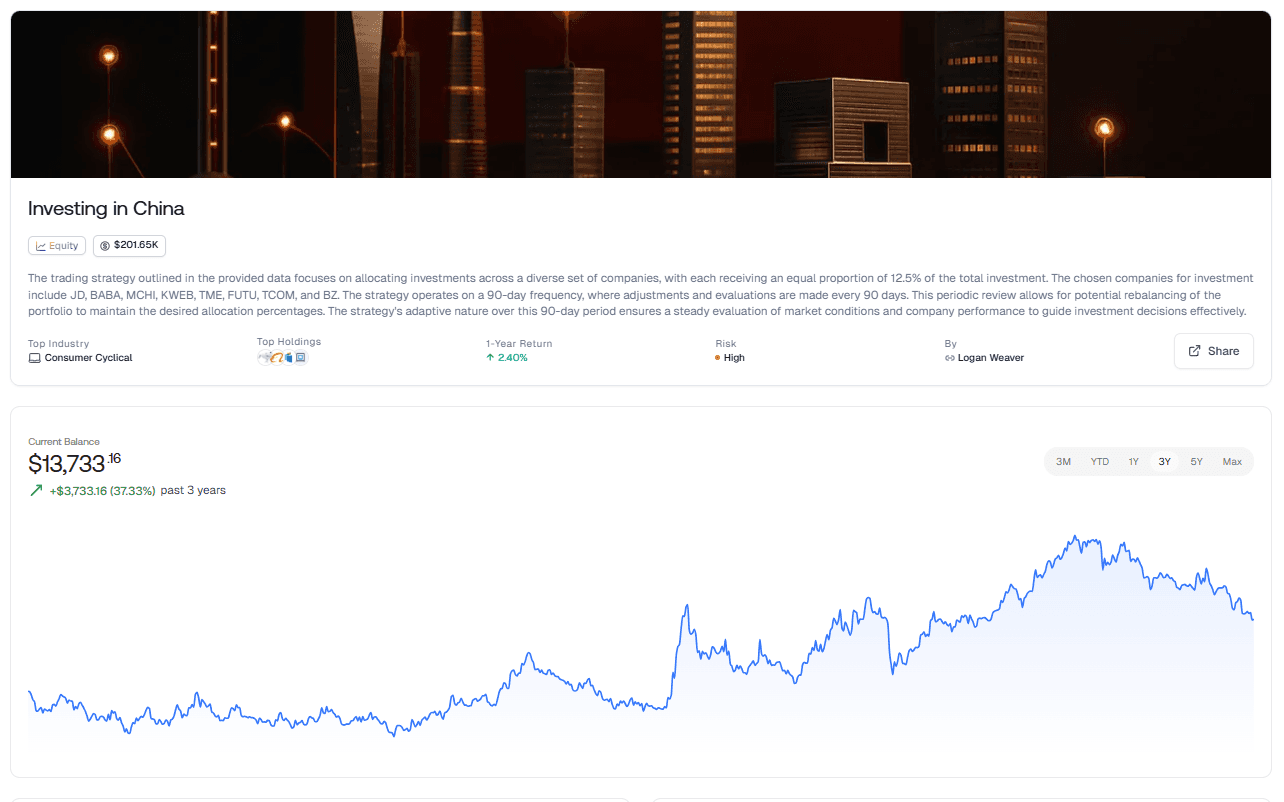

One indirect way investors can tap into this robotic boom is through the “Investing in China” strategy on Surmount:

This strategy equally allocates across eight leading Chinese stocks and ETFs, including JD.com, Alibaba, and KWEB, and is naturally positioned to capture the ripple effects of this structural shift.

These companies are not passive players—they are actively integrating robotics and automation into their operations, driving cost efficiencies, faster fulfillment, and improved margins. Broad exposure through ETFs adds another layer, tapping into the wider industrial ecosystem powering China’s robotic expansion.

Rebalancing every 90 days allows the portfolio to stay aligned with the companies that are leading the deployment of robotic infrastructure, while diversification reduces single-stock risk.

Essentially, this approach turns the structural transformation of China’s economy into an actionable investment framework: rather than betting on a single technology or company, it benefits from the cumulative gains flowing across the nation’s market leaders as the robot boom reshapes productivity and competitive positioning.

NEVER MISS A THING!

Subscribe and get freshly baked articles. Join the community!

Join the newsletter to receive the latest updates in your inbox.