Why the "SaaSpocalypse" Might Be the Most Crowded Mistake of 2026

Throughout February 2026, the "SaaSpocalypse" had become the buzzword in the market, referring to the massive market correction where over $1 trillion in value was wiped from software stocks in just a few weeks.

In particular, the S&P North American software index had undergone its most vicious fall since the 2008 financial crisis, while stalwarts like Microsoft saw a sharp plunge from its $481 highs at the end of January, to its current price of $398.

This violent repricing is increasingly being seen as a philosophical rejection of the subscription economy. Driven by the fear that autonomous AI agents have rendered human "seats" obsolete, investors fled the sector in a herd.

However, given the sheer unanimity of the panic, this crash is rapidly shaping up to be the most "crowded mistake" of 2026. While the sell-off feels like a final judgment, it is rooted in a fundamental misunderstanding of how enterprise value is actually created.

This does not seem like the extinction of software at all. In fact, this may be a clear case of a narrative overshoot.

The Market Is Pricing Substitution. The Data Suggests Augmentation

The primary engine driving the SaaSpocalypse panic is a simple, seductive piece of "efficiency math." Investors looked at new AI agents and calculated a lethal formula: If one AI agent can do the work of ten humans, then enterprise customers will fire nine people, cancel 90% of their software licenses (seats), and the SaaS vendor’s revenue will collapse.

This calculation assumes AI to be a "drop-in" replacement that deletes the need for software. However, early 2026 data reveals a far more complex reality: Augmentation.

According to recent Gartner forecasts for 2026, worldwide software spending is actually accelerating, projected to grow by 14.7% to reach $1.4 trillion.

This data is quite telling because according to these projections, software spending isn’t simply rising, but is in fact accelerating.

If AI were purely substitutive, we would see these budgets shrinking. Instead, we are seeing a massive "flush" of capital into the sector as enterprises realize that AI doesn't work in a vacuum; it requires a robust software substrate to operate.

To distinguish between the hype and the reality, we can apply the Augmentation Test. If AI is strengthening incumbents, we should see three specific signals:

AI Attach Rates & Pricing: Far from becoming "free," AI capabilities are driving higher Average Revenue Per User (ARPU). In 2025, 68% of vendors restricted AI to premium tiers. By early 2026, AI "add-ons" are commanding premiums of 30% to 110% over base costs.

Spending Intensity: Data from Zylo shows that for "AI-native" applications, enterprise spend surged by nearly 400% in a single year. Organizations are not buying fewer tools; they are spending more on the intelligence inside the tools they already have.

Net Revenue Retention (NRR): While seat counts are under pressure in some departments, the median B2B SaaS NRR remains stable at around 102%. This suggests that even if a company reduces human headcount, they are expanding their "wallet share" with the vendor to pay for the "digital workers" (AI agents) that replace them.

Given the data, therefore, the "crowded mistake" lies in the belief that an AI agent is a replacement for a SaaS seat. In reality, GenAI is becoming the most expensive "invisible worker" in the enterprise.

When an AI agent performs the work of five traditional employees, the business doesn't stop using the CRM; it increases its usage of the CRM's API, data storage, and processing power. This is why 61% of SaaS companies have already pivoted toward hybrid or usage-based pricing models, up from 49% in 2024. The revenue isn't disappearing—it's just changing shape, moving from "counting heads" to "counting outcomes."

Software’s Real Moat Isn’t Code. It’s Institutional Architecture

Another implicit view underpinning the SaaSpocalypse is this idea that AI can now somehow generate a functional CRM or ERP system in a weekend, which logically renders the billion-dollar incumbents as obsolete.

This explains Salesforce’s hard plummet last month, causing it to shed about one third of its market value:

This idea, however, doesn’t hold up very well, because the true moat of enterprise software isn't the code—it’s the Institutional Architecture it houses.

The "System of Record" vs. The "System of Intelligence"

An AI agent is a system of intelligence; it is fast, clever, and adaptable. But an enterprise needs a System of Record: a rigid, unmoving source of truth that governed by strict rules.

Compliance Frameworks: A global bank doesn’t use a SaaS platform just to store data; they use it because that platform has spent a decade earning SOC2, HIPAA, and GDPR certifications.

Workflow Logic: Large organizations have millions of "if/then" statements baked into their software—rules about who can approve a $5M spend or how a tax domicile is calculated.

Data Models: These aren't just lists; they are complex hierarchies built over years. Moving that data isn't a "copy-paste" job; it’s a structural re-engineering project.

The Great Sorting: Horizontal vs. Vertical

The SaaSpocalypse isn't an extinction event; it’s a Sorting Event. We are seeing a violent decoupling of software value based on "domain density."

Horizontal Point Solutions (High Pressure): Simple tools for note-taking, basic scheduling, or generic "wrappers" around databases are indeed being vaporized. If your software's value is just "making a task easier," an AI agent will likely eat your lunch.

Vertical, Domain-Dense Platforms (Low Pressure): Platforms that manage clinical trial data, construction blueprints, or complex supply chains are not being displaced. Their value is the specialized, rigid architecture that AI agents actually need to plug into to be useful.

The deeper the workflow embedding, the harder the displacement. You can replace a hammer (a tool) with a robot, but you cannot easily replace the foundation of the house (the architecture).

The SaaSpocalypse Opportunity For Investors

In 2026, the "Rip and Replace" idea remains the most expensive phrase in the corporate dictionary. Most CIOs aren't looking to burn down their existing infrastructure; they are looking to supercharge it. They want an AI agent that lives inside their trusted Salesforce or Workday environment, not a standalone AI that requires them to migrate twenty years of institutional memory into a "black box."

If the SaaSpocalypse has taught us anything, it’s that broad-market fear creates a unique opening for those who understand the underlying plumbing of the digital age. The "crowded mistake" of 2026 is treating all tech as a monolith. To capitalize on the recovery, investors need a framework that separates the "lazy middle" from the foundational titans.

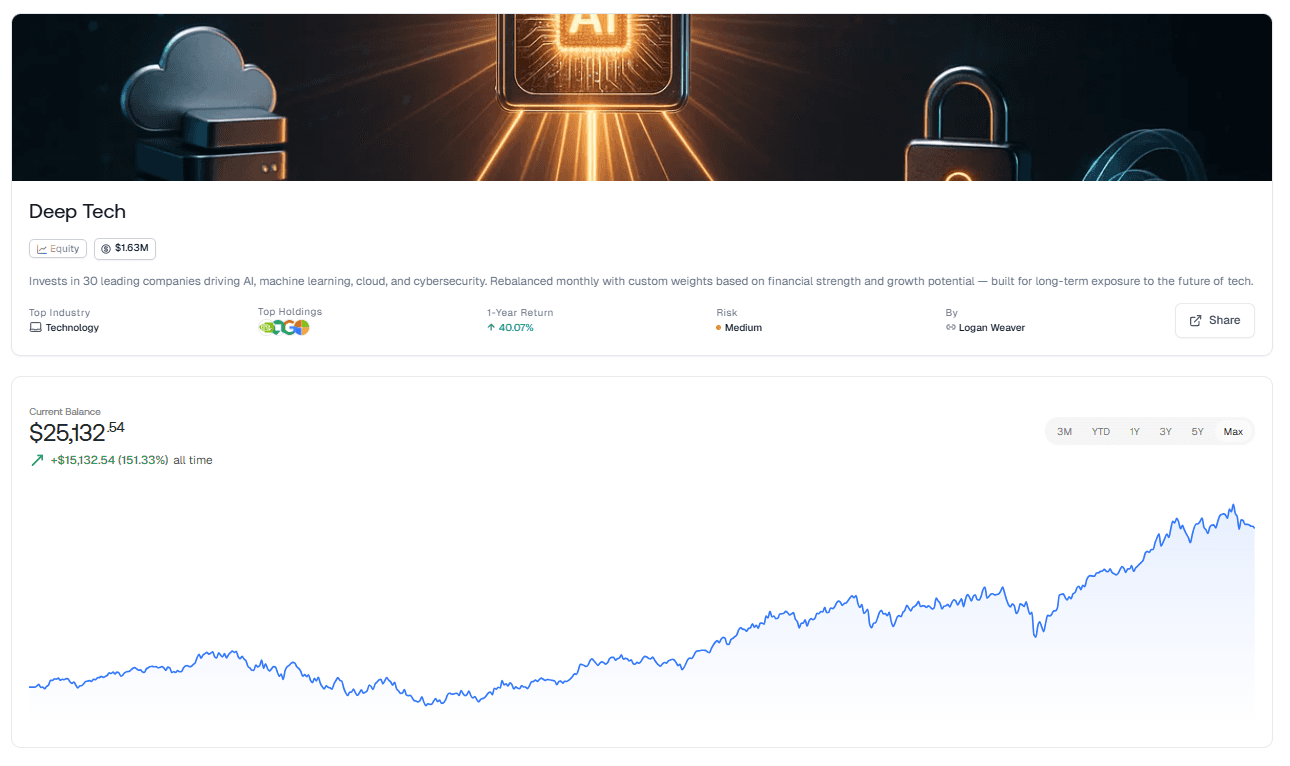

This is precisely why we recommend integrating the Deep Tech Innovators Thematic Investing Strategy into your portfolio.

While the retail market reacts to headlines, this strategy is designed to leverage the structural shift toward deep technology, the very infrastructure that makes the "AI Augmentation" possible.

Why Deep Tech Innovators?

This is a long-term, systematic approach built to navigate the volatility of the AI era. It doesn't just bet on "software"; it bets on the entire Deep Tech Stack:

Diversified Exposure: From the semiconductors powering the models to the cybersecurity protecting them and the cloud computing environments where they live.

Precision Weighting: The strategy identifies 30 public companies with established track records, using a customizable weighting system. Allocations are derived from each company’s financial strength and potential upside relative to their peers.

Agile Rebalancing: In a year as fast-moving as 2026, "set it and forget it" is a risk. This strategy runs on a daily interval and rebalances every 30 days to ensure your capital is always aligned with the strongest performers in the sector.

Secure Your Position in the Refactoring

The market is currently discounting extinction while the world’s largest enterprises are increasing their deep tech budgets. History shows that the greatest returns are found by investing in the "infrastructure of the future" while the rest of the world is still debating the past.

By focusing on companies well-positioned to benefit from the emerging potential of deep tech innovations, this strategy aims to deliver long-term capital appreciation and diversified growth across the most transformative areas of modern technology.

NEVER MISS A THING!

Subscribe and get freshly baked articles. Join the community!

Join the newsletter to receive the latest updates in your inbox.