How to Invest During an Oil Price Shock Before It's Late

For the better part of two decades, cheap energy didn't make you a great investor. It just made the environment forgiving. Oil at $50–60 a barrel was the performance-enhancing drug nobody questioned, because everybody was on it.

Portfolios were fat with consumer discretionary names, logistics plays, and capital-intensive manufacturers — all built on an implicit assumption that energy would stay cheap forever. That assumption is now broken.

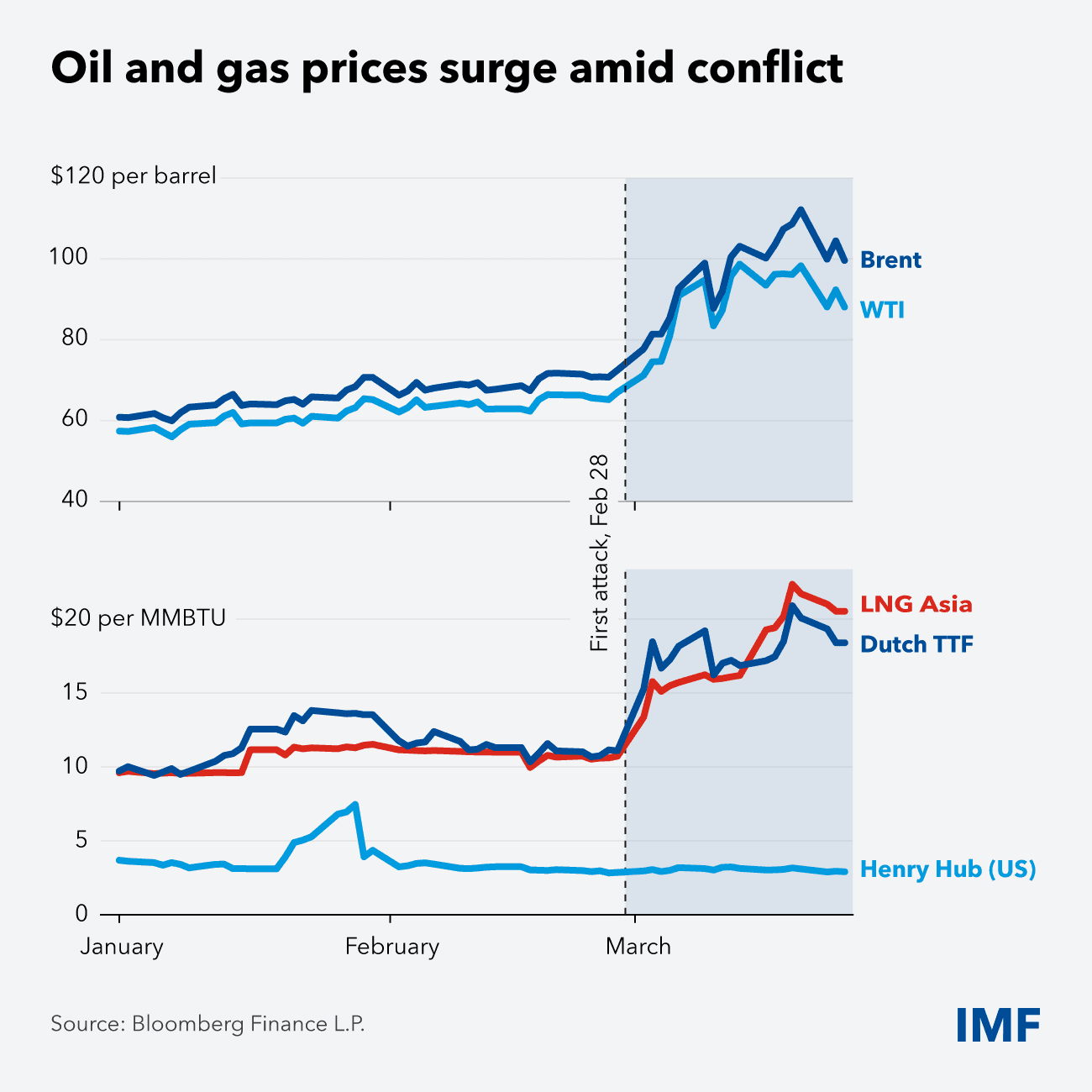

The closure of the Strait of Hormuz hasn't just disrupted oil supply. It has exposed the structural fragility that cheap energy was quietly hiding.

Why Your Portfolio Was Calibrated for a World That No Longer Exists

Think about what a decade of cheap energy actually did to capital allocation. Consumers loaded up on SUVs and energy-intensive goods. Companies optimised for labor efficiency over energy efficiency. Equity valuations in consumer cyclicals, industrials, and logistics were priced for a world where energy was essentially a rounding error on the income statement.

Your portfolio, statistically speaking, was built for that world. The question isn't whether this shock matters — it's whether you've already adjusted, or whether you're still positioned for yesterday's regime.

The Hidden Cost of Energy Dependency Nobody Talked About

Here's what the bulls on consumer stocks never modelled: when energy prices spike sharply, consumers don't just cut fuel spending. They cut everything discretionary to balance the budget. The energy shock becomes a spending shock, which becomes an earnings shock across sectors that had nothing to do with oil. That transmission mechanism is already in motion. The investors who understand it early are the ones who reposition before the earnings revisions hit.

Energy Price Shock Sector Rotation 2026

This is not 1973. The U.S. runs a net petroleum trade surplus, which partially insulates domestic energy producers from the demand-side pain hitting consumers. That asymmetry is the key to understanding where capital is flowing — and why Energy, Industrials, and Materials have dramatically outperformed since the start of 2026 while consumer cyclicals and technology have struggled.

The old playbook of buying the dip in growth stocks during macro uncertainty isn't working, because this isn't a demand-driven slowdown. And as we've previously argued, a significant portion of today's commodity price spike is geopolitical premium that markets are still struggling to price accurately. This means that the repricing isn't over.

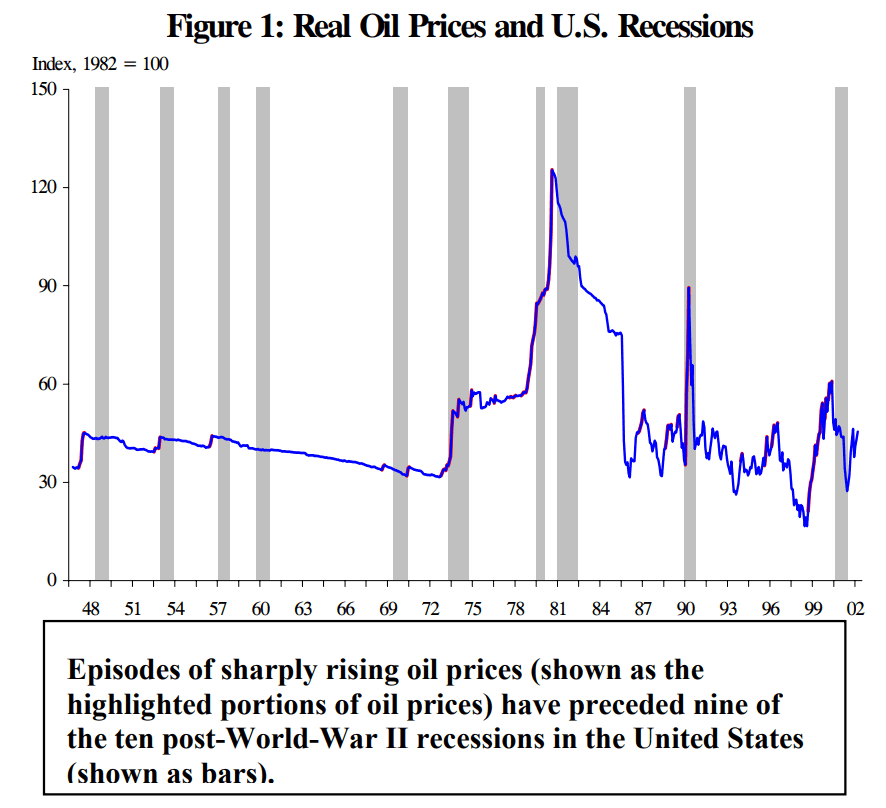

We are dealing with a supply shock, and supply shocks reprice economies structurally, not cyclically.

How to Reposition Your Portfolio After an Oil Supply Disruption

The sectors that get hurt first in a supply shock are those with the thinnest energy cost buffers and the most discretionary revenue streams. Airlines, road freight, fast fashion, and big-box retail all face simultaneous margin compression and demand softness. The sectors that benefit — domestic energy producers, efficiency infrastructure, and anything that monetises the transition away from oil dependency — are where smart money has already begun rotating.

Repositioning isn't about panic-selling. It's about recognising that the adjustment cycle is just beginning, and that the market is still in the early innings of repricing the full chain of second-order effects.

Energy Transition Investing: The Sectors That Win and Lose From Here

Persistent high energy prices do something powerful that decades of climate policy couldn't quite achieve: they make alternatives economically obvious. Before rotating aggressively into energy winners though, it's worth checking whether the commodity enthusiasm itself is nearing a cyclical peak. (Here are five red flags worth watching).

Renewables, EVs, energy storage, and grid infrastructure don't need a subsidy argument when oil is at $100-plus. They need a spreadsheet. And right now, the spreadsheet is increasingly making the case for them on its own.

The sectors positioned to compound through this disruption are those that either produce energy domestically, reduce energy dependency structurally, or enable the infrastructure of a lower-consumption economy. This isn't a values trade. It's a price signal trade — the oldest and most reliable kind.

Why an Algorithmic Investing Strategy Beats Discretion During Oil Price Volatility

Here's the uncomfortable truth: your investing instincts were trained in the cheap energy era. Every heuristic you developed, every sector bias you carry, every valuation shortcut you rely on was calibrated when $60 oil was the baseline. That's not an insult — it's just how pattern recognition works. The problem is that your patterns are now running on stale data.

This is precisely where rules-based, algorithmic strategies have a structural advantage. They don't carry the anchoring bias of the old regime. They respond to current price signals, not to what price signals used to mean. During periods of genuine regime change — and this is one — removing human discretion from the execution layer isn't a limitation. It's the edge.

The Geopolitical Risk Premium Is Still Being Mispriced — Here's the Contrarian Opportunity

Consensus is still treating the Hormuz closure as a temporary disruption.

History suggests that's optimistic, and markets that price geopolitical shocks as transient tend to reprice sharply when the timeline extends. The contrarian position is not just that energy stays elevated — it's that the structural acceleration of the clean energy transition just got a decade of tailwind compressed into two or three years.

That compression is where the asymmetric opportunity lives. The investors who move before the consensus updates their models are the ones who capture it fully.

How to Position for It

If the analysis above is right — that persistent high energy prices are the single most powerful structural accelerator of clean energy adoption — then the most forward-looking portfolio move right now isn't just defensive rotation. It's offensive positioning into the transition itself.

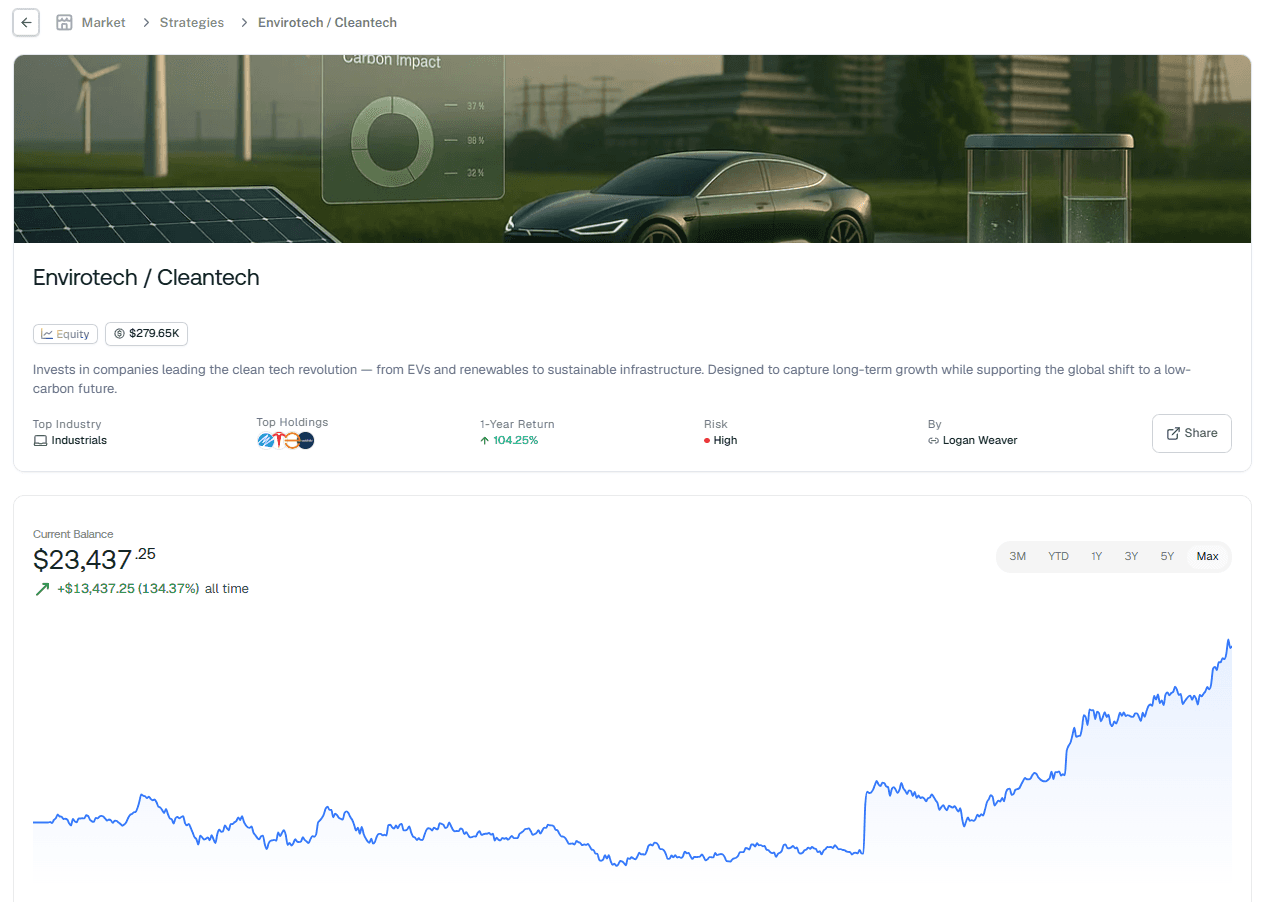

The Envirotech / Cleantech strategy on Surmount AI was built for exactly this moment.

This isn't a feel-good ESG play. This is a hard-nosed contrarian thesis: when oil becomes structurally expensive, renewables, EVs, energy storage, water management, and sustainable infrastructure don't just become morally preferable — they become economically inevitable. The Hormuz closure didn't change the destination. It just dramatically shortened the timeline.

The Envirotech / Cleantech strategy invests in the companies leading this transformation — the ones building the infrastructure that a high-energy-cost world is now urgently demanding. It's automated, rules-based, and designed to capture long-term structural growth without the behavioural drag of discretionary decision-making in a volatile environment.

This is the trade that the cheap-energy era made easy to ignore. That excuse is gone.

Deploy the Envirotech / Cleantech strategy to your portfolio on Surmount AI — before the window the consensus hasn't priced yet closes.

Frequently Asked Questions

How do you invest during an oil price shock without panic-selling?

The key is repositioning systematically rather than reactively — rotating toward energy producers, efficiency infrastructure, and clean tech before consensus catches up. Rules-based strategies remove the emotional bias that causes most investors to move too late.

Why does an oil price shock cause a recession even in sectors unrelated to energy?

Because consumers cut discretionary spending across the board to absorb higher fuel costs, transmitting the shock into retail, logistics, and manufacturing earnings. The energy hit becomes a spending hit — and most portfolios aren't positioned for that second wave.

What does energy price shock sector rotation look like in 2026?

Capital is visibly rotating out of consumer cyclicals and technology into energy, industrials, and materials — sectors that either produce energy or structurally benefit from higher input costs. The rotation is still early, meaning the repricing opportunity hasn't fully closed yet.

How does investing in energy transition companies help during an oil supply disruption?

Persistent high oil prices make renewables, EVs, and energy storage economically compelling without needing a policy argument — the spreadsheet makes the case on its own. Energy transition investing effectively turns a supply shock into a structural long-term tailwind.

Why is an algorithmic investing strategy better than discretionary trading during oil price volatility?

Human instincts were calibrated during a decade of cheap energy, making them unreliable guides during a genuine regime change. Algorithmic strategies respond to current price signals without the anchoring bias of the old energy paradigm — that's a measurable edge in volatile conditions.

NEVER MISS A THING!

Subscribe and get freshly baked articles. Join the community!

Join the newsletter to receive the latest updates in your inbox.