The AI Data Center Energy Crisis Nobody Is Pricing Into Markets

The artificial intelligence boom has captivated markets, minted billionaires, and rewritten valuations across the technology sector. But while investors obsessively track GPU shipments, hyperscaler earnings calls, and the latest large language model benchmarks, a far more prosaic constraint is quietly tightening around the entire AI investment thesis.

Electricity.

Not algorithms. Not regulation. Not even competition. The mundane, unglamorous reality of how much power it takes to run the AI revolution — and how badly the grid is struggling to provide it — may ultimately determine which companies survive the buildout, which investors profit, and whether current valuations have any basis in reality at all.

1. The Grid Is Already Breaking Under AI's Weight

The scale of the AI infrastructure buildout is genuinely unprecedented. The five largest AI hyperscalers are projected to spend a combined $750 billion on capital expenditures in 2026 alone — an increase of over 80% versus 2025. Every dollar of that spending assumes one thing: that the power will be there when the data centers come online.

Increasingly, it won't be. Roughly half of all planned AI data centers are currently being delayed or suspended — not because of financing problems or permitting bureaucracy, but simply because the electrical generation capacity does not exist to support them. These are not marginal projects on the fringes of the buildout. These are core infrastructure investments being stalled by a grid that was never designed for gigawatt-scale demand arriving this suddenly.

For investors pricing in a seamless, uninterrupted AI infrastructure ramp, this is a material risk that is almost entirely absent from the consensus narrative.

Regional Electricity Costs Are Surging

The demand shock is already showing up in electricity prices. Regional electricity costs are rising sharply across key data center markets in the United States. This has a compounding effect on the economics of the buildout — higher operating costs reduce the return on the enormous capital being deployed, pressuring the already deteriorating free cash flow picture at the major hyperscalers.

This is not a temporary supply-demand imbalance that normalises in a quarter or two. Grid modernisation investment operates on decade-long timelines. The demand is arriving now.

Local Opposition Is Becoming a Real Barrier

There is a third dimension to this constraint that receives almost no coverage in mainstream financial media. Local and regional opposition to new data center construction is growing materially. Communities are pushing back against the noise, the water consumption, the visual impact, and most pointedly, the electricity costs that large-scale data center development pushes onto residential and commercial ratepayers.

This opposition translates directly into permitting delays, legal challenges, and in some cases outright rejection of proposed developments. For a buildout operating on the assumption of frictionless execution, this represents a source of real-world friction that financial models are not capturing.

2. The Hidden Ceiling on Hyperscaler Capex

The fundamental problem is a timing mismatch of historic proportions. AI-driven power demand is scaling exponentially. Grid modernisation — new transmission lines, upgraded substations, expanded generation capacity — scales on bureaucratic, regulatory, and engineering timelines measured in years, sometimes decades.

Utilities are not slow because they are incompetent. They are slow because building energy infrastructure in a regulated environment, across multiple jurisdictions, with environmental review requirements, is genuinely complex. That complexity does not compress to match the ambitions of Silicon Valley's capital allocation cycles.

Load growth forecasts that utilities published as recently as 2022 have already been rendered obsolete by AI power consumption projections. The grid is being asked to absorb a demand shock it had no meaningful time to prepare for.

Baseload Power Constraints Nobody Is Talking About

AI data centers require something particularly demanding from an energy grid perspective: consistent, uninterruptible baseload power. Unlike residential or commercial demand, which is variable and somewhat predictable, large-scale AI inference and training workloads require stable power delivery around the clock.

This places unusual pressure on baseload generation sources — primarily natural gas, nuclear, and coal — at precisely the moment the energy transition is shifting investment toward intermittent renewable sources. Wind and solar, whatever their long-term merits, cannot serve as the primary power source for a data center running continuous AI workloads. This tension between the energy transition agenda and the raw power requirements of the AI buildout is a contradiction that markets have not begun to seriously price.

Gigawatt-Scale Demand Meets Nineteenth-Century Infrastructure

Much of the transmission infrastructure underpinning the American grid dates, in its basic architecture, to the mid-twentieth century or earlier. It was not built to move power at the scale, speed, or directional flexibility that a geographically concentrated cluster of hyperscale data centers demands. Behind-the-meter power solutions and on-site generation are emerging as partial workarounds, but they introduce their own costs and complexities — costs that flow directly back into the capex and operating expense lines that are already under severe pressure.

3. What This Means for the AI Investment Thesis

Markets are currently pricing AI stocks as though the buildout will proceed on schedule, at projected cost, with power available on demand. The Shiller PE and the Buffett Indicator are both signalling valuation extremes comparable to — and in some measures exceeding — the peak of the Internet Boom in 1999. That boom also had a genuinely transformative technology at its core. It also ended with the NASDAQ surrendering over 80% of its value peak to trough.

The AI data center energy crisis is not a theoretical future risk. The delays are happening now. The cost overruns are happening now. The free cash flow deterioration at the hyperscalers is happening now. The market is simply choosing not to look.

Utility Stocks and Nuclear Energy Are the Contrarian Play

If the AI boom is real but constrained by energy, the logical contrarian allocation shifts away from the priced-to-perfection hyperscalers and toward the infrastructure required to actually power them. Utility stocks levered to load growth and nuclear energy assets — particularly those positioned to provide reliable baseload power to data center campuses — represent the unglamorous, under-owned, under-discussed side of this trade.

The Bottleneck That Could Pop the AI Bubble

Every great technology boom has eventually met a physical constraint that the financial narrative chose to ignore until it could not. For the railroad era it was overcapacity. For the Internet Boom it was the absence of viable business models behind the infrastructure spend. For the AI boom, the constraint may well be something as simple, as boring, and as immovable as the capacity of the electrical grid.

The market is betting on the algorithm. The contrarian bet is on the kilowatt.

Get Positioned for What Comes Next

The thesis in this piece is straightforward: AI infrastructure is running into a physical ceiling, valuations are stretched to historic extremes, and the consensus is not pricing any of it in. Knowing that is useful. Having a mechanism to act on it — automatically, systematically, without emotion — is where analysis becomes returns.

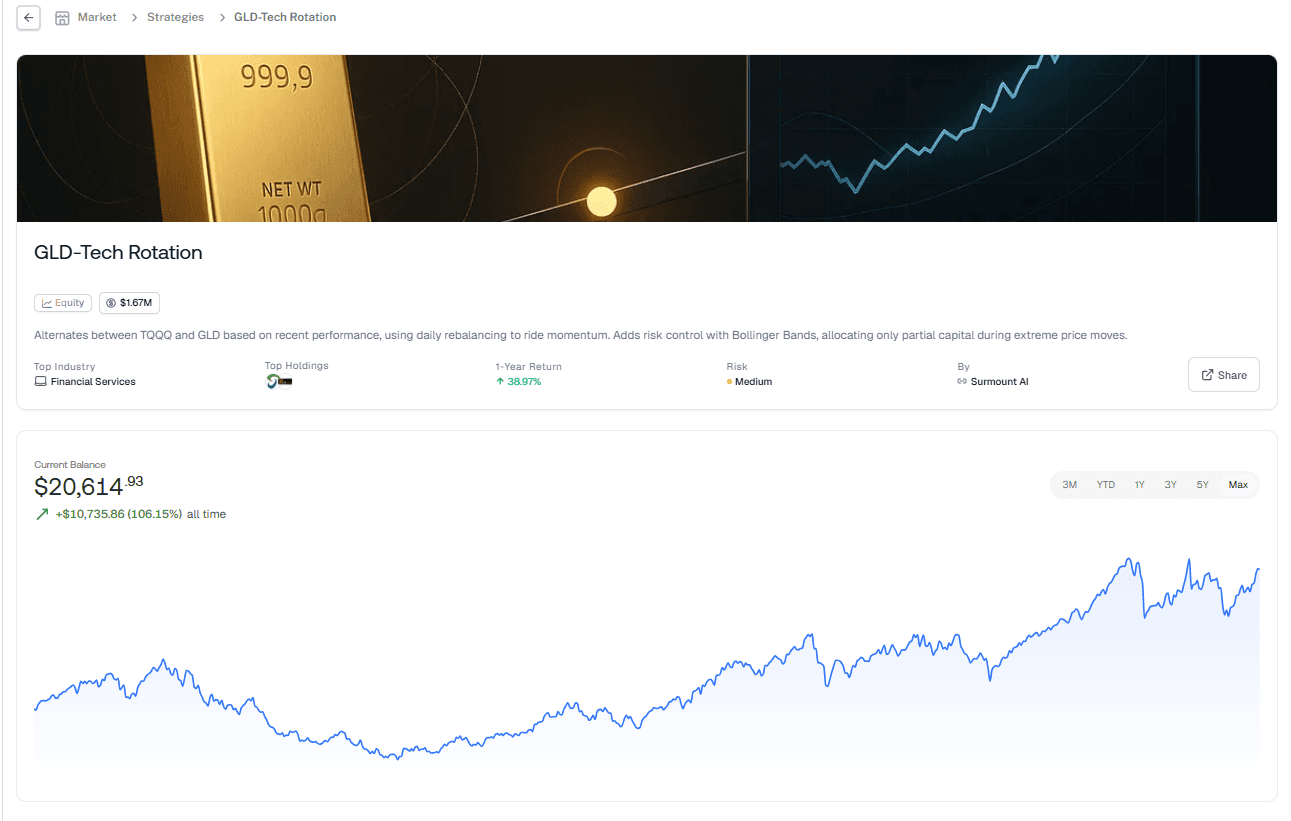

That is precisely what the GLD-Tech Rotation strategy on Surmount is built for.

The Strategy That Rotates So You Don't Have To

The GLD-Tech Rotation strategy is an algorithmic approach that alternates capital between two positions: TQQQ (ProShares UltraPro QQQ — 3x leveraged tech exposure) and GLD (SPDR Gold Trust — the canonical safe haven asset). The logic is elegant in its simplicity. Every day, the strategy increases its position in whichever asset is outperforming the other on a recent historical basis, systematically riding momentum and rotating away from weakness.

In practical terms, this means that when tech is running — as it has been through the AI boom — the strategy is long tech. When tech momentum deteriorates and gold begins to assert itself — as it does in precisely the kind of risk-off, overvaluation-correction environment this blog has been describing — the strategy rotates into gold. Automatically. Without hesitation. Without the paralysis that hits most investors when the narrative they have believed in for three years starts to crack.

This is not a passive bet against tech. It is a dynamic, momentum-driven system that profits on both sides of the rotation.

Built-In Protection for Extreme Markets

Here is where the strategy earns its keep for the contrarian investor specifically.

When recent prices move more than 1.5 standard deviations away from the 20-day moving average — the kind of parabolic, Bollinger Band-breaching moves we have seen repeatedly across AI-related equities — the strategy automatically reduces its capital deployment to 50%. It does not try to call the top. It does not panic. It simply reduces exposure when markets enter the statistically extreme territory that historically precedes sharp reversals.

For an audience that has just read about Shiller PE ratios at 1999 extremes, semiconductor indices going parabolic, and valuations discounting earnings years into the future — this is not an abstract risk control feature. It is a mechanism designed for exactly the market environment we are describing right now.

The Contrarian Edge, Systematised

Most investors intellectually understand the rotation trade. They know gold outperforms in risk-off environments. They know overleveraged tech is vulnerable when sentiment shifts. They know they should reduce exposure when valuations are stretched. But knowing and doing are separated by the most expensive gap in investing: human emotion.

The GLD-Tech Rotation strategy closes that gap. It executes the thesis this blog is making — systematically, daily, without ego — and it does so with built-in tail risk management for the extreme price environments that define the late stages of every bubble.

If the contrarian case laid out above proves correct, this strategy is structurally positioned to capture the rotation. If tech continues to defy gravity for another leg higher, the strategy captures that too.

That is the definition of an asymmetric setup.

Explore the GLD-Tech Rotation strategy on Surmount and automate the trade the market is not yet making.

NEVER MISS A THING!

Subscribe and get freshly baked articles. Join the community!

Join the newsletter to receive the latest updates in your inbox.