The Great "Existing Home" Liquidation to Watch

A March 2025 survey from Clever Real Estate found that 70% of Americans fear an impending housing market crash, driven by concerns that new trade policies and tariffs could hinder inventory. The study further indicates that 95% of respondents are worried about general price increases.

More recently, the wider market seems particularly fixated on the potential inflation impacts that may materialize from the effectively closed Strait of Hormuz and the resulting spike in diesel and fertilizer costs. While the "higher-for-longer" interest rate narrative is back in vogue, investors seem to be treating the housing market as a monolith of "permanent scarcity."

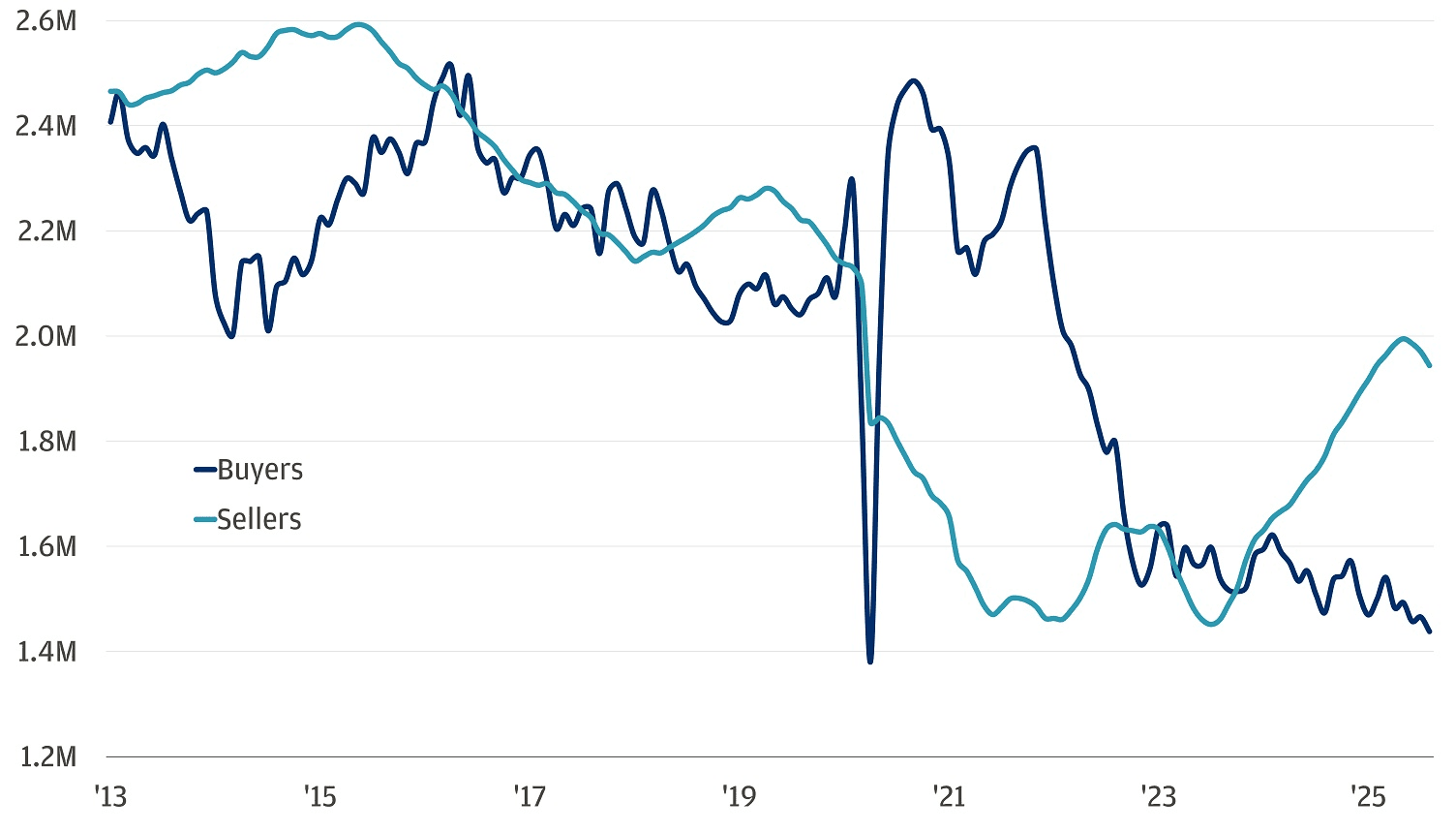

The consensus view is that a "lock-in" effect—where homeowners refuse to sell and abandon their 3% mortgages—has created a floor under prices. But look closer at the fissures appearing in early 2026. The "housing shortage" seems to resemble a psychological standoff that is currently being lost by the builders. This seems to be evident in the degree to which home-sellers noticeably outweigh home-buyers:

Take Lennar Corporation (LEN) as the canary in the coal mine. While existing homeowners cling to 2021 valuations, the nation's largest builder has already surrendered. Lennar is now spending a staggering 14% of home sales revenue on incentives—mortgage buy-downs, free upgrades, and closing costs—just to move units. This is a significant increase from the peak of the pandemic housing boom in Q2 2022, when the incentive rate was only 1.5%. More tellingly, their average sale price has retreated to 2017 levels.

Overall, we seem to be witnessing a massive divergence:

New Home Inventory: Has ballooned to nearly 10 months of supply.

Existing Home Sales: Are languishing at levels not seen since 1995, back when the U.S. population was 20% smaller.

The market is currently pricing in a "soft landing" for real estate, but they are ignoring the 11% drop in new home sales this January.

When the "new" version of a product (with warranties and 5% subsidized mortgage rates) is selling for nearly the same price as the "used" version (with aging roofs and 6.2% market rates), the "used" market is toast. The only thing keeping existing home prices elevated is a lack of urgency—an urgency that is about to be forced by the largest generation of homeowners in American history.

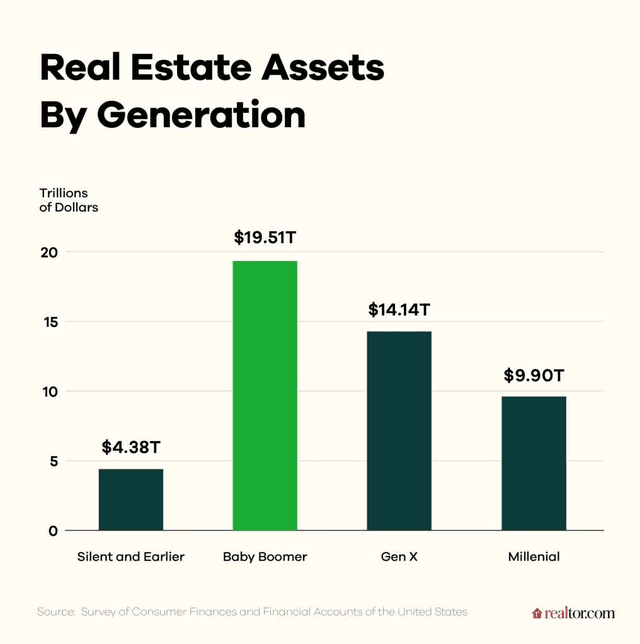

The Boomer Death Cross: $19.5 Trillion in Search of an Exit

For years, the "housing shortage" has been the ultimate safety net for real estate bulls. They point to low inventory and "locked-in" 3% mortgages as a permanent floor for prices. But they are looking at a snapshot of the past, and not towards the future. We are fast approaching a point where the sheer weight of aging demographics finally crushes the artificial scarcity of the post-COVID era.

The Concentration Risk

The numbers are staggering. Baby Boomers currently sit on roughly $19.51 trillion in residential real estate assets. To put that in perspective, that is nearly double the real estate wealth of Millennials. For a decade, this generation has been the "Great Withholder" of inventory, choosing to age in place or renovate rather than downsize.

We are now entering a window where "aging in place" becomes physically or financially impossible for millions. Whether it is the rising cost of property taxes—which are outpacing inflation—or the simple reality of the human lifecycle, this $19.5 trillion is a concentrated inventory bomb waiting for a catalyst.

The Breakdown of the "Lock-In" Effect

The bulls argue that no one will sell because they don’t want to trade a 3% mortgage for a 6.2% one. This assumes that all sales are elective. They aren't.

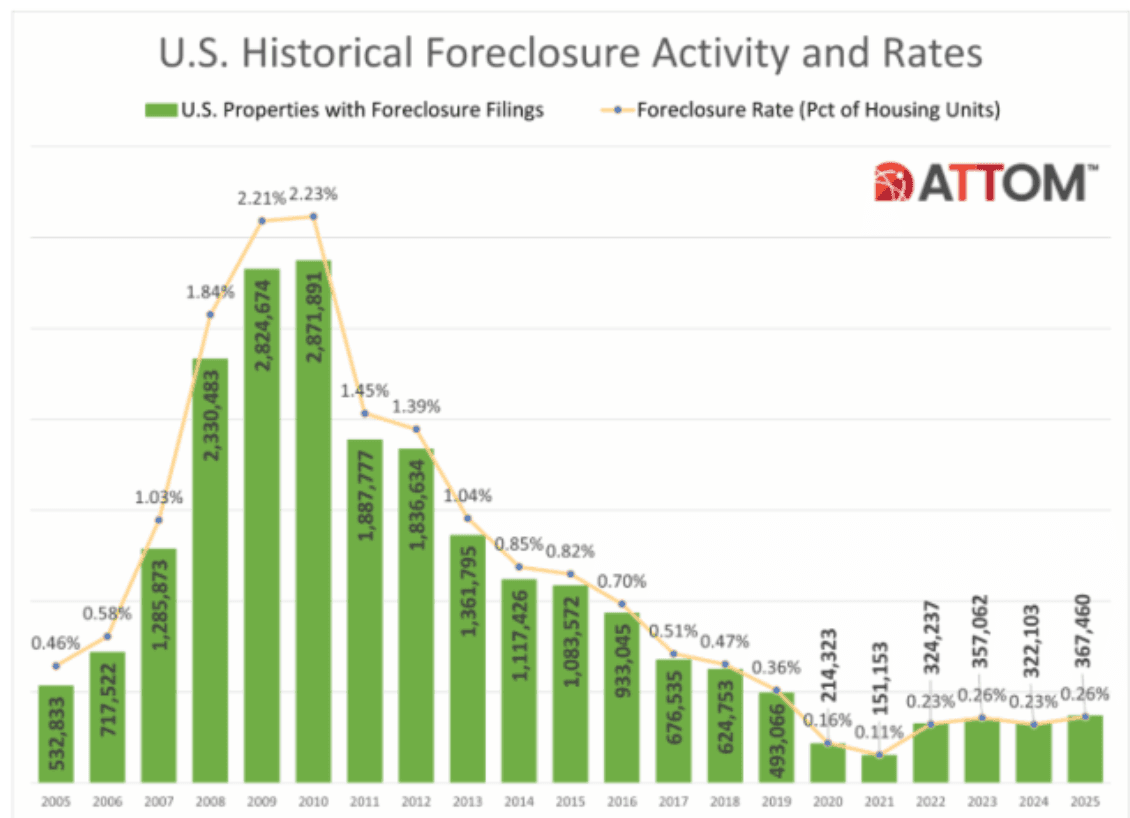

With COVID-era forbearance programs finally in the rearview mirror as of last summer, FHA foreclosure rates are quietly ticking up.

Similarly, with diesel prices close to $5.50 and the Strait of Hormuz effectively closed, the cost of maintaining a 30-year-old suburban home (roofs, HVAC, appliances) is skyrocketing.

Then there is also the new home pivot to thinking about.

Why would a buyer struggle to negotiate with a Boomer who is anchored to 2022 prices when they can walk into a Lennar development and get a brand-new home with strong incentives and a mortgage buy-down?

The Liquidity Gap

The "Death Cross" occurs when this "must-sell" inventory meets a buyer pool that is fundamentally broken.

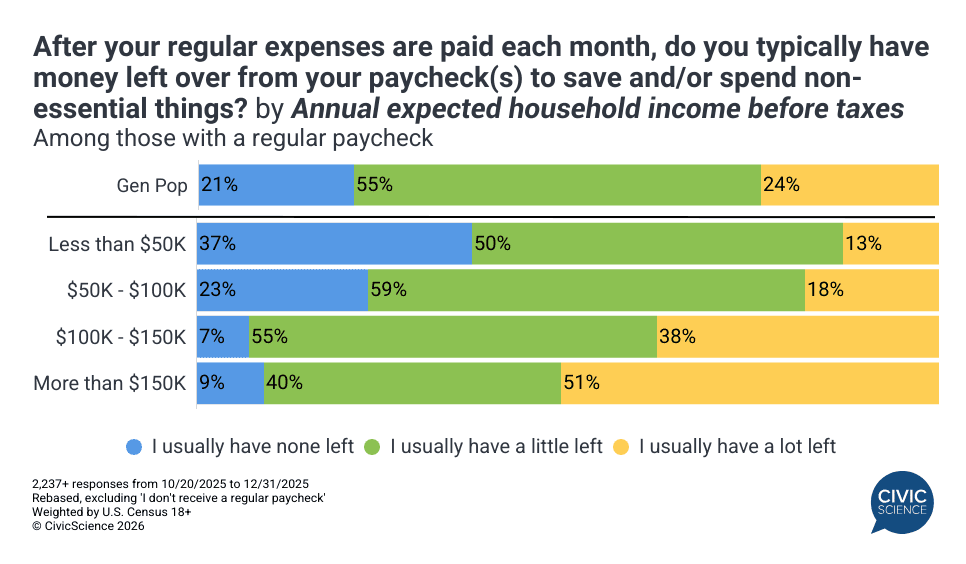

In 2025, more than a fifth of all US households were living paycheck to paycheck.

When the Silent Generation and the older Boomers begin to liquidate—whether by choice, medical necessity, or estate settlement—they will find a market where the "Top 10%" already have their mansions, and the other 90% can’t even afford the insurance on a bungalow.

When $19.5 trillion in assets looks for an exit at the same time the job market turns negative, "price discovery" won't be a gentle correction. It will be a forceful liquidation, as I will discuss in the next section.

When the "Sacred Cow" Becomes a Liability

For decades, the American home has been the ultimate "sacred cow" of building wealth. But in 2026, the math has turned predatory. We are witnessing the birth of a Liquidity Trap where the asset that supposedly anchors the middle class is actually the weight pulling them under.

The Negative Equity Feedback Loop

For the vast majority of U.S. households, real estate is the most valuable asset on their list of holdings.

But as we’ve seen, giant builders like Lennar are already pricing new homes at 2017 levels to move inventory. This creates a brutal "price floor" that existing homes simply cannot meet without a massive correction.

When the "average" existing home price inevitably moves lower to compete with new builds—which offer modern efficiency and subsidized 5% mortgage rates—trillions in perceived wealth will vanish. For the so many Americans living paycheck to paycheck, a 10% drop in home equity is a burn down of their only emergency fund.

The Cost of "Holding" is Skyrocketing

The contrarian view is that "sitting on a low mortgage" is a winning strategy.

It actually isn't.

While the mortgage rate might be fixed at 3%, the cost of ownership is hyper-inflationary:

Property Taxes & Insurance: These are reset by current valuations and rising climate/labor risks, often increasing faster than the CPI.

Maintenance: With diesel north of $5 and the Strait of Hormuz choking chemical and raw material imports, the cost to repair a roof or replace an HVAC system has doubled since 2022.

The "locked-in" homeowner is actually "locked-out" of discretionary spending. Every dollar spent on surging insurance premiums is a dollar taken away from the retail, lodging, and hospitality sectors.

The Private Credit Collision

Perhaps most dangerous is the looming credit crunch. As the crisis in private credit markets deepens, the "shadow" lending that has fueled consumer resilience is evaporating. If a homeowner loses their job in this anemic 2026 labor market, they can no longer treat their home like an ATM.

When the "Sacred Cow" of real estate finally stops being an appreciating asset and starts being a liability with rising carry costs, the top 10% won't be able to buy enough lattes to save the economy. We are underweighting consumer discretionary for a reason: The basement of the American economy is flooding, and the homeowners are the ones holding the buckets.

The "Exit Strategy" for a Frozen Market: The Global Real Estate Pivot

The U.S. residential market is increasingly a ticking time bomb of Boomer inventory and evaporating margins. But as a contrarian, you don't just "sit out"—you rotate.

While the average investor is trapped in a "sacred cow" asset (their primary residence) that is illiquid and bleeding value to property taxes, the smart money is moving toward Institutional-Grade Global Liquidity.

Stop Speculating. Start Arbitrating.

Surmount’s Global Real Estate Exposure Strategy isn't a "buy and hold" hope-fest. It is a cold, calculated machine designed to strip the emotion out of property investing.

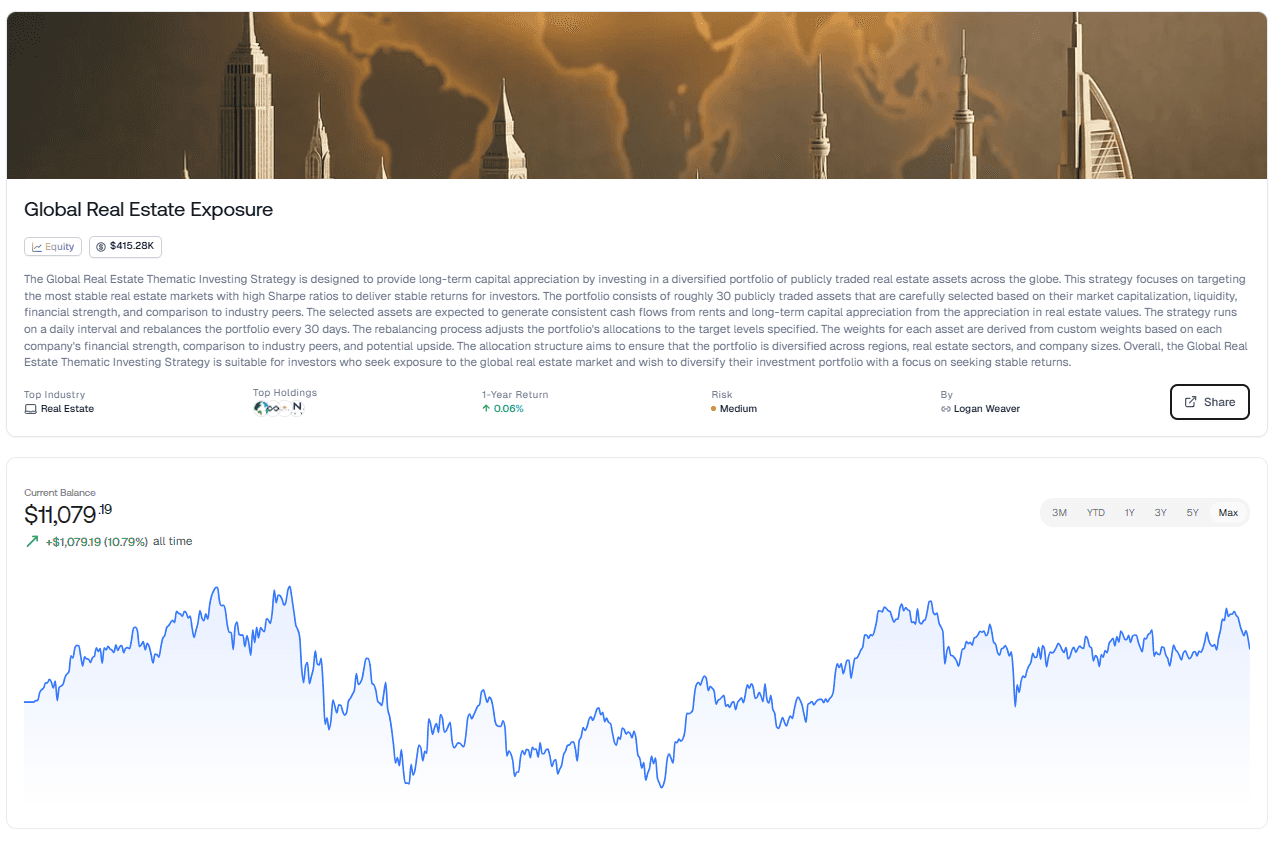

Here is why this is the only way to play real estate in 2026:

Beyond the U.S. Death Cross: This strategy diversifies across global regions where demographics and cap rates haven't been distorted by a decade of U.S. stimulus.

The 30-Day Agility Edge: While an existing home sale takes months to close, this strategy rebalances every 30 days. If a specific sector or region starts showing "Lennar-style" margin decay, the algorithm rotates your capital into more resilient, high-Sharpe ratio assets.

Institutional Strength Only: We ignore the "mom-and-pop" rental traps. This portfolio selects roughly 30 publicly traded powerhouses based on rigorous financial strength and liquidity metrics—the kind of balance sheets that can survive a private credit crunch.

Daily Surveillance: The strategy runs on a daily interval, monitoring market caps and peer comparisons to ensure you aren't holding the bag when the next "SaaSpocalypse" hits a local economy.

Don't get stuck in the mud.

If the U.S. housing market is about to enter a liquidation phase, you want your real estate exposure to be liquid, global, and automated.

[Click Here to Deploy the Global Real Estate Strategy]

Target stability. Seek upside. Rebalance for the new reality.

NEVER MISS A THING!

Subscribe and get freshly baked articles. Join the community!

Join the newsletter to receive the latest updates in your inbox.