Investing During Inflation: How The Same Investors Win Every Cycle

Most investors treat inflation like a weather event — something that happens to them. The investors who built serious wealth during the worst inflationary periods in modern history treated it differently. They saw it as a transfer mechanism, identified the pattern early, and positioned before the crowd caught on.

This piece maps those decades. The pattern is less complicated than the financial media makes it sound — but acting on it consistently is harder than it looks.

Inflation Doesn't Behave the Way Most Investors Think

The mainstream response to rising inflation is predictable: buy gold, maybe some TIPS, wait it out. That playbook is not wrong exactly — it's just incomplete, and chronically late. By the time inflation dominates headlines and your advisor is recommending adjustments, the easy money in inflation trades is largely gone.

Investing during inflation rewards the investor who moves on early signals, not confirmed ones. That's the first uncomfortable truth the historical record establishes clearly. For instance, there is already a strong case that the Fed may already be losing to inflation.

The second is that inflation is not uniformly destructive. It destroys certain portfolios while systematically enriching others. Understanding which side of that divide you're on is the entire game.

The Decades That Reveal the Pattern

The 1940s — War, Supply Shocks, and the First Lesson in Real Assets

World War II created one of the most acute inflation environments in American history. Supply chains were redirected toward the war effort, consumer goods became scarce, and prices surged. The investors who fared best held real assets — farmland, commodities, and equities in companies with direct exposure to physical production.

The inflation decades history from this period establishes the foundational rule: when the purchasing power of money deteriorates, assets with intrinsic physical value or productive capacity hold and grow that purchasing power. Paper claims on money — bonds, savings, fixed-income instruments — erode. Real assets inflate alongside everything else.

The 1970s — Stagflation and the Portfolio Strategy That Actually Worked

The 1970s remain the defining case study. Two oil shocks, wage-price spirals, and a Federal Reserve that was perpetually behind the curve produced a decade of punishment for conventional portfolios. The 60/40 portfolio — the bedrock of mainstream wealth management — delivered negative real returns for much of the decade.

What worked during stagflation was a concentrated rotation into hard assets: oil and energy equities, precious metals, and real estate. Investors running a stagflation portfolio strategy with meaningful commodity exposure didn't just preserve wealth — many compounded it aggressively. The 1970s inflation investing record shows that energy equities in particular delivered extraordinary returns while the broader market stagnated.

The secondary lesson from this decade: duration was lethal. Long-dated bonds were obliterated as rates rose. Short-duration instruments and floating-rate exposure preserved capital while everything else burned.

2021–2022 — The Modern Replay and Who Got It Right

The most recent inflationary episode followed the same script with modern instruments. Investors who rotated into energy, commodities, and inflation and interest rates portfolio positioning — shortening duration, tilting toward real assets — outperformed sharply. The S&P 500 fell over 18% in 2022. Energy equities gained over 60%.

The investors who got it wrong were those anchored to the prior decade's disinflation regime, still holding long-duration growth equities and investment-grade bonds. The pattern from the 1940s and 1970s repeated almost precisely — and was widely dismissed until it was too late to position for.

The Assets That Show Up Every Time

Hard Assets and Commodities — The Consistent Winners

Across all three decades, the common thread is straightforward. Commodities during inflation outperform because inflation is, at its core, a rise in the price of real things.Companies that produce those real things — energy, agriculture, metals, real estate — see revenues rise with prices while their cost bases lag. That margin expansion drives equity outperformance.

Though, as we’ve discussed earlier, it is important to keep in mind that not every commodity price surge is what it appears.

Hard assets vs inflation is not a subtle relationship. It is one of the most consistent patterns in financial history, and yet retail investors remain chronically underweight these assets going into inflationary cycles because they've been trained on a 40-year bull market in financial assets.

The Inflation-Proof Portfolio: What the Pattern Actually Looks Like

Synthesizing the three decades, the inflation resistant investment strategy that consistently worked had three characteristics. First, meaningful allocation to real assets and commodity-linked equities. Second, short duration — avoiding long-dated fixed income when rates are rising. Third, early positioning — rotating before CPI headlines force the consensus to act.

This is not a complex framework. It is a consistently ignored one. Building an inflation proof portfolio is less about exotic instruments and more about having the conviction to act counter-cyclically before the thesis is obvious.

Why Most Investors Get the Thesis Right and Still Lose

Being Early Is Worthless Without a System to Act On It

Here is the uncomfortable part. Most sophisticated investors who study these inflationary decades intellectually understand the pattern. Very few of them execute it well. Beating inflation with investments requires not just the right positioning but the discipline to hold it through the inevitable periods of doubt — when inflation cools temporarily, when growth assets stage a counter-rally, when the crowd mocks the trade.

Knowing what investments do well during high inflation is table stakes. The actual edge is behavioral: a pre-committed, rules-based approach that executes the strategy without second-guessing at precisely the wrong moment. This includes knowing when the cycle is turning against you.

That is where most investors — including sophisticated ones — lose the advantage their analysis gave them.

How to Play it

Understanding the pattern is step one. Having a system that actually executes on it — without hesitation, without second-guessing, and without the emotional drag that causes most investors to buy the thesis and still lose money — is what separates the investors who make it into the history books from those who merely read about them.

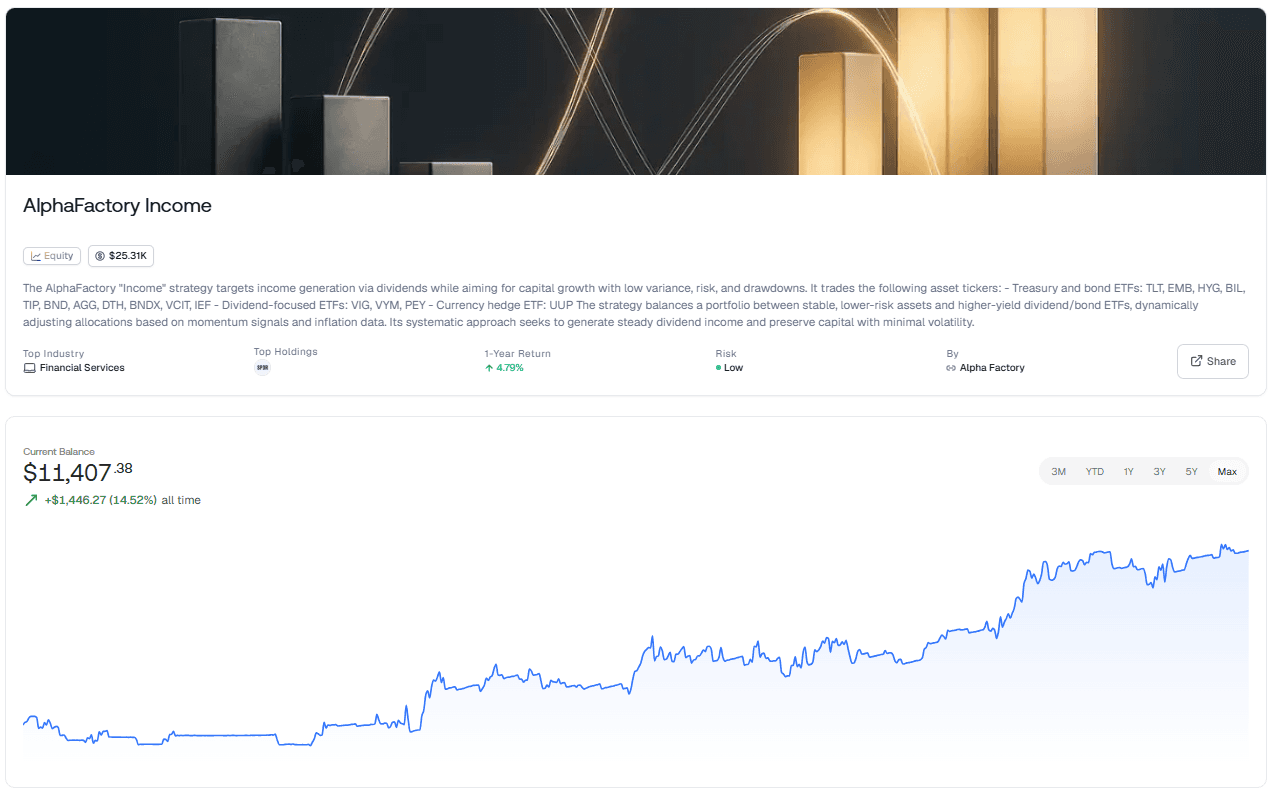

This is exactly where AlphaFactory Income comes in.

While most portfolios sit statically positioned as inflation erodes their real value, AlphaFactory Income is actively working against that erosion. It dynamically allocates across short-duration T-bills, inflation-protected securities, dividend ETFs, and bond instruments — adjusting in real time based on momentum signals and live inflation data. It doesn't wait for CPI headlines to confirm what the early indicators already showed. It doesn't freeze up when the consensus narrative shifts. It responds systematically, the way every investor in every inflationary decade wished they could have.

The 1940s, 1970s, and 2022 all made the same point: the investors who won weren't necessarily smarter. They were more decisive, better positioned earlier, and — critically — they didn't abandon the trade at the worst moment. AlphaFactory Income is built to enforce that discipline automatically, on your behalf, across your existing portfolio.

Inflation doesn't wait for you to feel ready. Neither should your strategy.

[Deploy AlphaFactory Income to your portfolio on Surmount AI →]

Conclusion — The Pattern Is Clear. Is Your Strategy?

Every major inflationary decade has made the same investors rich: those who identified the regime early, rotated into real assets and short duration, and held the position with discipline while the consensus caught up. The pattern is not obscure. It is hiding in plain sight in the historical record.

Investing during inflation is not primarily an analytical problem. It is an execution problem. If you want a system that lets you act on macro conviction without emotional interference — and automate that positioning across your existing portfolio — that is exactly what Surmount AI is built for.

Frequently Asked Questions

What is the best strategy for investing during inflation?

The most consistent inflation investing strategy across history is rotating into real assets, commodities, and short-duration instruments before CPI headlines force the crowd to act. Early positioning separates the winners from everyone else.

What investments do well during high inflation?

Hard assets, commodity-linked equities, and energy stocks have been the consistent winners across every major inflationary decade. Long-duration bonds and growth equities are historically the biggest losers.

How did investors make money during the 1970s stagflation?

The 1970s inflation investing winners ran a concentrated stagflation portfolio strategy heavy in oil, energy equities, precious metals, and real estate. Those who stayed in conventional 60/40 portfolios saw negative real returns for most of the decade.

Why does an inflation-proof portfolio need real assets?

Because inflation is fundamentally a rise in the price of real things — commodities, land, and physical production. Real assets inflate alongside prices, preserving and growing purchasing power while cash and bonds erode.

How do interest rates affect your portfolio during inflation?

Rising rates destroy long-duration bonds while rewarding short-duration and floating-rate instruments. Aligning your inflation and interest rates portfolio positioning toward shorter duration is one of the most reliable defensive moves in an inflationary cycle.

NEVER MISS A THING!

Subscribe and get freshly baked articles. Join the community!

Join the newsletter to receive the latest updates in your inbox.