Is Cash a Safe Investment in 2026? The Slow Bleed Reality

There's a certain comfort in watching your balance sit still. You don’t see red days, volatility alerts, and there are no anxious portfolio checks at midnight. For millions of investors, T-bills and money market funds have become the default hiding place. It is a way to feel responsible while the market does whatever it wants.

But most people don’t realize that stillness is costing you. Quietly, consistently, and with mathematical certainty.

Cash isn't protecting your wealth in 2026. It's eroding it. And the investors who understand this are already repositioning while everyone else applauds their own caution.

The Illusion of Safety — What Cash Is Really Doing to Your Wealth

Safety is a feeling. Real returns are a fact. Right now, those two things are telling very different stories.

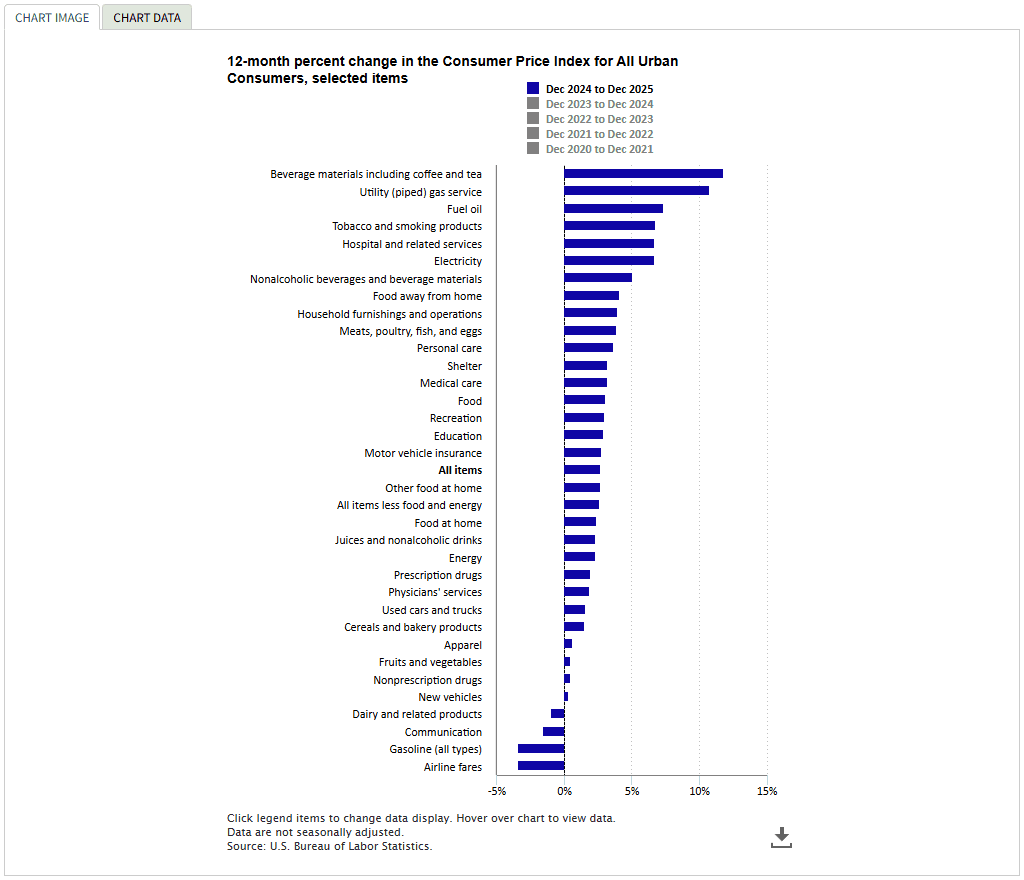

Money market funds are yielding somewhere in the 4.5% to 5% range. That sounds reasonable on the surface. But once you account for inflation — which has proven far stickier than the Federal Reserve originally projected — your real return shrinks to something between flat and slightly negative, depending on how honestly you measure purchasing power erosion.

And that's before taxes. After tax, the picture gets uglier.

Purchasing Power Erosion in 2026 — The Numbers Don't Lie

A dollar that sits in cash doesn't stay a dollar in real terms. It loses ground every single year inflation runs above your yield. At a 3.5% inflation rate and a 4.8% money market yield, your real pre-tax gain is roughly 1.3%. After federal income tax at a typical high-net-worth rate, you're likely negative.

This is the slow bleed. No single day looks catastrophic. But compounded over three, five, or ten years, the purchasing power erosion in 2026 is not a rounding error — it's a meaningful destruction of wealth dressed up as prudence.

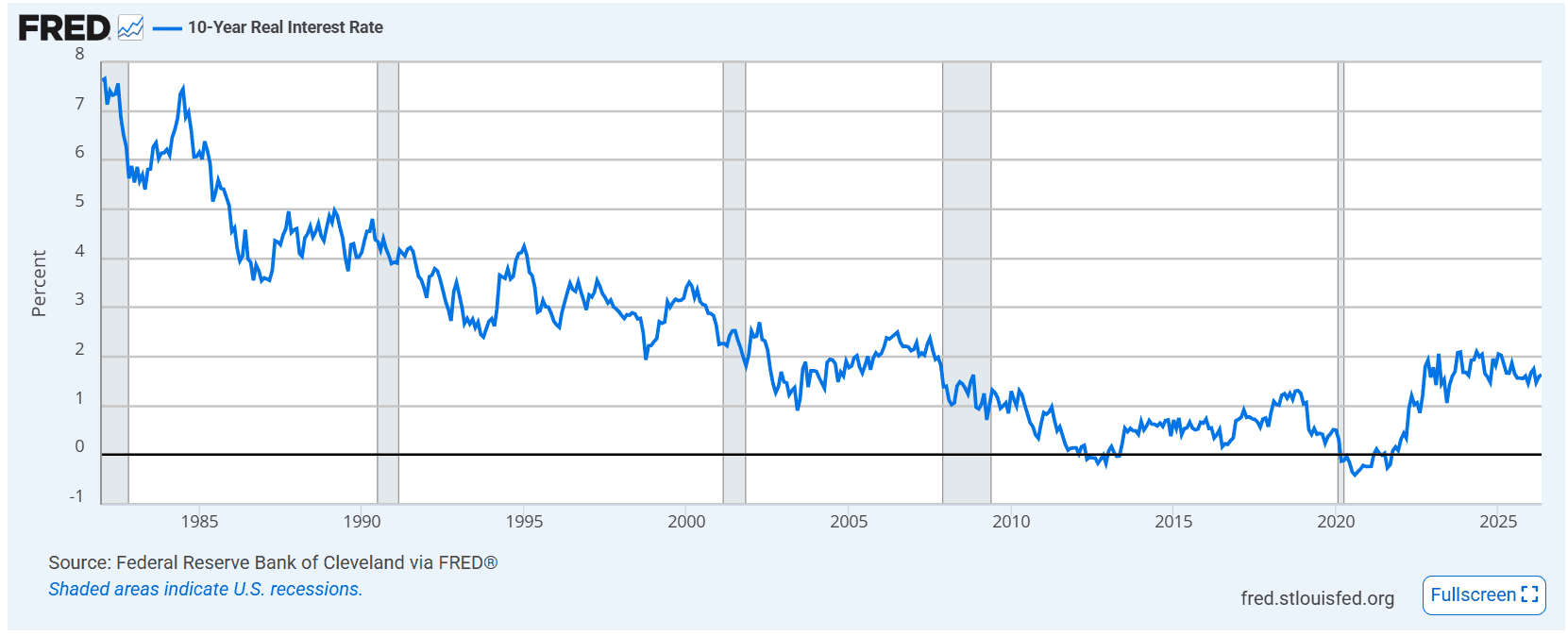

Real Return on Cash vs Inflation — A Losing Trade

Historically, cash has only truly "won" during deflationary periods or when the Fed was actively crushing inflation with rates well above the CPI. Neither condition describes the current environment. The real return on cash vs inflation today is, at best, marginally positive — and structurally at risk of turning negative if inflation reaccelerates, which remains a credible scenario.

Why This Time Is Different — The Macro Regime Has Shifted

The instinct to hide in cash made a lot more sense between 1987 and 2021. That era was defined by falling yields, contained inflation, and a bond market that reliably cushioned equity drawdowns. The classic 60/40 portfolio worked precisely because of that structural tailwind.

That tailwind is gone.

Nominal GDP Growth and Equities — The Dynamic Cash Investors Are Ignoring

We have entered a macro regime more closely resembling the 1950s through 1980s — a period defined by persistent nominal GDP growth, elevated capital spending, and yields that trended higher alongside a growing economy. In that environment, nominal GDP growth and equities moved together. Cash and long-duration bonds were the underperformers.

The driver today is aggressive AI infrastructure investment, reshoring of industrial capacity, and sustained government spending. These are not short-term sugar highs. They represent a multi-year capital expenditure cycle that keeps corporate earnings — and nominal growth — elevated.

Bond Yields Rising — What It Really Means for Investors

Most retail investors have been conditioned to treat bond yields rising as a fire alarm for equities. That's not always accurate. When yields rise because the economy is growing — because borrowing demand is strong and earnings are expanding — that is not inherently bad for stocks. It's bad for cash holders and long-duration bond holders who mistakenly believed they were in a safe haven.

The question is never simply whether yields are rising. It's why they're rising. Growth-driven yield increases are a feature of a healthy nominal expansion, not a warning sign to liquidate into cash.

Portfolio Strategy for an Inflationary Environment

Inflation Hedge Strategies for High Net Worth Investors

Sophisticated capital has been quietly rotating for months. The sectors benefiting most in a persistent inflation hedge strategy are those tied to real assets, pricing power, and essential capital spending: energy, industrials, financials, and AI infrastructure.

And as we’ve pointed out earlier, the same playbook repeats itself with remarkable consistency.

These aren't speculative bets. They're businesses that generate earnings in nominal terms — meaning inflation actually works in their favor rather than against them. A portfolio strategy for an inflationary environment looks nothing like the one that worked between 2010 and 2021. It requires deliberate sector exposure and active rebalancing (such as through time arbitrage investing), not passive allocation and a cash buffer.

Alternatives to Holding Cash — Where Sophisticated Investors Are Repositioning

The contrarian investing strategy in 2026 isn't simply "buy more equities." It's about identifying where real returns are available and positioning accordingly.

Alternatives to holding cash for investors who understand the macro regime include: inflation-linked equities in energy and industrials, companies directly embedded in the AI infrastructure buildout, and commodity exposure that benefits from sustained capital spending. These aren't outlier ideas — they're logical conclusions from the macro data.

Active investing vs cash holding isn't even a close debate when real rates are structurally compressed and nominal growth is the dominant tailwind.

Stop Watching the Regime Shift From the Sidelines

Everything discussed in this piece points to the same conclusion: the old playbook is broken, cash is bleeding you dry, and the investors who win in this environment are the ones with deliberate, active exposure to the forces actually driving nominal growth.

The single biggest force driving nominal growth right now is deep technology.

Not speculative software. Not multiple-expansion stories built on hope and low rates. The real infrastructure of the AI era — semiconductors, machine learning systems, cybersecurity, cloud computing, and the hardware that makes all of it run. These are the companies with pricing power, capital inflows, and earnings momentum that thrive precisely when nominal GDP is the dominant tailwind.

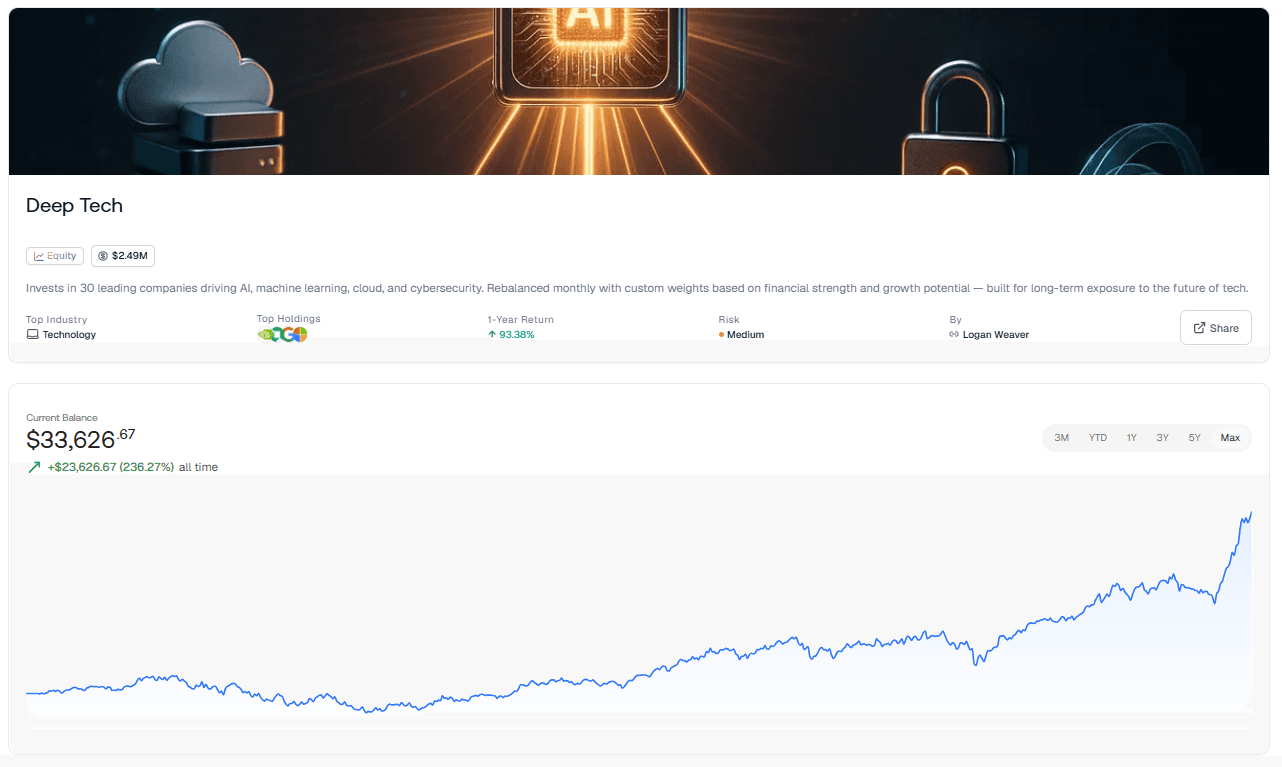

This Is Exactly What the Deep Tech Strategy Is Built For

Surmount's Deep Tech Strategy invests in 30 of the leading companies driving this transformation — carefully weighted by financial strength, industry positioning, and growth potential. It isn't a passive index bet that buries your capital in yesterday's winners. It's a dynamically rebalanced, algorithmically managed portfolio that stays aligned with the companies at the actual center of the AI infrastructure buildout.

Every 30 days, the strategy recalibrates. Dead weight gets trimmed. Stronger positioning gets reinforced. You're not set-and-forget in a world that's moving faster than any static allocation can track.

The Real Edge Is Automation

Here's what most high-net-worth investors get wrong even when they have the right thesis: they act on it too slowly, too emotionally, or too inconsistently.

You can read every macro piece published this year, build the perfect mental model of the regime shift, and still underperform because execution is where conviction goes to die. A position held too long. A rebalance skipped during volatility. A rotation delayed because the news cycle spooked you.

The Deep Tech Strategy removes that friction entirely. The algorithm doesn't panic. It doesn't second-guess the thesis at 2am when yields spike. It executes — systematically, repeatedly, and without the behavioral drag that quietly destroys real returns for even the most sophisticated investors.

This Is the Antithesis of Sitting in Cash

While money market investors are earning a marginally positive nominal yield and a quietly negative real one, the Deep Tech Strategy is positioned in the exact companies benefiting from the capital expenditure supercycle the blog just laid out. Every dollar sitting in a T-bill earning 4.8% pre-tax is a dollar not compounding inside the infrastructure of the next decade.

The regime has shifted. The data is clear. The only question left is whether you're going to act on it.

Deploy the Deep Tech Strategy on Surmount AI and put your portfolio on the right side of this macro trade.

Final Thoughts

Is cash a safe investment in 2026? Only if you define safety as the absence of volatility rather than the preservation of real wealth. By that honest measure, cash is one of the riskiest positions a high-net-worth investor can hold in the current macro environment.

The regime has shifted. The old rules no longer apply. And the investors who recognize that earliest will be the ones who look back at 2026 as the year the opportunity was obvious — if you were willing to see it.

FAQ Section

Is cash a safe investment in 2026?

Not in real terms. Inflation is quietly eroding your purchasing power faster than money market yields can compensate.

Why is cash losing value to inflation now?

The post-COVID macro regime has kept inflation structurally elevated, meaning cash yields rarely outpace real purchasing power erosion after tax.

How does nominal GDP growth affect cash holders?

When nominal GDP growth drives equities and earnings higher, cash holders fall further behind — missing compounding returns while inflation chips away at their balance.

What are the best alternatives to holding cash?

In an inflationary environment, energy, industrials, and AI infrastructure equities offer real returns. Automated investing strategies can help you rotate into these systematically.

When does an inflationary environment hurt cash most?

When real returns on cash vs inflation turn negative — which happens when inflation runs persistently above your yield, exactly the condition unfolding in 2026.

NEVER MISS A THING!

Subscribe and get freshly baked articles. Join the community!

Join the newsletter to receive the latest updates in your inbox.